Articles

Renters accounted for roughly four-in-five new households last year, demonstrating how much rental demand has climbed while the for-sale housing market remains soft. Based on an analysis of U.S. Census Bureau data, Arbor Realty Trust and Chandan Economics examine how rental and homeowner growth in 2025 compare and outline the economic factors supporting the rise in demand across multifamily and single-family rental (SFR) housing.

Current Reports

Arbor Realty Trust’s Top Markets for Multifamily Investment Report, developed in partnership with Chandan Economics, weighed 25 variables within 10 categories to pinpoint the large metropolitan areas that are this spring’s most attractive locations for commercial real estate investment.

Articles

In many urban areas, densely concentrated housing, strong transit networks, and walkable neighborhoods offer residents viable environmentally friendly commuting alternatives. Using data from the U.S. Census Bureau’s American Community Survey, Arbor Realty Trust and Chandan Economics examined commuting patterns of workers living in multifamily rental housing in the nation’s largest metropolitan areas to identify where renters rely least on private cars to travel to the office.

Investment

Arbor Realty Trust and Chandan Economics’ latest Special Report leverages industry-leading data analysis to interpret key multifamily real estate trends as the sector moves from recalibration to stabilization. With occupancy levels remaining strong and loan originations rebounding sharply, this biannual report outlines why now is an opportune time to deploy capital.

Articles

The nation’s rental housing is older than at any point on record, with a median age of 45 years, according to the 2026 America’s Rental Housing report from Harvard’s Joint Center for Housing Studies (JCHS). America’s aging housing stock has created unique opportunities as the need for capital investments to rehabilitate and preserve affordable housing units rapidly rises.

Current Reports

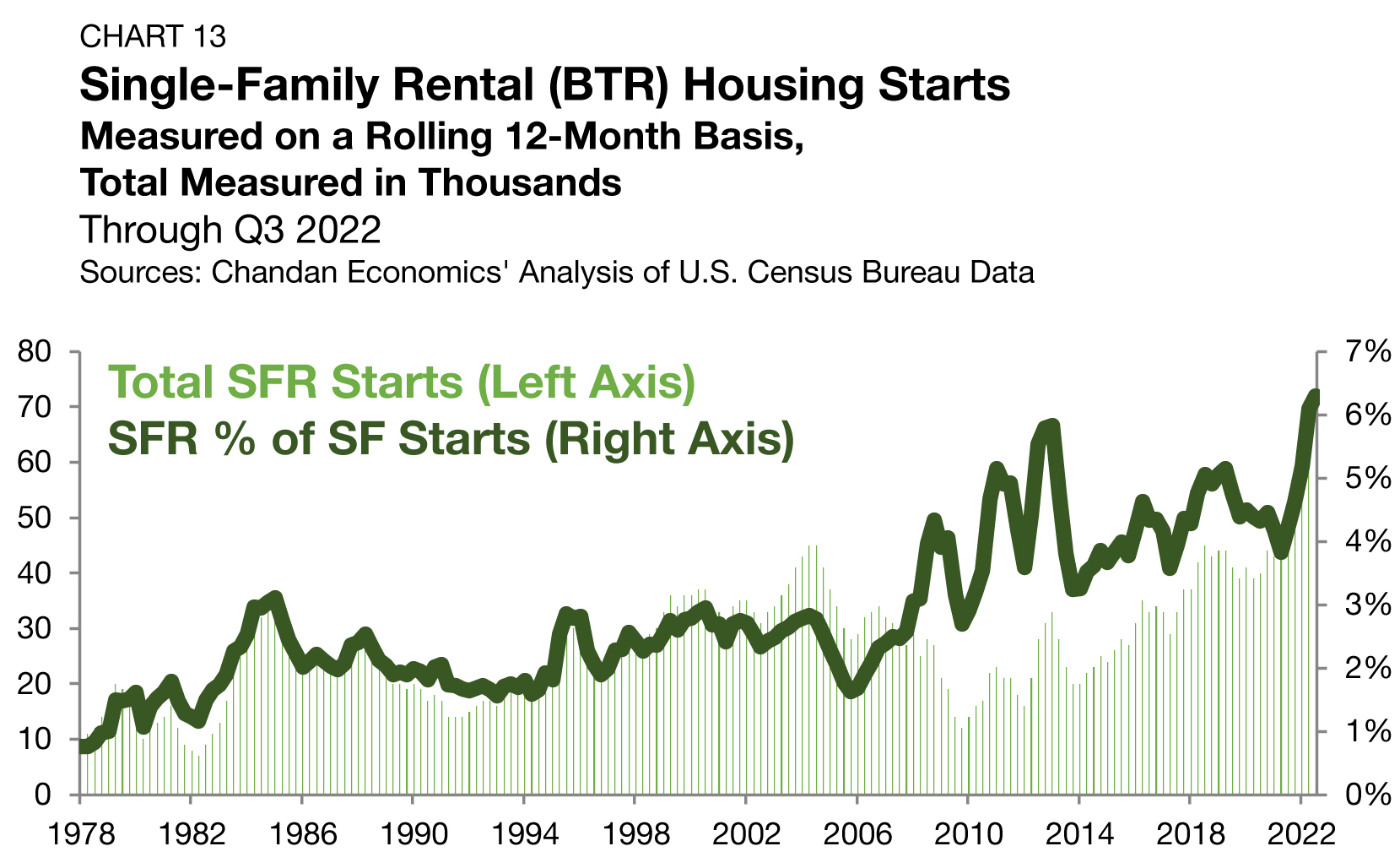

Arbor’s Single-Family Rental Investment Trends Report Q1 2026, developed in partnership with Chandan Economics, spotlights how market shifts, including the rising cost of living and historically high build-to-rent activity, have fueled record rental household growth.

Articles

Multifamily permitting trends indicate continued national stability amid local recalibration. Across the country, issuances were steady, rising just 2.6% in 2025. At the metropolitan level, trends diverged sharply, with some markets accelerating and others pulling back. Per-capita leaders continued to cluster around high-growth Sun Belt and regional hubs, while year-over-year market-level fluctuations suggest that more pipelines have become increasingly selective and, in some cases, more concentrated in large-scale projects.