Articles

Whether you are just beginning your investing journey or are looking to take your portfolio to the next level, Arbor stands ready with our talented team and decades of expertise. Given our vast experience and national footprint of successful deals, we are familiar with many common commercial real estate investor questions, such as the ones answered in this article.

Articles

With the macroeconomy maintaining its underlying strength and a handful of rate cuts expected by the Fed within the next 18 months, green shoots of optimism within the multifamily sector are multiplying. Even as high interest rates impede normal operations, stabilization is underway while the sector’s long-term prospects remain unwavering. In this deep dive, our research teams will explore the tailwinds underpinning the multifamily sector’s short- and long-term outlook.

FHA® Interest Rate Reduction (IRR) Refinance of Existing HUD-Insured Loan Arbor provides this program to reduce the interest rate on qualified existing HUD-insured multifamily loans. The HUD-insured loan remains in place, with reduced payments based on the new rate, the current balance, and the remaining term. The existing prepayment penalty must be paid in full. V041624

FHA®220 Mortgage Insurance for Rental Housing for Urban Renewal and Targeted Redevelopment* Arbor provides FHA-insured, long-term, fixed rate financing for new construction and substantial rehabilitation of multifamily projects nationwide. This program provides for both construction and permanent financing for projects in urban renewal areas and other areas where local governments have undertaken designated revitalization activities. Applications are typically processed in two stages (preliminary application followed by firm application). Affordable/rental assisted projects and HUDexperienced development teams may request a “straight to firm” application, saving significant time by eliminating the preliminary application stage. V020224

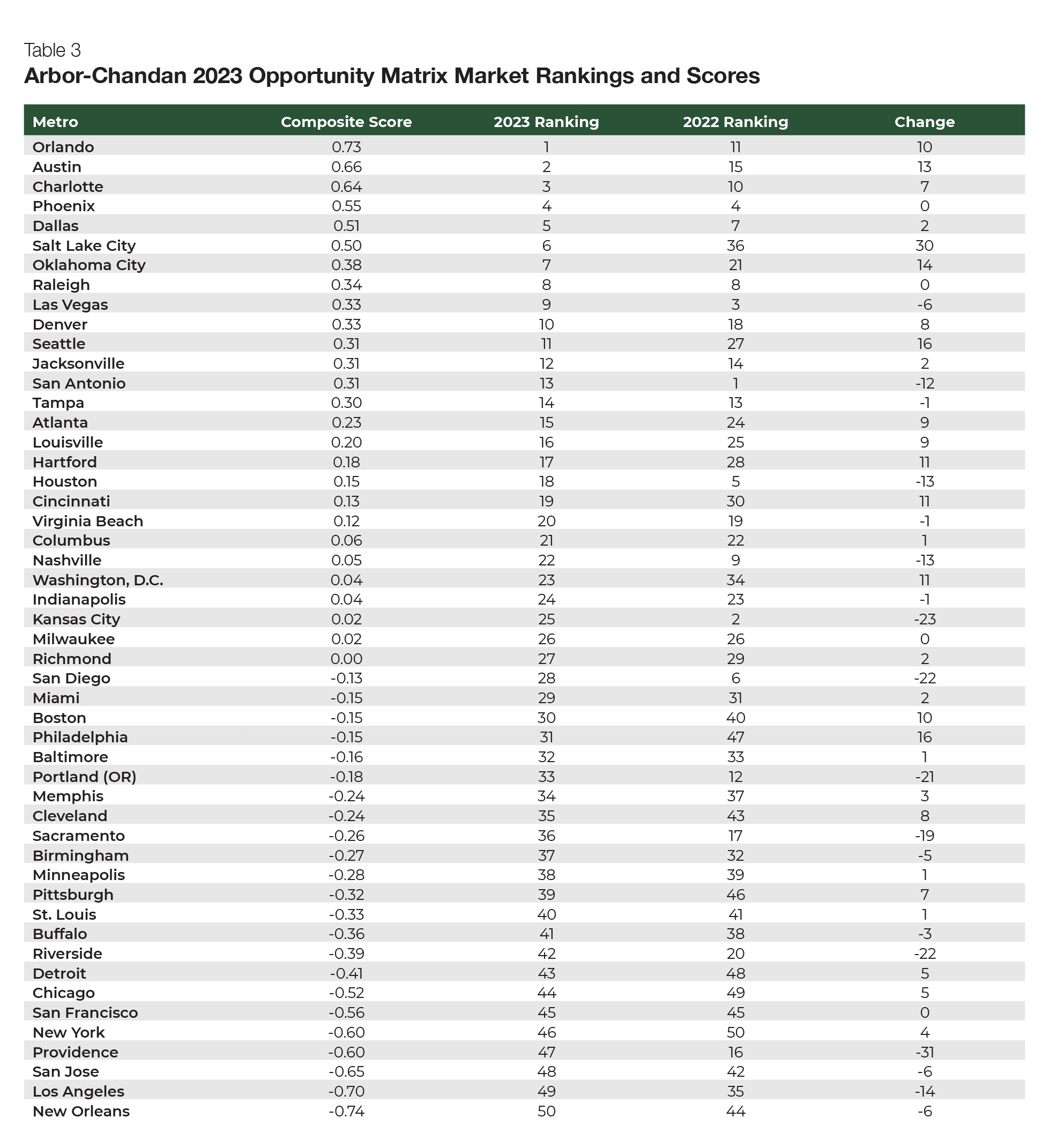

Articles

After the volume of newly issued multifamily permits hit a 37-year high in 2022, multifamily completions surged another 22.3% last year. As the sector continues to gain strength, its growth has remained concentrated in the southern and western regions of the country, according to an analysis of new data from the U.S. Census Bureau’s Survey of Construction.

Articles

During the post-global financial crisis (GFC) cycle, a disproportionate share of new multifamily construction was of high-rise units in properties with amenities. However, the tides have turned. The rising cost of homeownership has brought the need for more affordable housing development in the U.S. to the top of many legislative agendas. In this deep dive, our research teams utilize data from the U.S. Census Bureau’s Annual Survey of Construction to show how and why the characteristics of new multifamily properties continue to evolve alongside shifting market needs.

Articles

On balance, the SFR sector continues to demonstrate strength amid economic turmoil, attracting increased attention from the broader multifamily investment community.

Articles

LGBTQIA+ Pride Month is recognized in June, but its lessons are timeless. During a recent conversation between Tres Seippel, Director, Construction Management at Arbor, and Dr. Sam Chandan, Founder of Chandan Economics, Founding Director, NYU Chen Institute for Global Real Estate Finance, and Co-Chair of the Real Estate Pride Council, Seippel shared why it is more important than ever for the industry to embrace visibility and show support for employees who identify as LGBTQIA+ or other diverse backgrounds.