FREDDIE MAC® Conventional Small

Key Findings

- The sustainability of consumer financing and geopolitical tensions are risk factors capable of triggering an economic contraction more severe than baseline forecasts.

- Unlike other commercial property types, the market standard of amortizing mortgages will insulate the rental housing sector from expiring debt distress.

- SFR/BTR should see structural gains despite cyclical headwinds as awareness for the product type grows and hybrid work supports a broader geography of housing choices for urban-working Americans.

Ivan Kaufman is the Founder, Chairman and CEO of Arbor Realty Trust, Inc. (NYSE:ABR), a leading multifamily and commercial real estate lender and real estate investment trust. Arbor manages and services a $42 billion real estate loan portfolio and has originated more than $20 billion in loans since 2021. Arbor is recognized as a top lender by Fannie Mae and Freddie Mac. Ivan is also the co-founder of Arbor Multifamily Acquisition Company (AMAC), an investment firm created in 2012, which owns and operates over 12,000 units and has acquired more than $2.5 billion of multifamily properties across the country. Through his successful development and evolution of many companies that span nearly four decades through all cycles, Ivan Kaufman is a trusted thought leader and pioneer in all aspects of commercial real estate finance.

Sam Chandan is a professor of finance and Director of the Chen Institute for Global Real Estate Finance at the NYU Stern School of Business. He joined the Stern faculty in late January 2022. From 2016 through early January 2022, he was the Larry & Klara Silverstein Chair and academic dean of the Schack Institute of Real Estate at the NYU School of Professional Studies, one of the world’s largest centers of real estate education. He is also the founder of Chandan Economics, an economic advisory and data science firm serving the institutional real estate industry, a contributor to Forbes, and host of the Urban Lab on Apple Podcasts. Dr. Chandan is chair of the Real Estate Pride Council, a global association of lesbian, gay, bisexual, and transgender leaders in the professions of the built environment. Dr. Chandan is a Fellow of the Royal Institution of Chartered Surveyors (FRICS), the Royal Society for Public Health (FRSPH), and the Real Estate Research Institute (RERI), and an Associate Member of the American Society for Microbiology (ASM). His multifaceted research interests address real estate as well as urban epidemiology and the preparedness of global cities and other systemically important urban areas in managing novel public health threats.

Sign up to receive Arbor's content in your inbox.

The Outlook

With the books closed on 2022, it is time to take stock and calibrate our expectations for the 12 months ahead. As we sit here today, in our industry and throughout the economy as a whole, we are in a corrective environment. However, the upshot is that, in our baseline forecasts, the economy is equipped and capable of absorbing a mild recession without triggering a 2008 (or pandemic shutdown) style event.

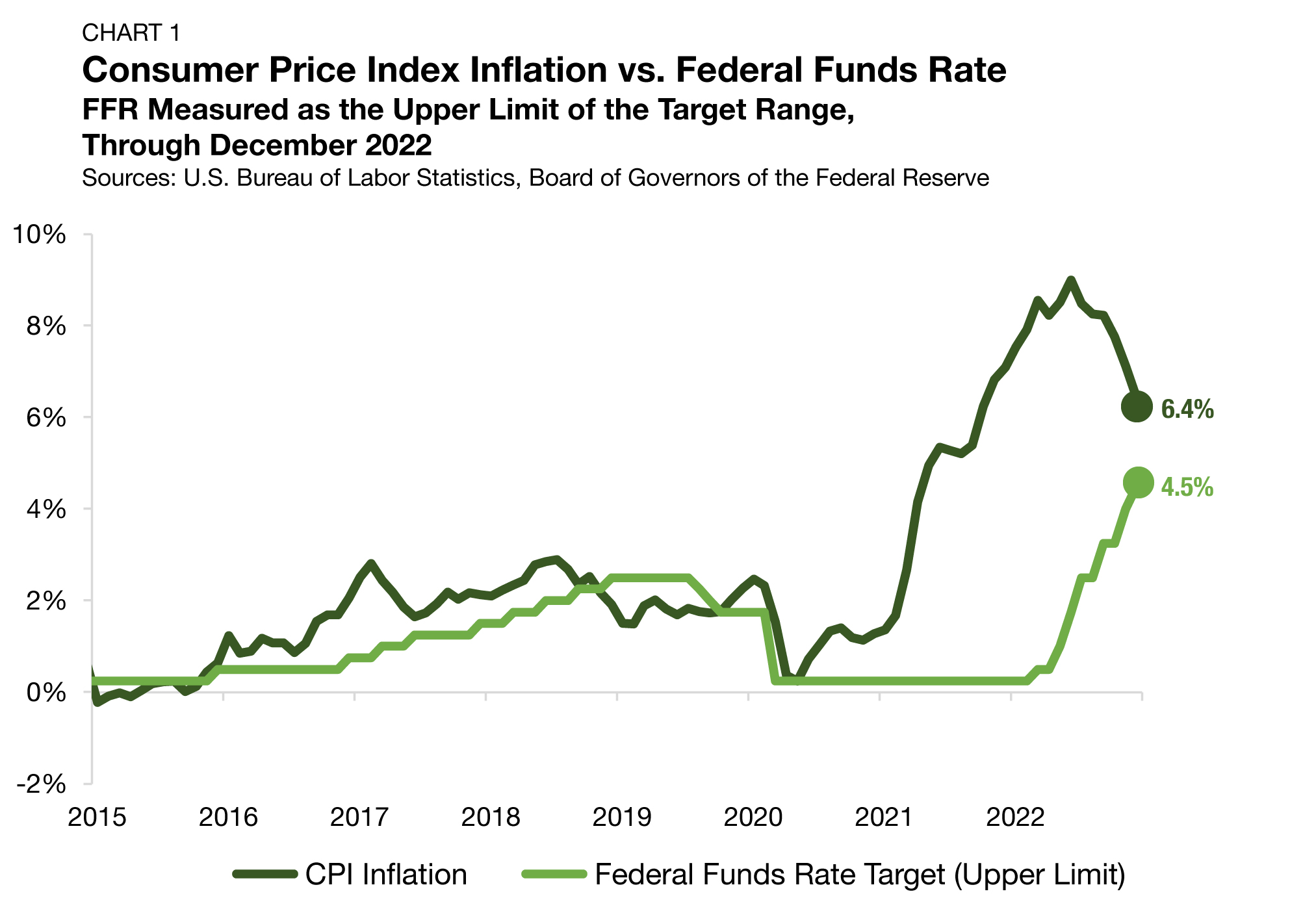

One unknown clouding the outlook is the Federal Reserve’s ongoing monetary tightening as it seeks to slow runaway inflation. The Fed moved its policy rate up by 425 bps between March and December last year. Even as the pace of inflation and interest rate increases have slowed in recent months, markets believe the tightening cycle has more runway ahead — a sentiment echoed in Federal Reserve Chairman Jerome Powell’s public statements (Chart 1).

Of course, the central bank is mindful of the fact that changes in monetary policy impact the economy with a lag. As a result, it risks overshooting its target and tightening by more than is needed. Still, the Fed has stated it will engage in monetary policy that balances the importance of price stability with strong employment to maximize the likelihood of a soft landing.

Risk Factors Abound

Front and center on the list of concerns for rental housing investors heading into next year are the business cycle and macro economy. Changes in the macro environment impact capital availability, tenant and buyer spending power, and risk appetites generally. While our median forecast for the year ahead calls for the economy to bend rather than break, the scope of uncertainty is broader today than it was before the pandemic. Beyond ongoing geopolitical tensions, several sources of concern are capable of triggering a severe contraction in 2023.

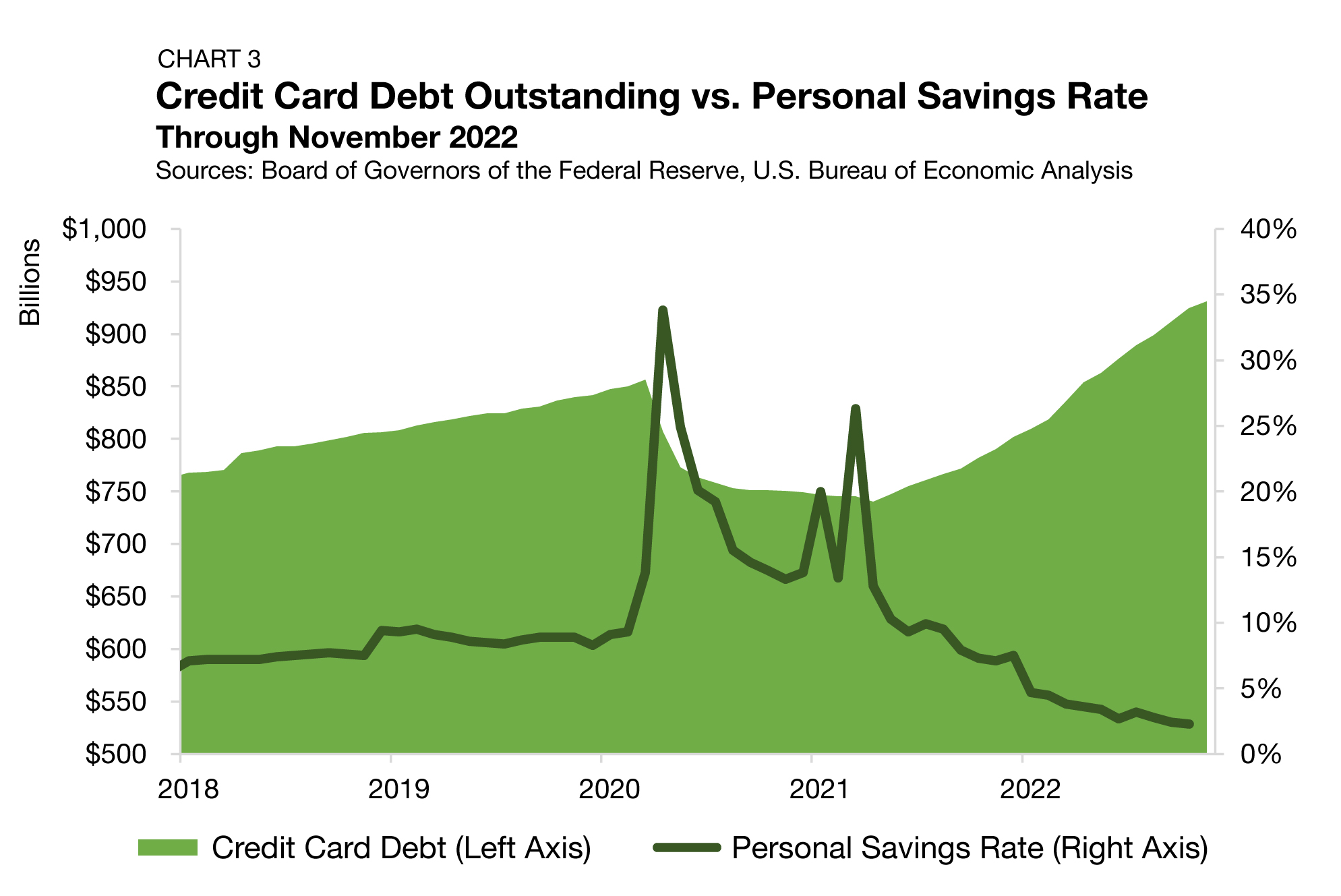

One of these significant risk factors is the sustainability of consumer activity. Thus far, despite a pervasive nervousness surrounding inflation and the economy’s year-ahead prospects, consumers have remained resilient and have not cut back on spending. Personal consumption expenditures are up through October by 7.9% from a year earlier. Even after accounting for the impact of inflation, consumption is 1.8% above last year’s levels (Chart 2).

A tight labor market and healthy levels of wage growth have, up until this point, allowed consumers to postpone a spending curtailment. The challenge is when we look at how consumers are financing current expenditures. Credit card debt is at all-time highs, and we are seeing higher levels of utilization of existing consumer credit lines even as the cost of revolving credit is significantly higher than it was one year ago. Worse, personal savings rates have dropped off dramatically, reaching their lowest levels since 2005 (Chart 3). Taking these factors together paints a picture of consumers quickly drawing down on their safety cushion resources.

Beyond the risks within our borders, we would be wise to remember that the U.S. sits inside a global ecosystem of trade, politics, climate, and epidemiology. There is no escaping the fact that the current geopolitical landscape is tense, and the potential for greater disruption is significant. If the war in Ukraine were to escalate to involve NATO coalition forces directly, implications for energy markets would be substantial. Additionally, the potential for further deterioration of trade or diplomatic relations with China also stands as a source of concern.

Rental Housing: Insulated, Not Immune

Within the market for rental housing in the U.S., the sector is uniquely positioned to withstand the unrelenting blitz of economic headwinds. Of course, many commentators are pointing to a slowdown in apartment rent growth as a sign of growing weakness. However, we do not view that as reflective of any structural change in the profile of demand or supply but rather a cyclical feature. It is normal to expect a period of slowing rent growth while there is uncertainty in the economic outlook and greater risk aversion among households.

While no asset class is immune from the challenges of higher interest rates, the presence of amortization makes the multifamily sector less likely to see mounting distress. All HUD-conforming multifamily loans are fully amortizing. Moreover, Fannie Mae- and Freddie Mac-conforming multifamily loans require at least partial amortization. Where we are most likely to see debt-related difficulties next year and beyond are with CMBS transactions. According to data from Trepp and the Mortgage Bankers Association, a majority (64.6%) of outstanding CMBS loans are categorized as interest-only over their entire term. Operators with expiring interest-only loans may run into trouble next year as they try to replace debt at roughly twice the cost. Accounting for just 10.5% of CMBS debt outstanding, the multifamily sector’s exposure to these transactions is limited. Meanwhile, the same cannot be said for the office, retail, and hotel sectors — all of which rely more on CMBS capital markets.

On the margins, subsets of mortgages in the multifamily portfolio will still require careful monitoring, especially those that originated in the years leading up to the pandemic, where over-leveraging was a re-emergent concern.

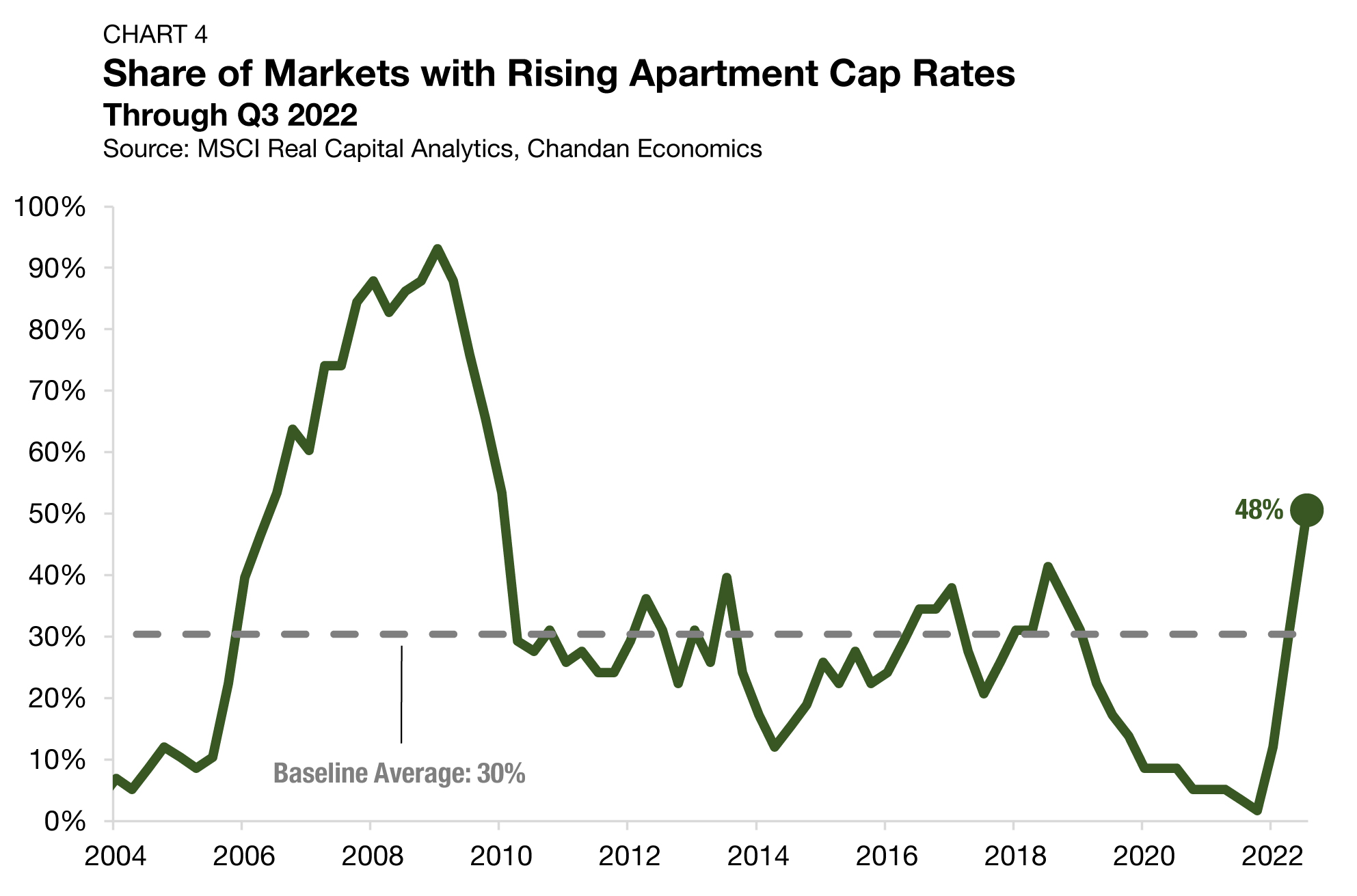

The criterion where real differences are likely to emerge over the next year is along geographic lines. According to MSCI Real Capital Analytics, through the third quarter of 2022, nearly half (48%) of U.S. markets are seeing rising apartment cap rates — the highest share since 2010 (Chart 4). We can expect that these performance trends will continue, driven by slowing business sectors and evolving migration patterns.

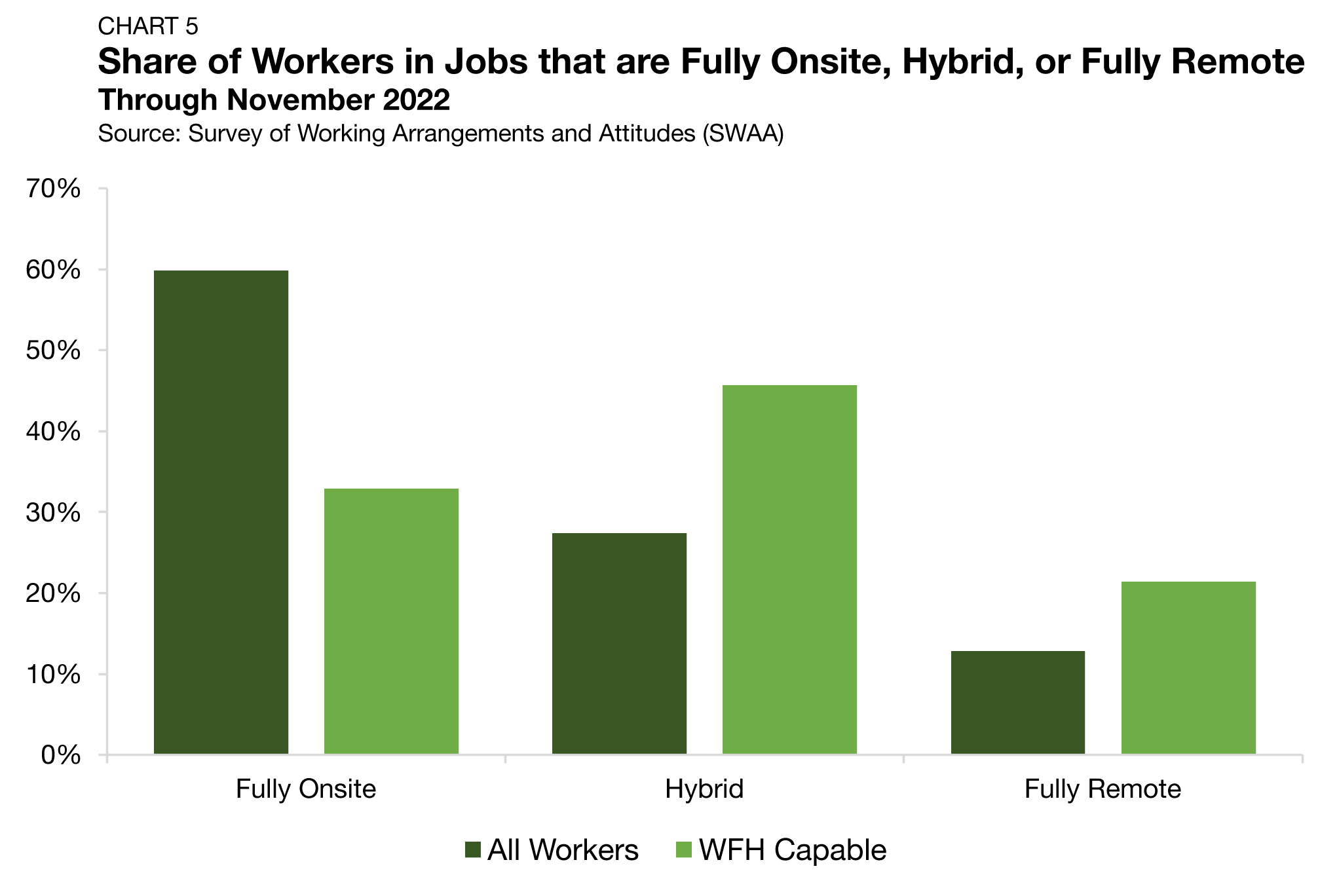

Work-from-home, a trend that seemed capable of upending the rental housing market’s appraising assumptions just a few months ago, now looks like less of a risk than initially feared. Hybrid has quickly become the dominant alternative to full onsite employment. As a result, more workers are expanding their housing search radius, though they are not un-tethering from their offices completely (Chart 5).

Among the beneficiaries of the hybrid work proliferation is a product type that was already enjoying a run of success: single-family rentals (SFR). Beyond a growing willingness of workers to locate further away from their urban offices, the SFR sector is likely to benefit from increased visibility. Although built-to-rent (BTR) communities with amenities have received less attention thus far, their demand should climb as greater awareness of this product type develops.

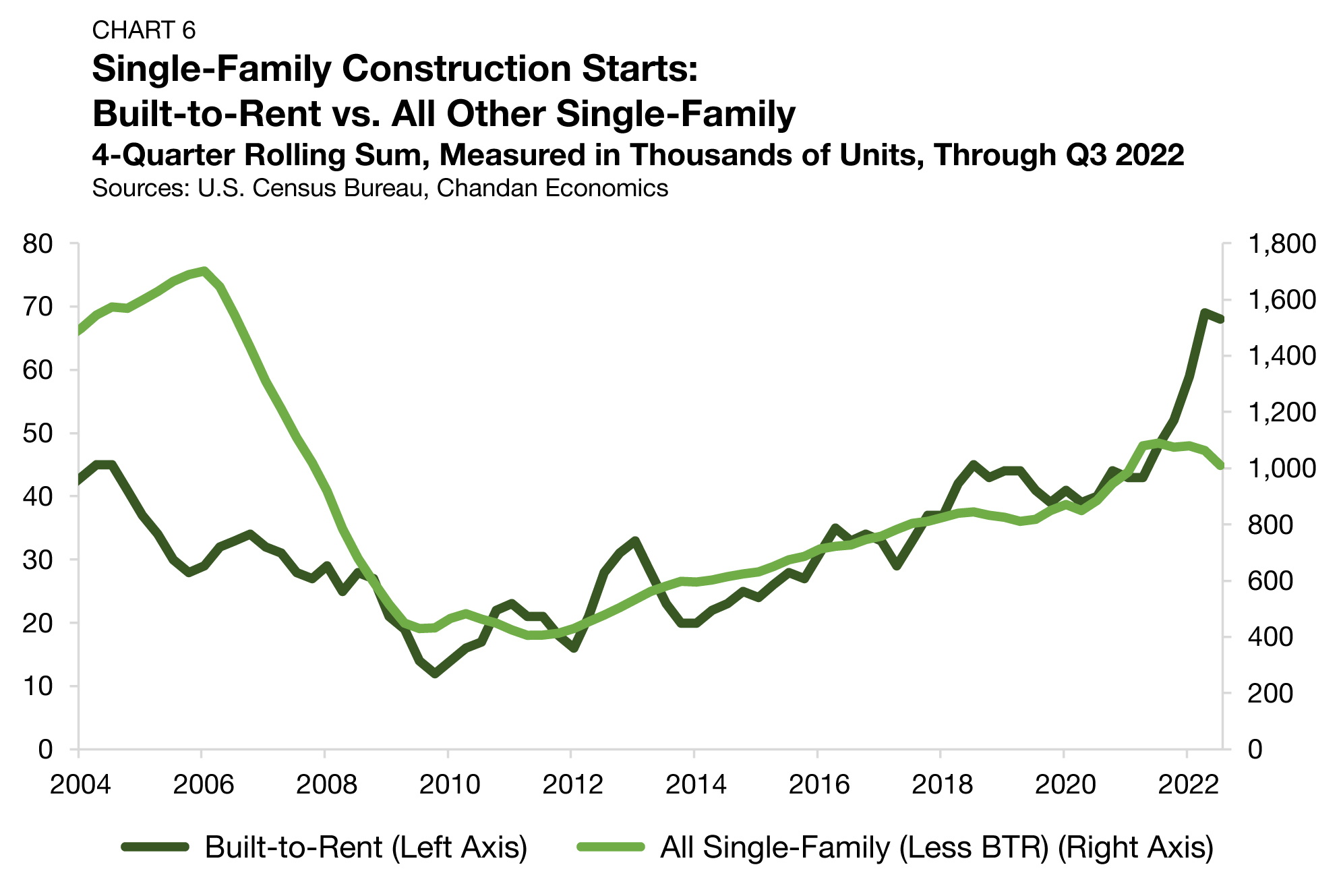

As accessibility to affordable quality housing remains a pressing challenge across the country, it is critical to note that the BTR sector is an area of growth that is adding net new homes. According to U.S. Census Bureau, BTR construction starts reached all-time highs even as the broader single-family construction landscape reached an inflection point (Chart 6). Ultimately, we see SFR/BTRs as critical alternatives in the diversification of housing opportunities for all Americans, no matter their homeownership capacity or preference.

The Road Ahead

In the months ahead, we can broadly expect a continued correction in the residential housing market, though we do not anticipate a 2008-style crisis. Mortgage underwriting standards for owner-occupied single-family homes remained tight over the past several years. Moreover, the combination of low locked-in interest rates on outstanding mortgages and relatively strong labor market conditions means that defaults and disclosures should remain limited. Of course, owners that need to sell will have no choice but to capitulate, and market clearing prices should move lower. However, many of the risk factors necessary for widespread distress in the residential housing market are simply absent.

The historically low interest rates enjoyed by existing owners are unlikely to return over the medium term. Even as the Fed eventually regains control over pricing pressures and has the rate-cutting ammunition to reintroduce monetary accommodation, it is unlikely that we will revert back to near-zero interest rates. According to the Fed’s estimates, it expects a long-run average of 2.5% for its Federal Funds Rate. If these estimates hold true, 30-year mortgage rates would remain well above levels that buyers have become accustomed to in recent years. As a result, home financing conditions will continue to support higher levels of rentership.

Undoubtedly, the current market environment contains an underlying anxiousness. This is a moment of accelerated change both in our industry and throughout the economy, and we will not make it to our final destination without some in-flight turbulence. All signs point to the economy entering the early stages of a contraction. However, the big difference between this moment and the housing bubble we saw in the 2000s is that housing in the U.S. today is undersupplied, not oversupplied. While the rental housing sector will not be immune from challenges along the way, it sits in a position of strength to withstand the ongoing storm.

For more research and insights, visit arbor.com/articles

Disclaimer All content is provided herein “as is” and neither Arbor Realty Trust, Inc. or Chandan Economics, LLC (“the Companies”) nor their affiliated or related entities, nor any person involved in the creation, production and distribution of the content make any warranties, express or implied. The Companies do not make any representations regarding the reliability, usefulness, completeness, accuracy, currency nor represent that use of any information provided herein would not infringe on other third party rights. The Companies shall not be liable for any direct, indirect or consequential damages to the reader or a third party arising from the use of the information contained herein.