Find answers to common questions about multifamily and single-family rental real estate financing.

Find answers to common questions about multifamily and single-family rental real estate financing.

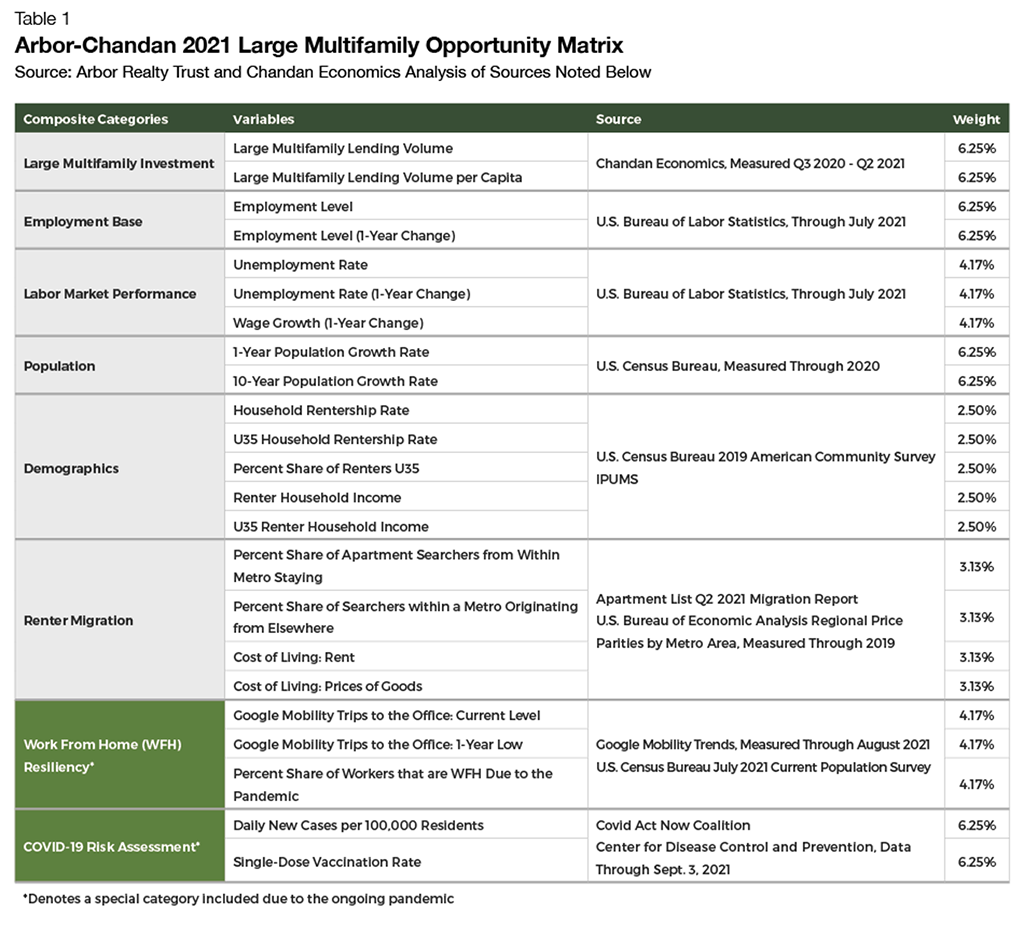

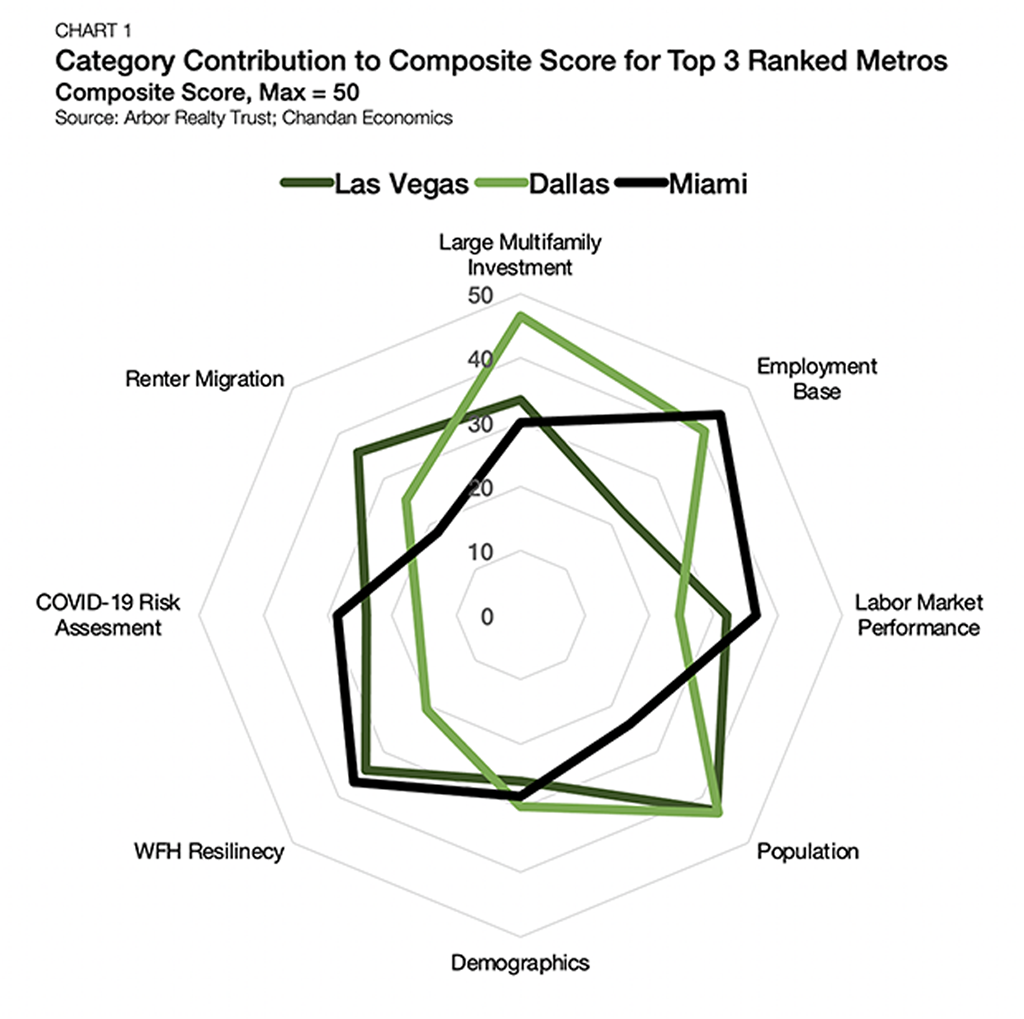

As headwinds fade and transaction volume rises, market knowledge is a critical advantage to commercial real estate investors. The Arbor Realty Trust-Chandan Multifamily Opportunity Matrix analyzed a wide range of factors within the 50 largest U.S. metros to assess market strength and durability. From maturing, dynamic metros to affordable, opportunity-rich markets, our biannual report is a roadmap to the top locations for capital deployment.

Sponsors today are increasingly choosing bridge lending solutions to capitalize on opportunities during the lease-up and stabilization phases, with multifamily completions projected to remain elevated through 2030. Bridge loans, when paired with a lender equipped to support your investment needs from construction through permanent financing, can effectively position borrowers for long-term success.

The single-family rental (SFR) sector shows renewed operational strength, supported by higher occupancy rates and improving tenant retention even as home prices have softened in mid-2025.

After proving its resilience, the multifamily real estate sector is positioned to thrive in the next growth cycle. While uncertainties persist and risks remain, new federal policies and long-awaited interest rate relief have brought optimistic investors back to the table with a new sense of urgency.

Fannie Mae and Freddie Mac, which operate under the Federal Housing Finance Agency’s Duty to Serve Plan, have made financing workforce housing a central component of creating more equitable and sustainable access to quality rental housing. With a wide range of programs and incentives now available, investors have been increasingly securing stable and valuable opportunities, which can also improve the lives of cost-burdened middle-income professionals.

Arbor takes pride in empowering employees to reach their full potential, helping to strengthen our clients and communities. With that aim, our company supported the Fifth Annual Smile Farms Invitational golf outing in Jericho, NY, on September 16, benefiting the Long Island-based non-profit dedicated to advancing opportunities for people with disabilities.

Unless an 11th-hour agreement is reached, a political impasse over budget legislation for the next fiscal year will trigger a federal government shutdown. Starting October 1, 2025, many non-essential federal government operations could potentially be limited or suspended, but most multifamily financing activities will not be disrupted.