Articles

Increasingly, single-family rental (SFR) operators have been relying on build-to-rent (BTR) development to bridge the housing gap, accelerating the momentum of SFR construction through 2024’s halfway point. Both total SFR/BTR housing starts and BTR’s share of all single-family housing starts reached new record highs in the second quarter, setting the stage for another banner year.

Current Reports

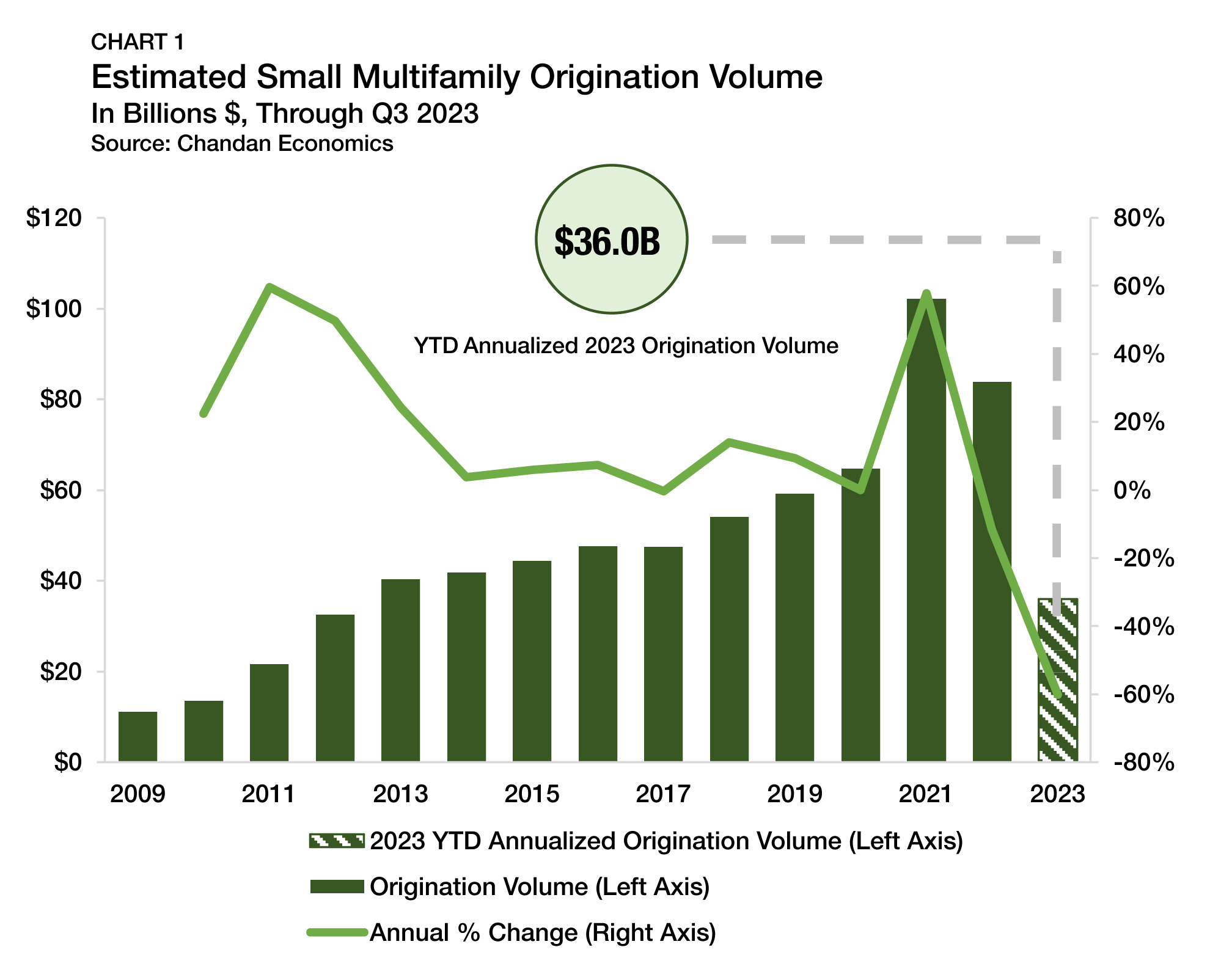

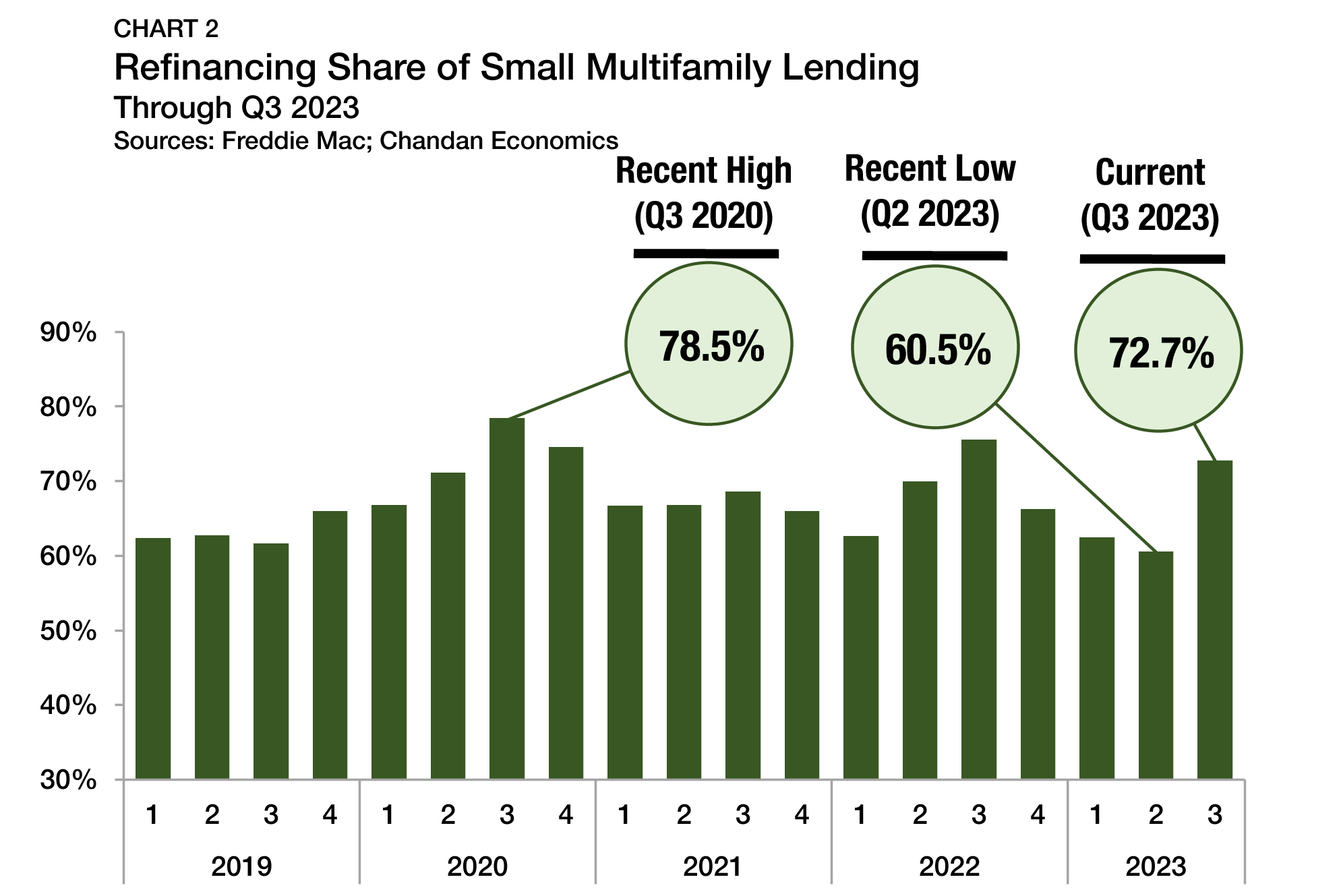

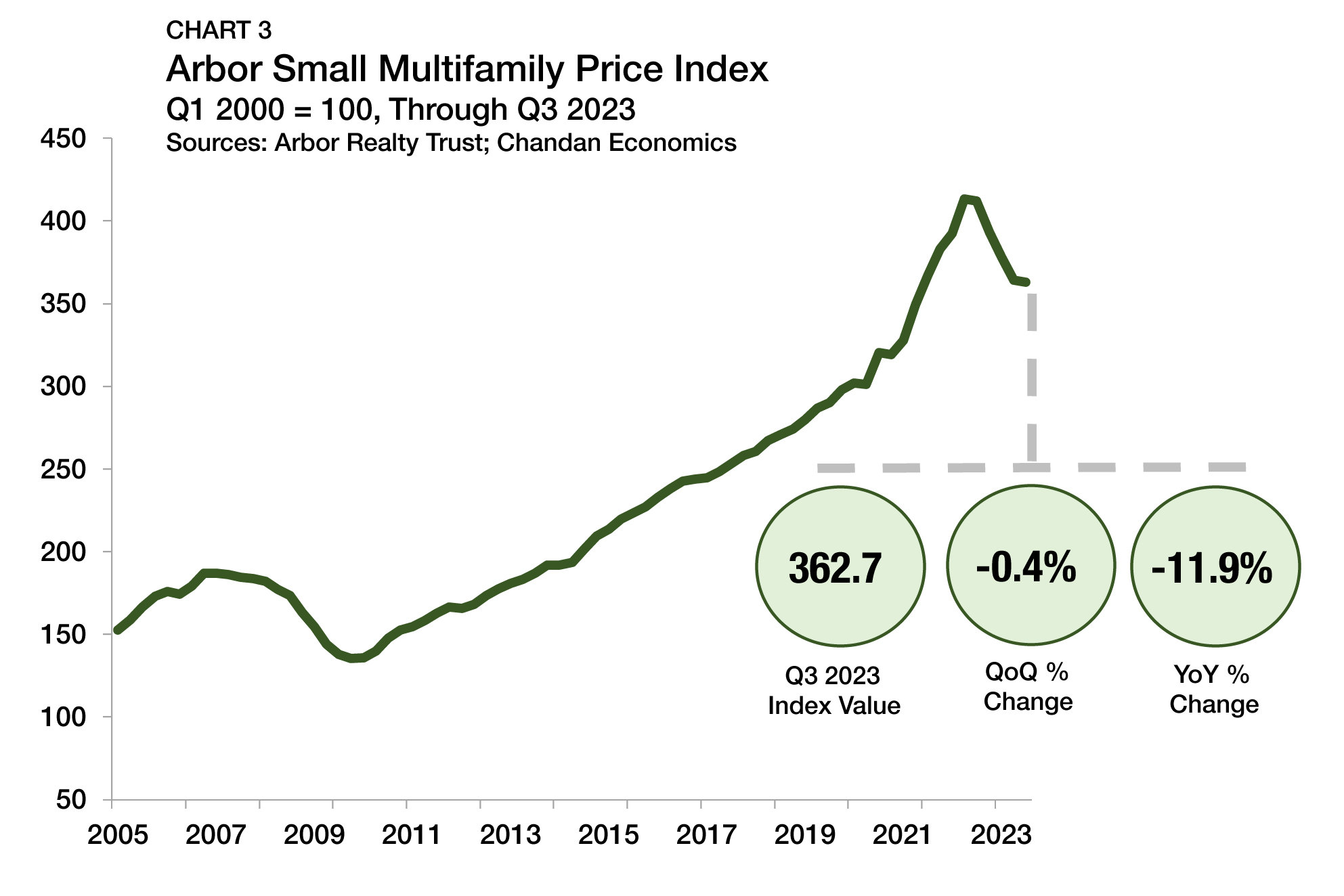

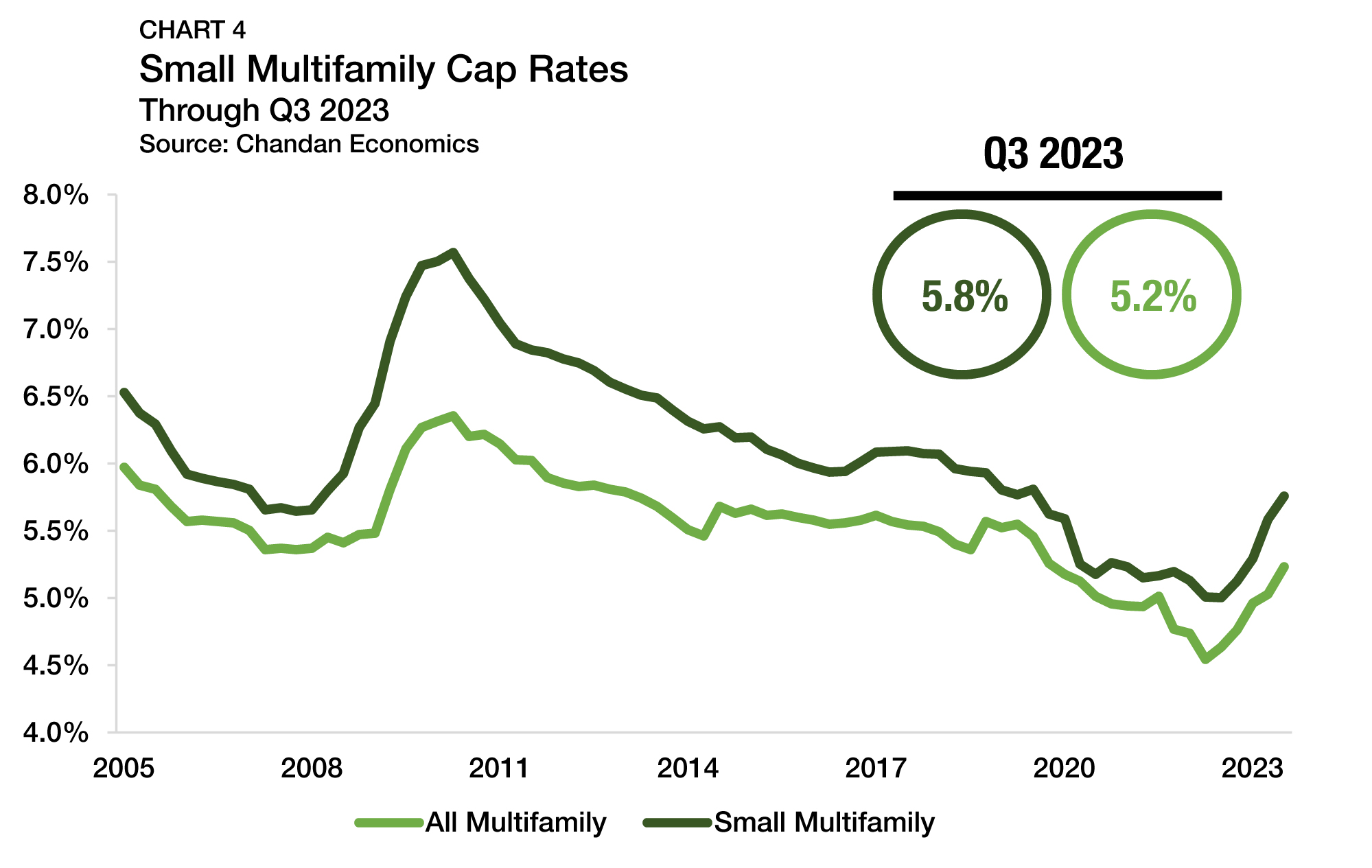

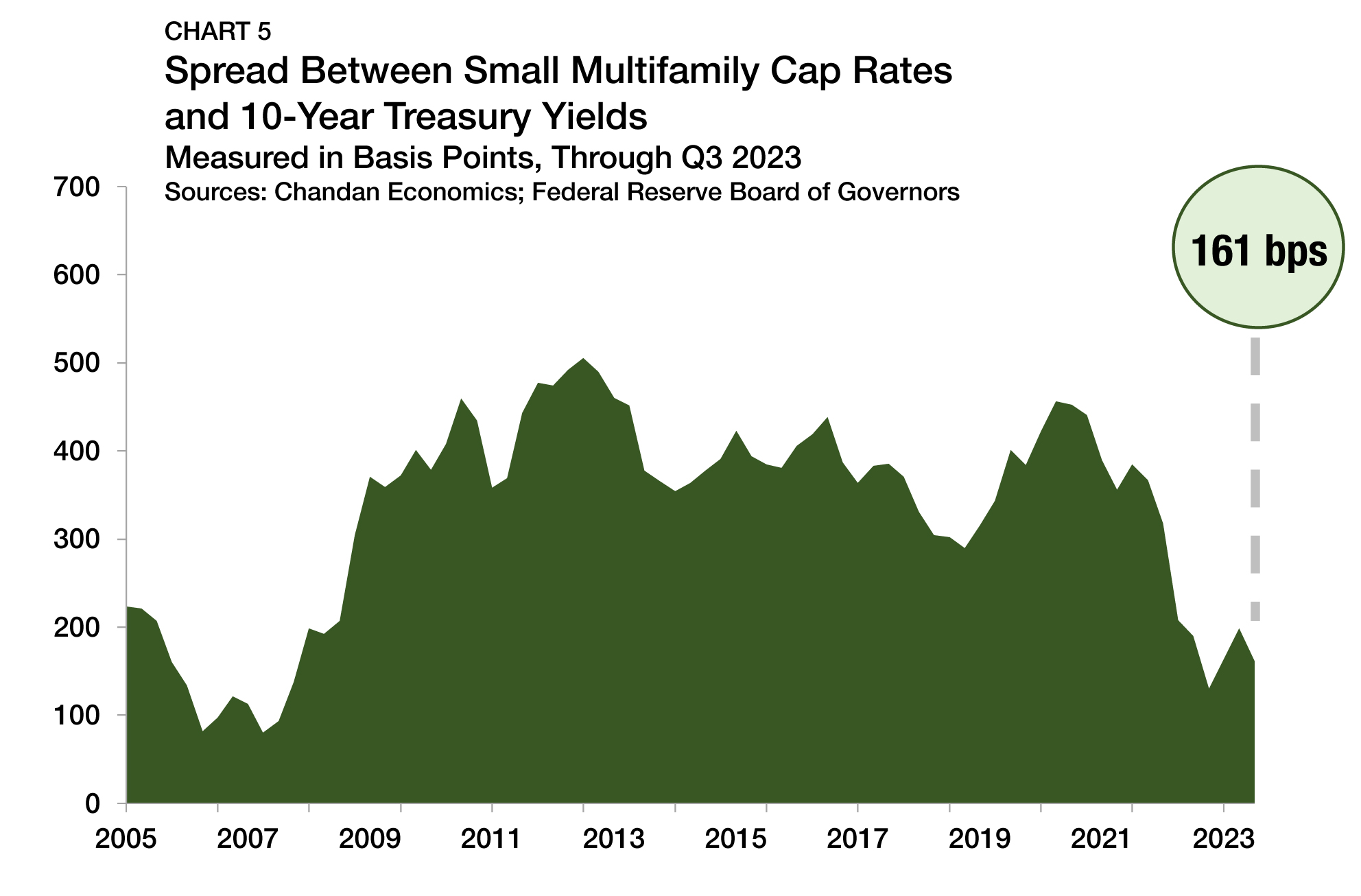

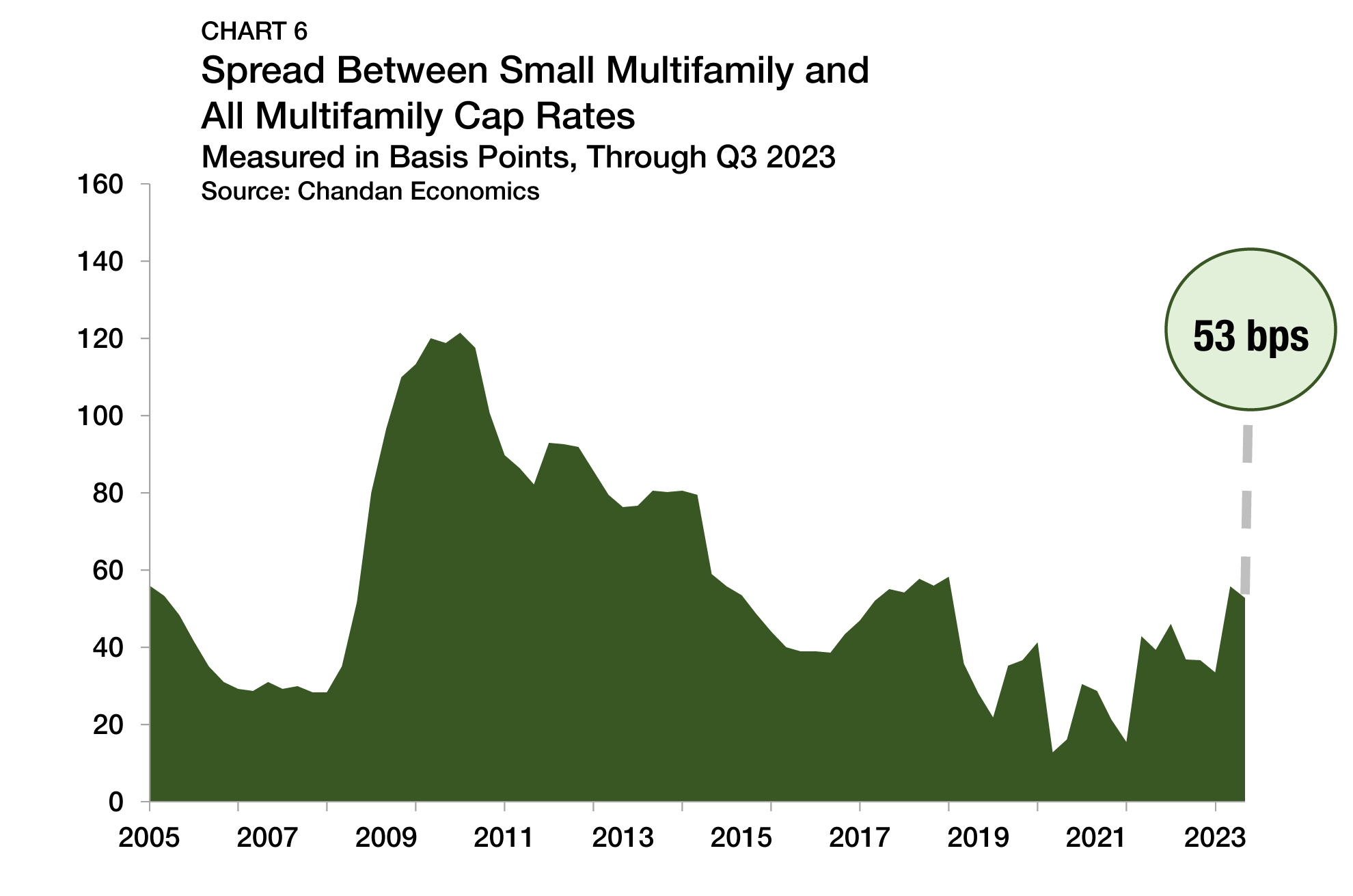

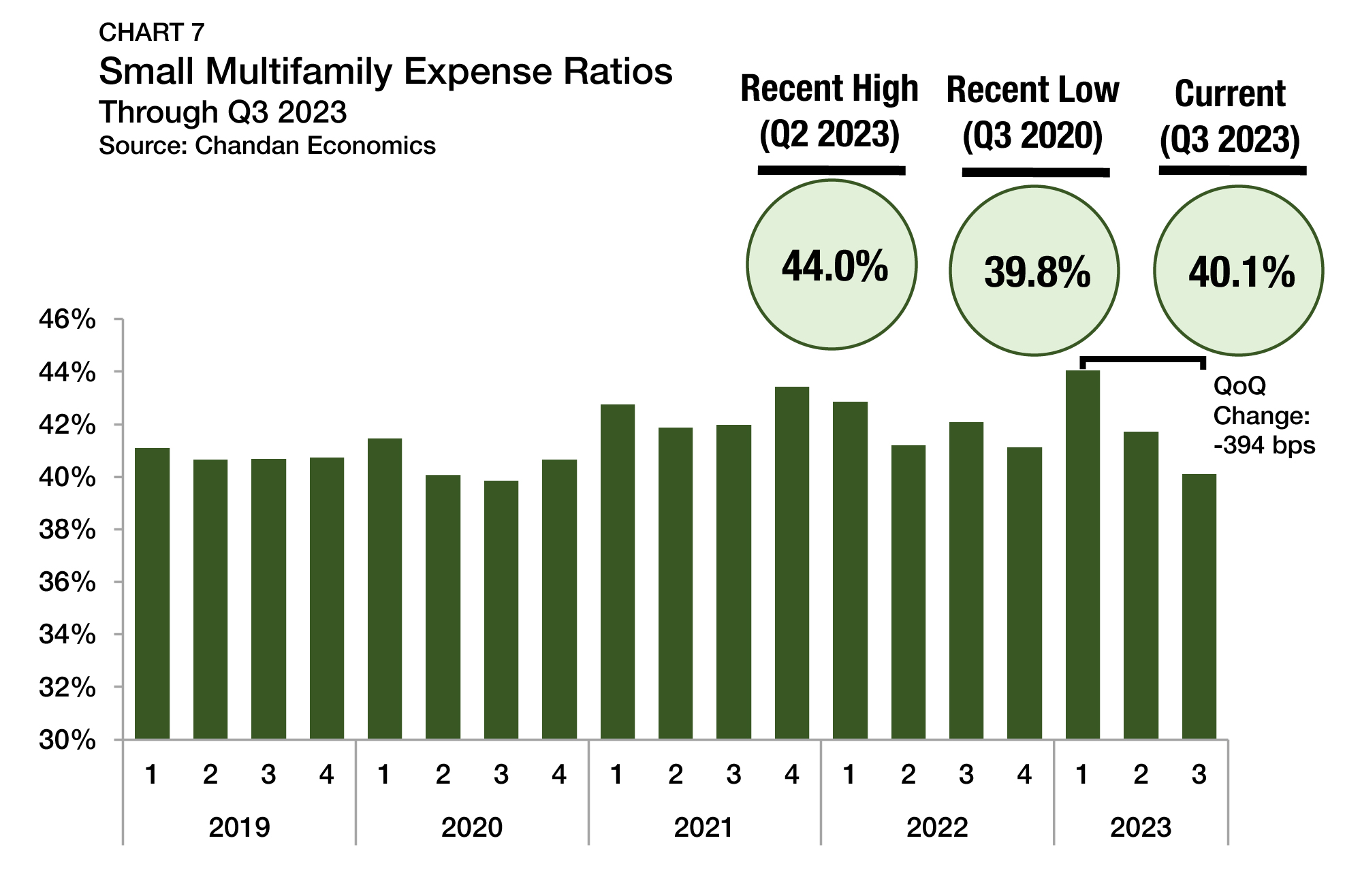

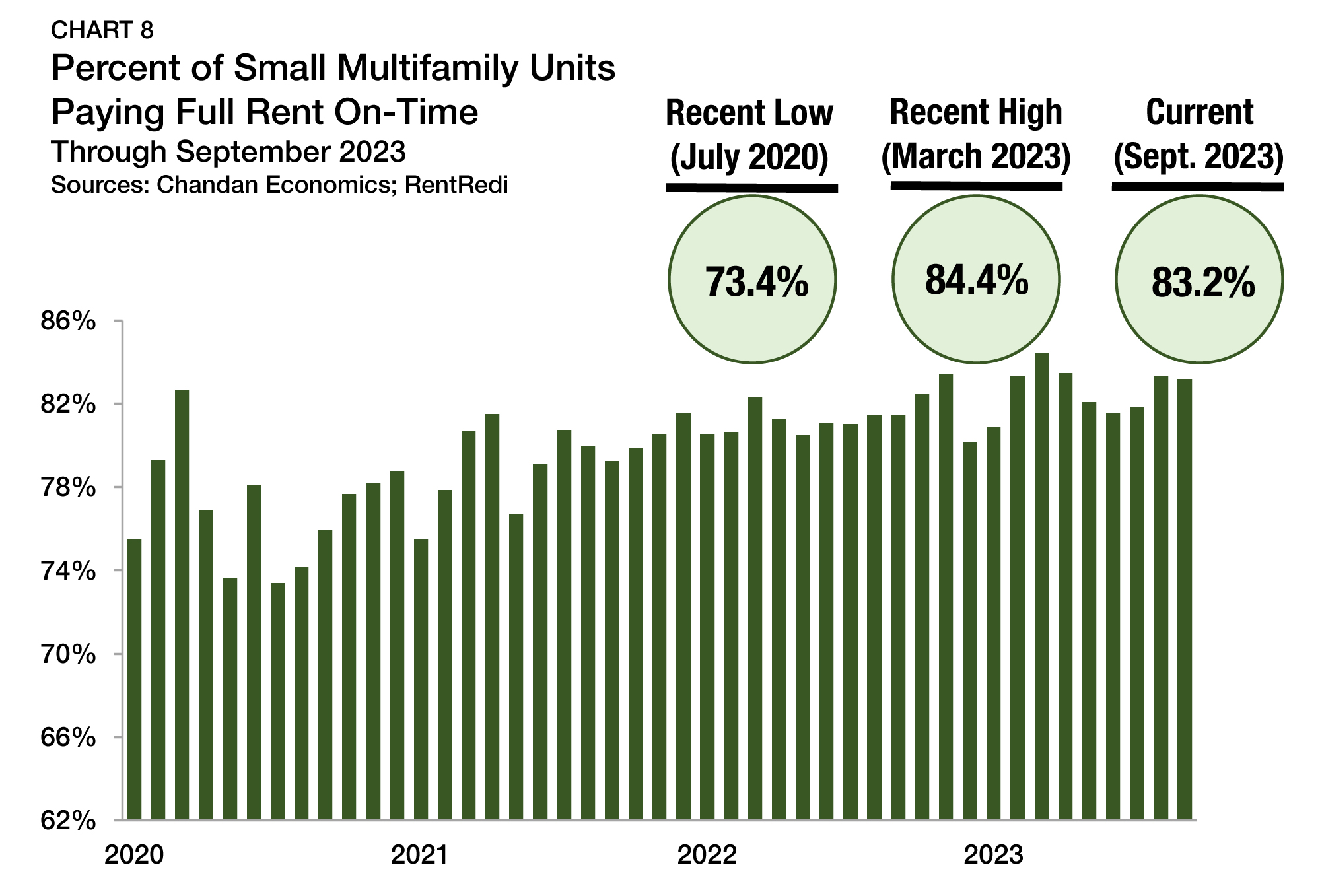

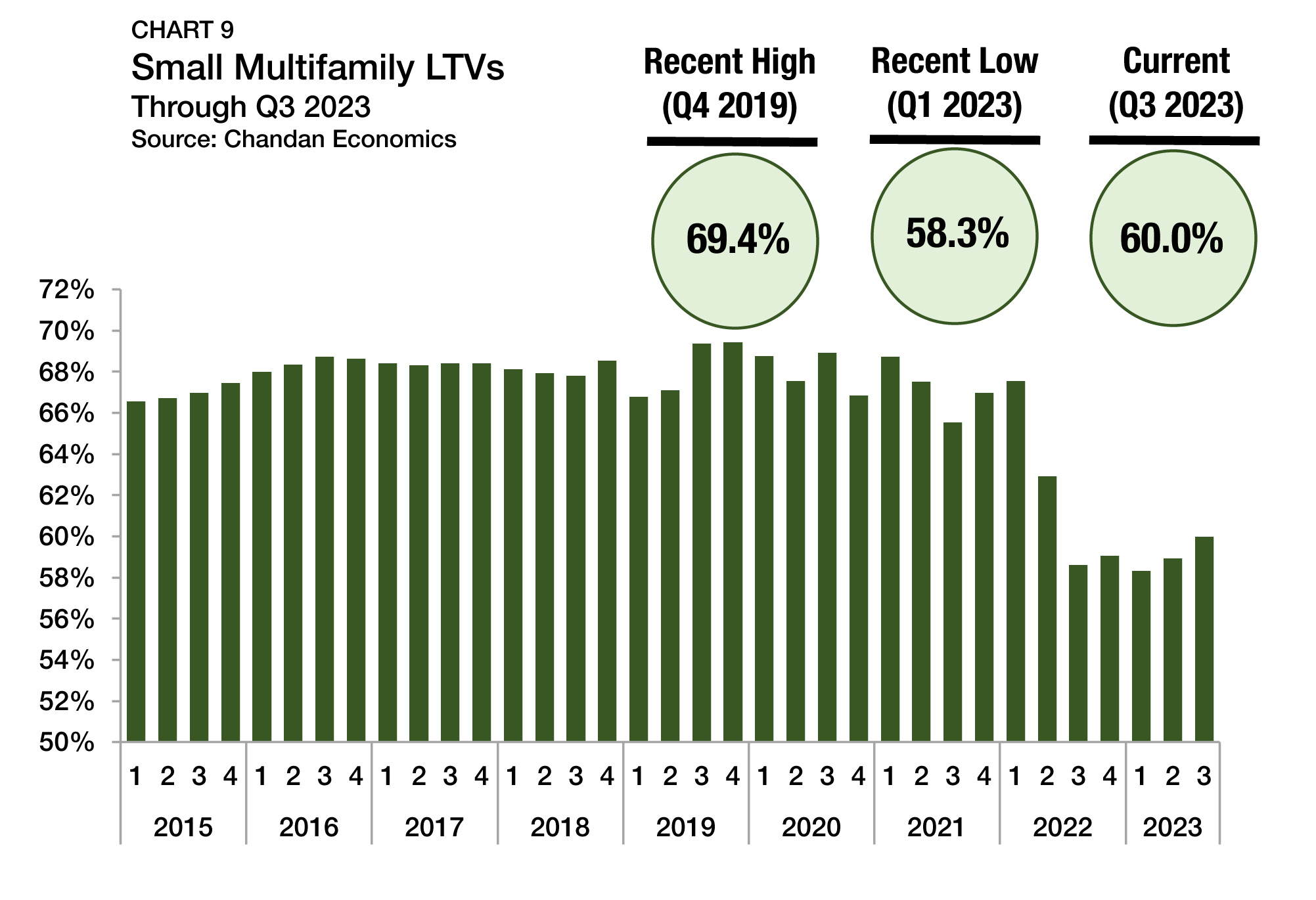

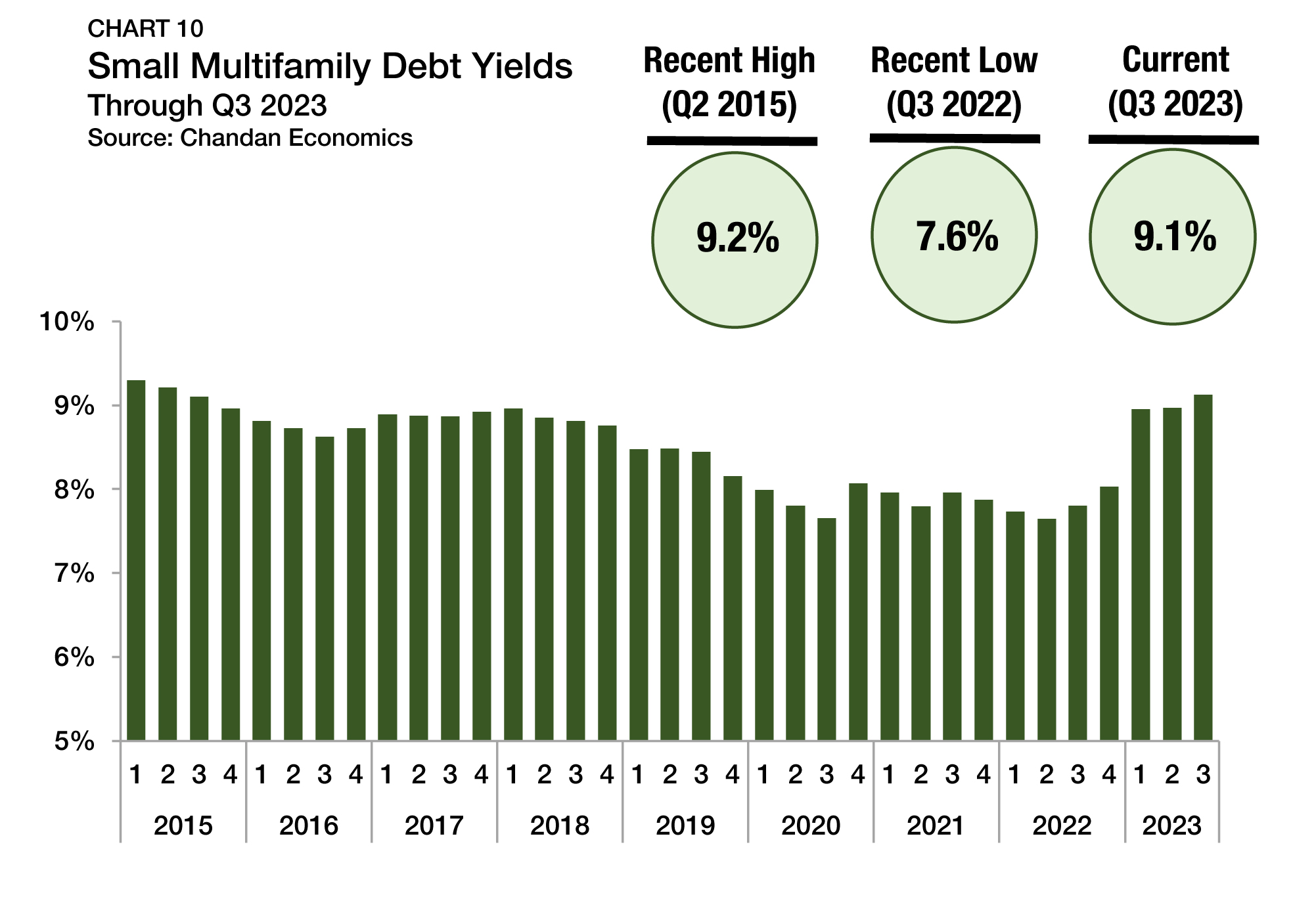

The small multifamily outlook continues to brighten as more signs indicate a normalization has already begun. In the second quarter, originations activity and borrowing conditions improved as completions sat at a five-decade high, Arbor’s Small Multifamily Investment Trends Report Q3 2024, developed in partnership with Chandan Economics, shows. While the subsector’s fundamentals are trending up, it still has room for growth when interest rate relief arrives.

Articles

While the overall pace of new multifamily permitting per capita in the U.S. slowed recently, it has picked up momentum in pockets of the country, especially the Midwest. In the first two quarters of 2024, Madison, WI, Columbus, OH, and Omaha, NE, were among the major metropolitan markets posting solid permitting gains, another sign of multifamily’s strength in all cycles.

Analysis

The U.S. multifamily market followed the quick pandemic contraction with a strong recovery, and has now normalized into a more stable cycle. Demand remained strong across the country, with a wide variety of markets among the leaders for rent growth.

Articles

Did you know that more U.S. renters now spend over 30% of their income on housing and utilities than at any other time on record? Limited affordable housing options not only increase the rent burdens of low-income tenants but disrupt physical and mental health, underscoring the need for the creation and preservation of more affordable housing units nationwide. Quality affordable housing adds stability to communities and supports healthier environments that can significantly improve well-being.

Analysis

After skyrocketing through a boom cycle over the past two years, the U.S. multifamily market settled into a cycle of stabilization in the first half of 2024. Rents held steady, occupancy increased, and vacancy rates remained in line with historical averages, while investor sentiment remained positive.

Articles

Single-family rental (SFR) CMBS issuance saw a sizeable pickup through the first half of 2024, with $4.2 billion in new issuance, placing it on pace to at least triple last year’s annual total.

Articles

Build-to-rent (BTR), a compelling solution to the U.S. housing market’s evolving needs, is experiencing record growth. BTR accounted for 8% of all single-family rental (SFR) construction starts in the 12 months that ended in the first quarter of 2024, according to Arbor’s Single-Family Rental Investment Trends Report Q2 2024. As the need for quality rental units remains high, borrowers have much to gain from partnering with an experienced lender who specializes in build-to-rent financing.