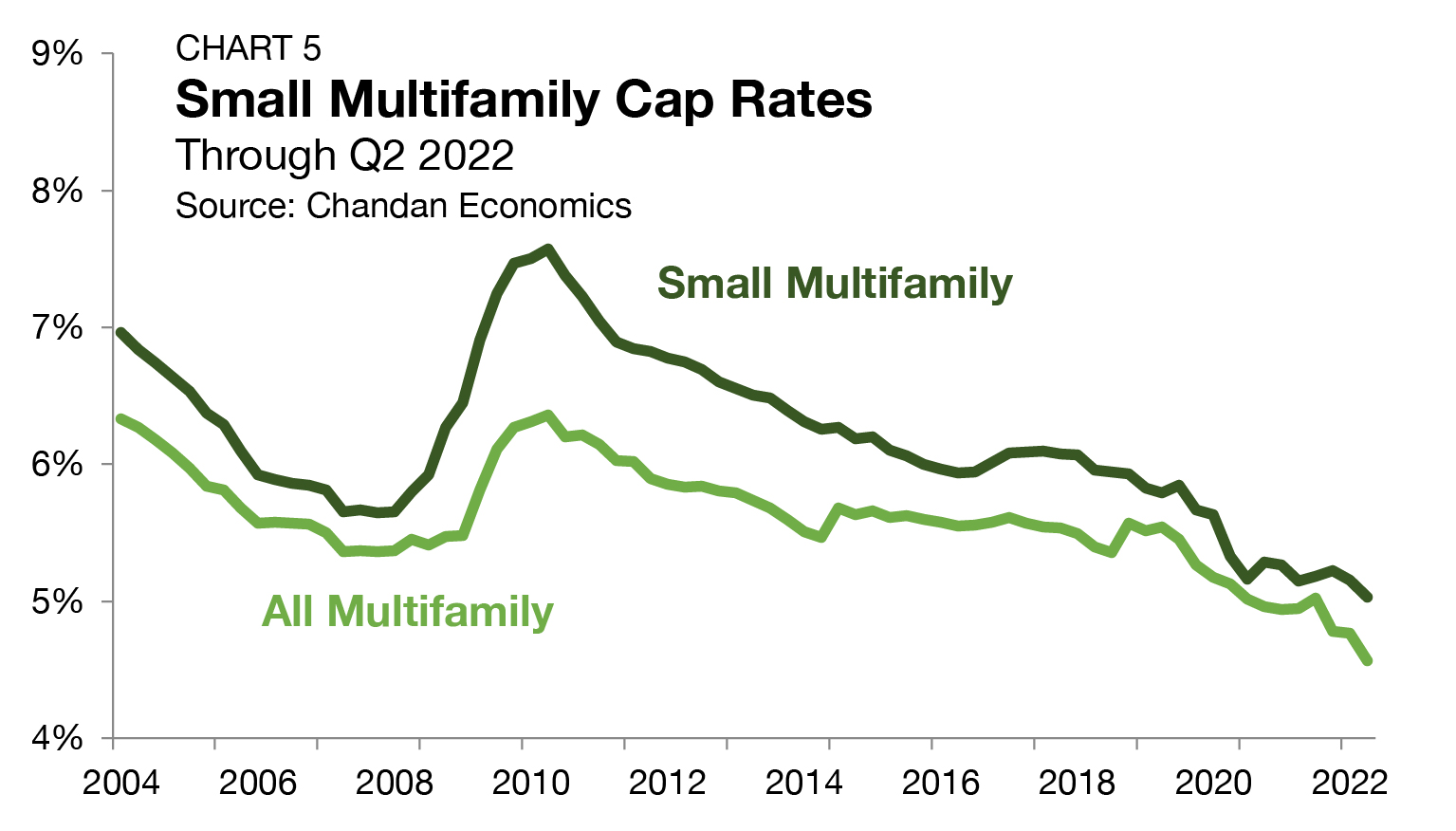

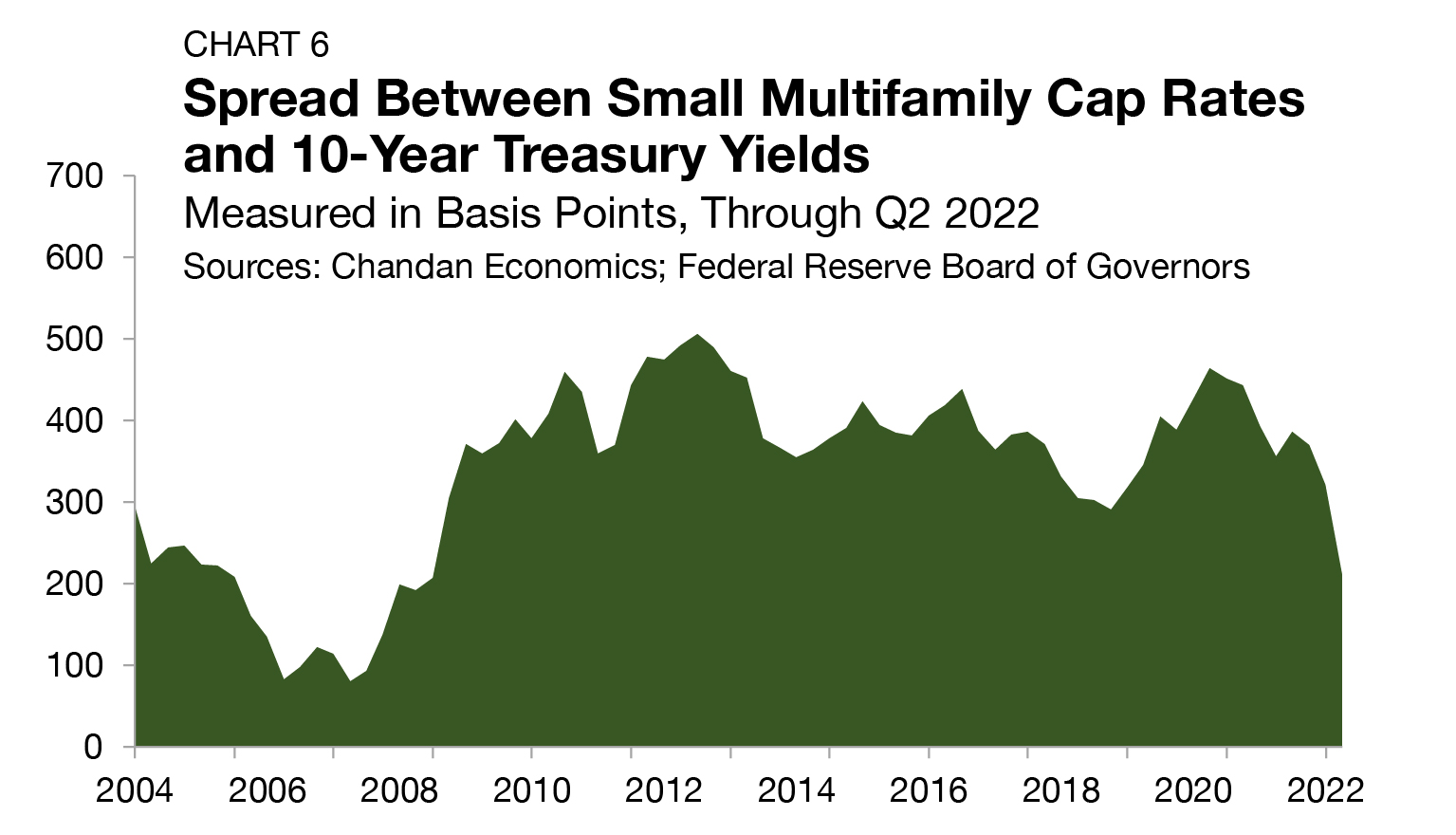

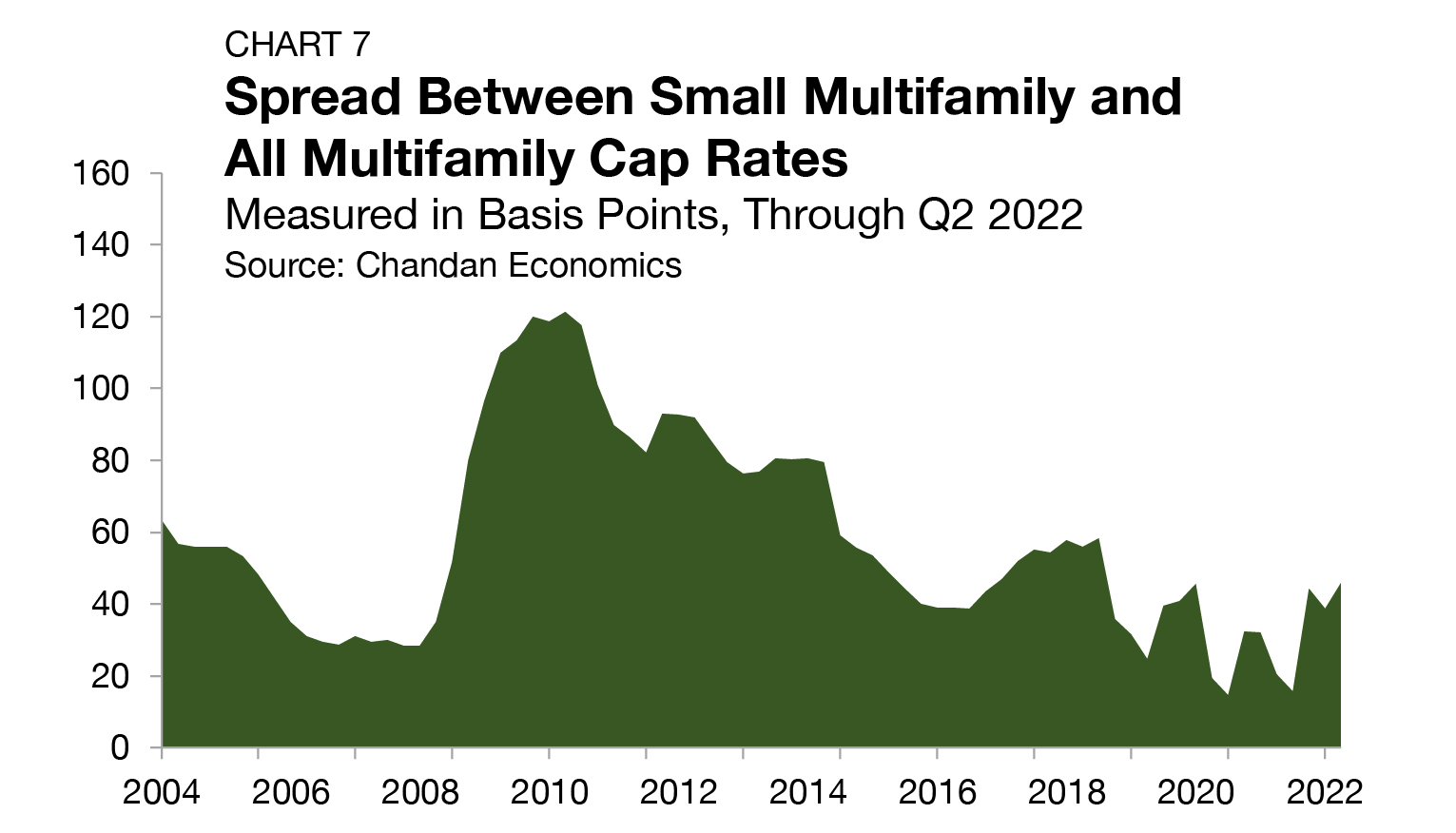

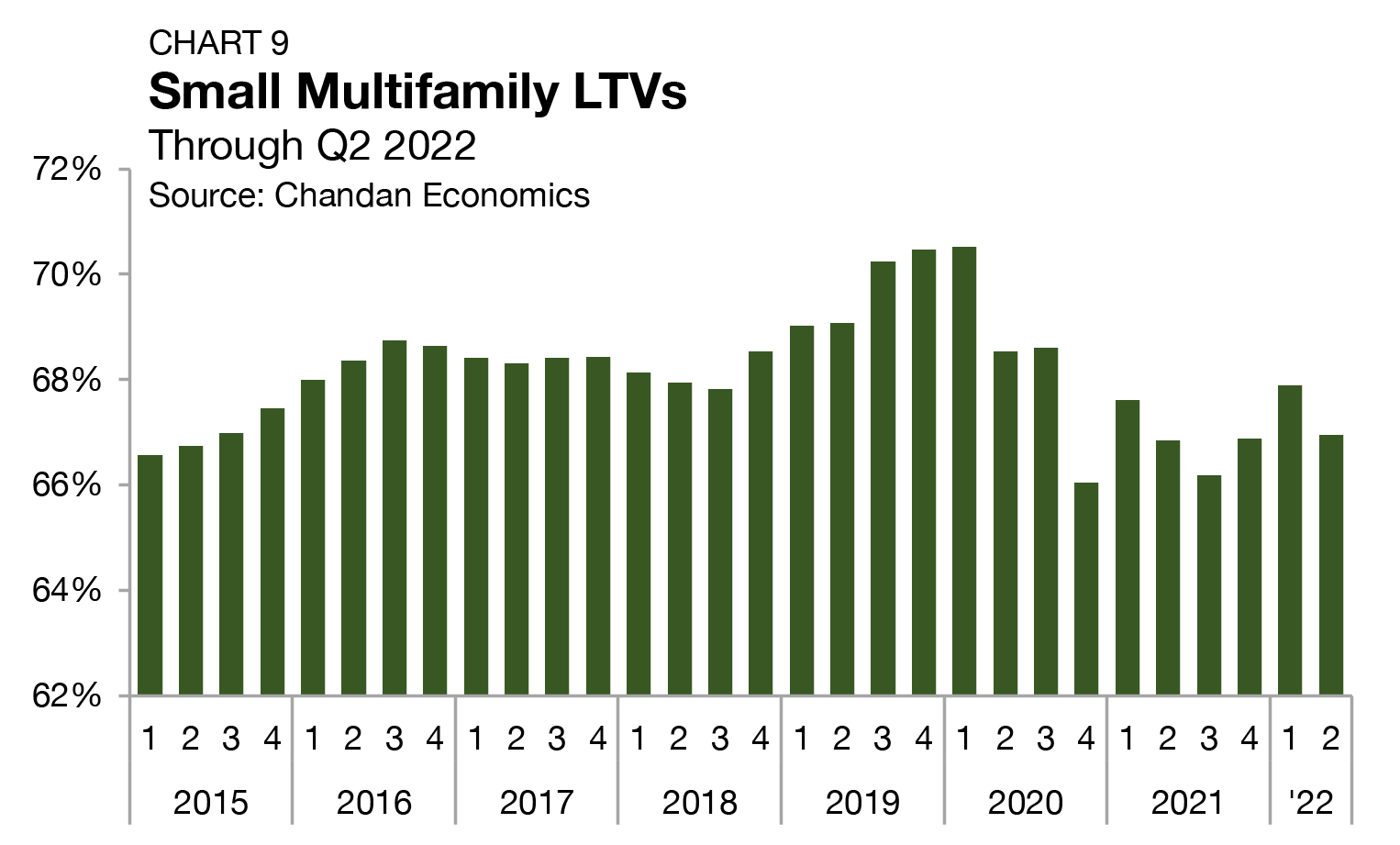

Current Reports

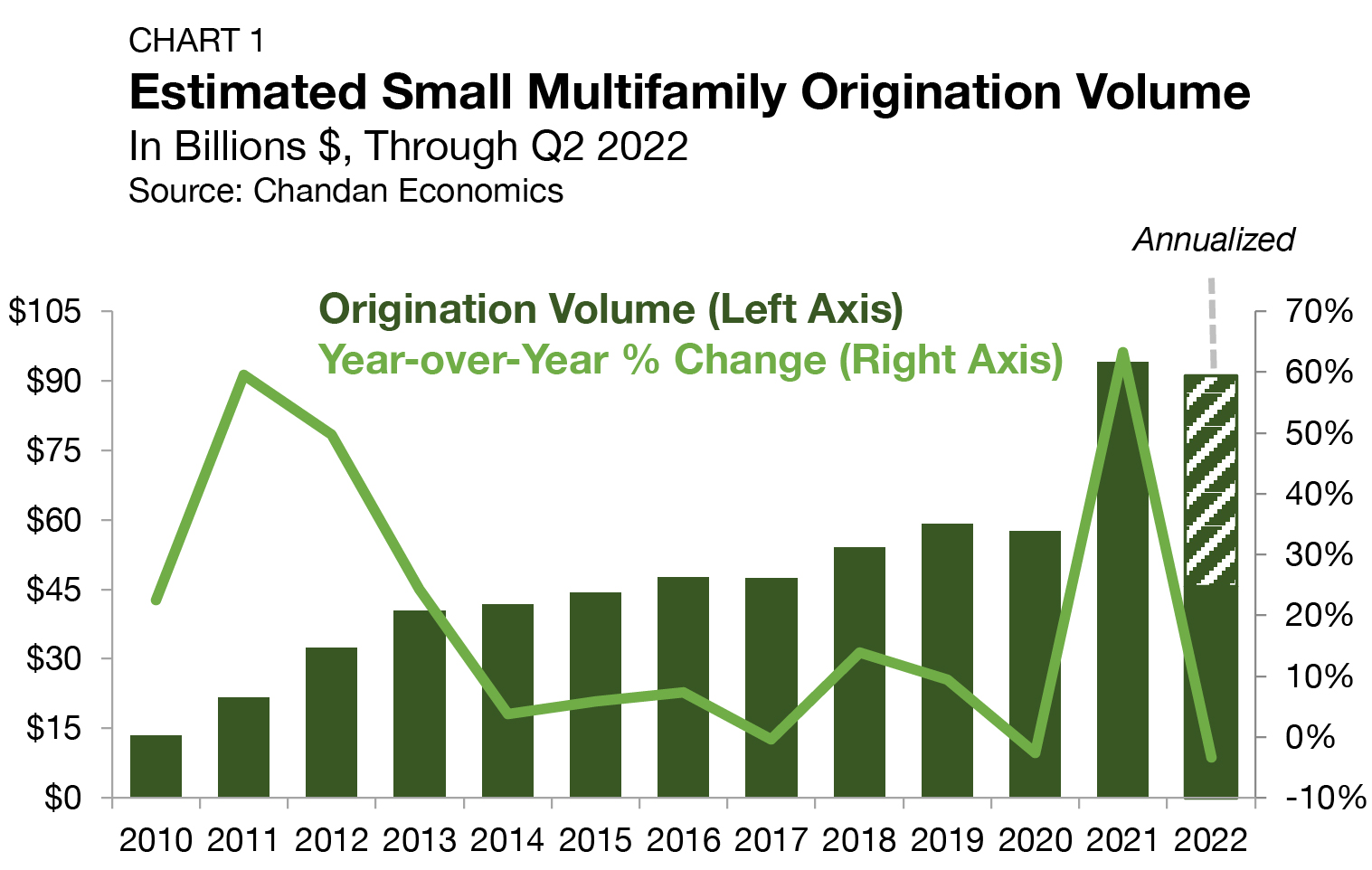

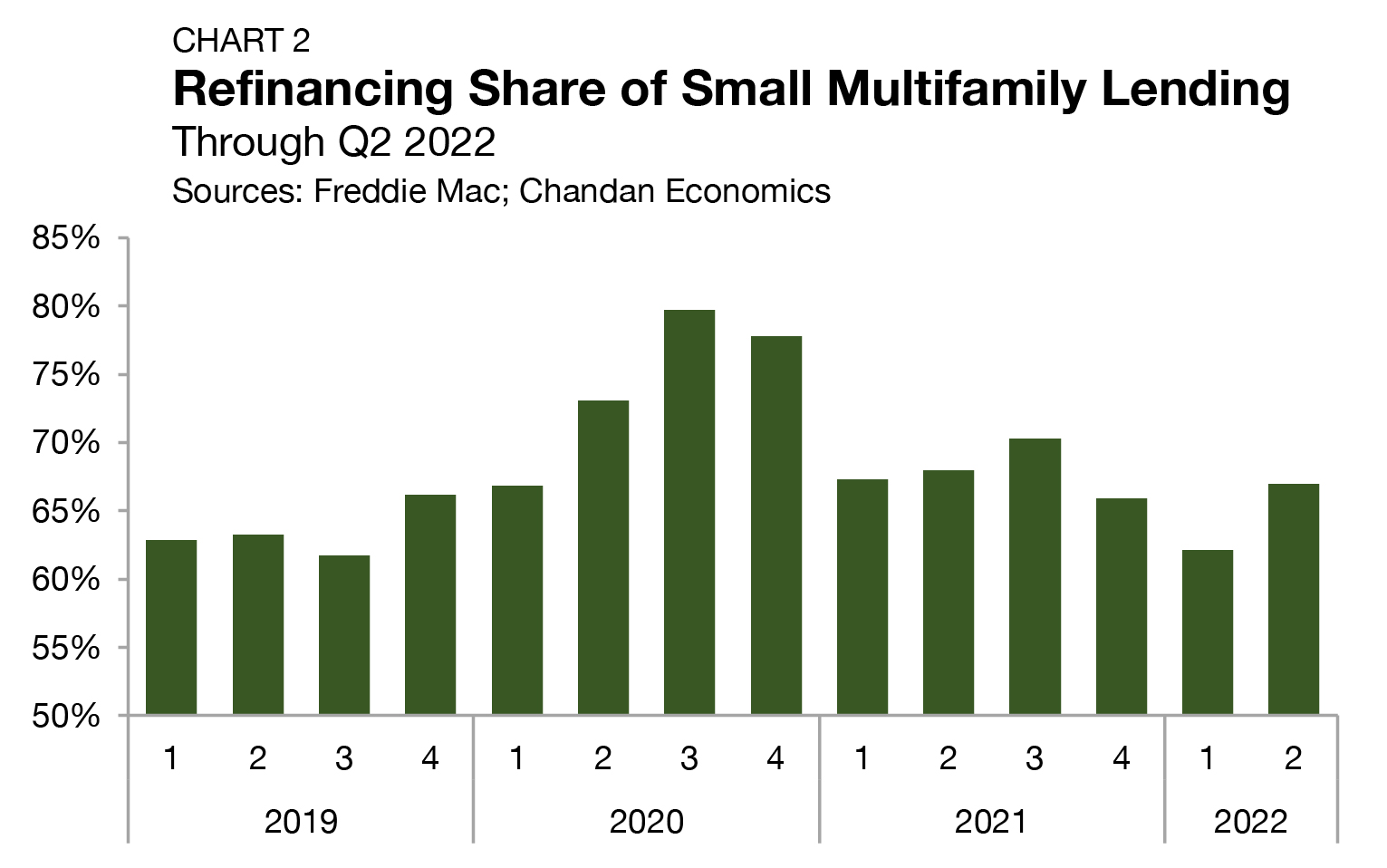

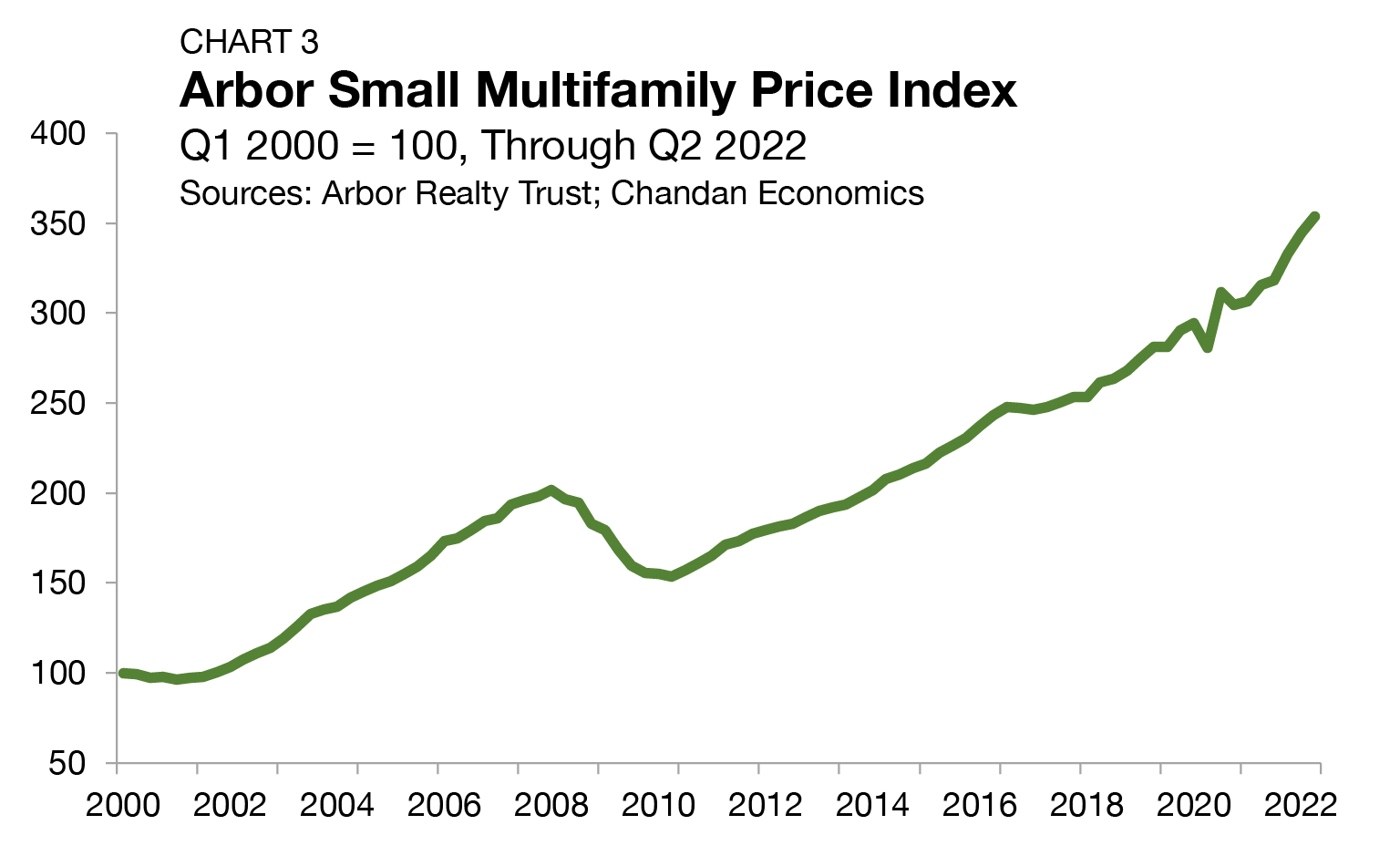

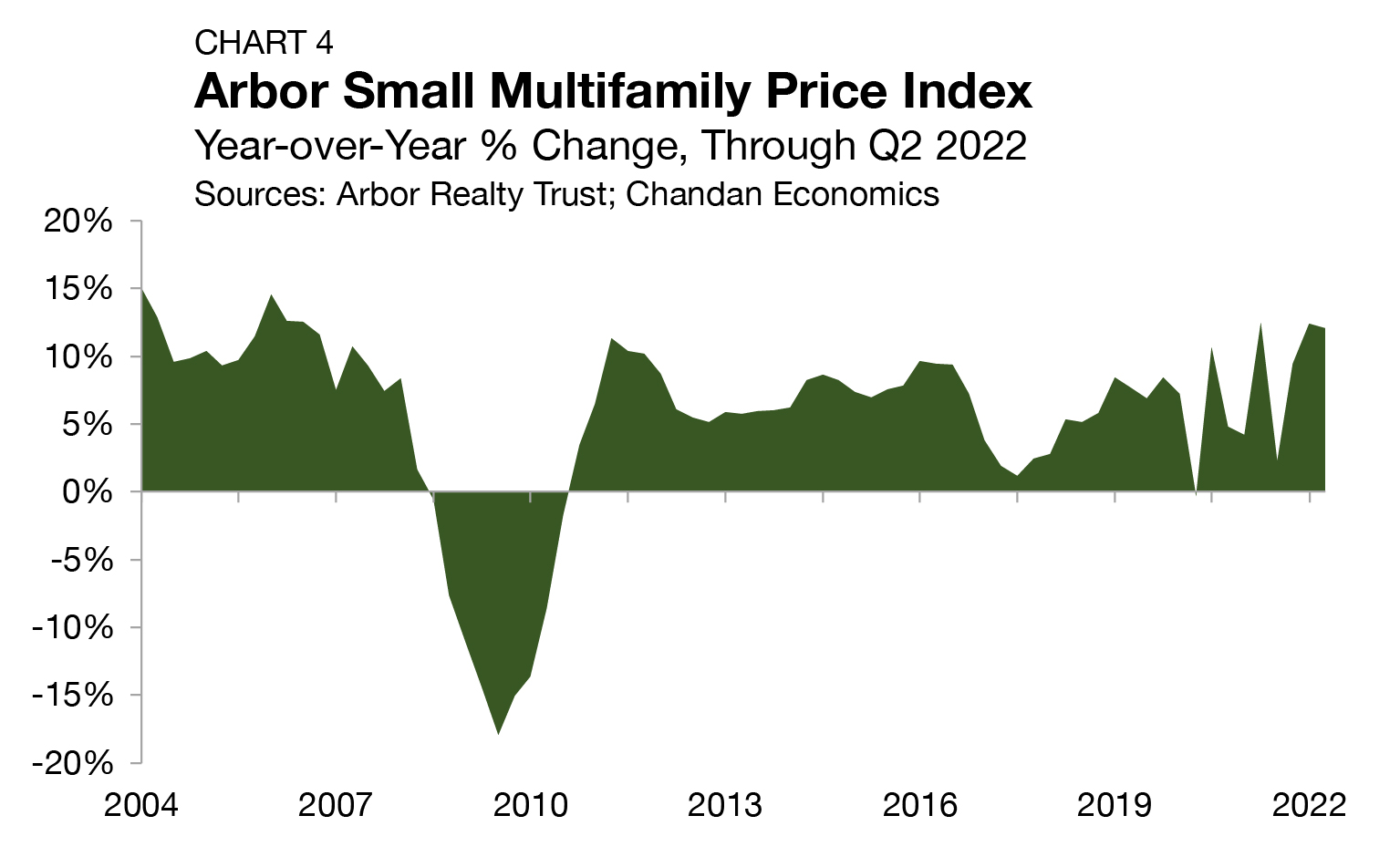

Arbor Realty Trust’s latest Small Multifamily Investment Trends Report, developed in partnership with Chandan Economics, evaluates what’s driving this sector’s ongoing stability as macroeconomic conditions remain mixed. Loan originations rose last quarter, and valuations are rebounding, signaling that normalization is taking hold.

Analysis

Over the past 12 months, the leading rent growth markets spanned multiple regions, each exhibiting distinct strengths and characteristics.

Articles

Labor market conditions are a foundational driver of rental housing demand, influencing tenant stability and household growth. While the national pace of hiring has moderated, the economies of many metropolitan areas continue to outperform. Expanding on Arbor’s latest Top Markets for Multifamily Investment Report, our research teams highlight the local dynamics supporting growth in several of the country’s strongest-performing multifamily markets.

Analysis

The U.S. multifamily sector continued to build momentum at the start of 2026. Rent growth moved into positive territory, and a moderating construction pipeline showed that vacancy may have reached its cycle peak.

Articles

Arbor’s track record of top finishes across multifamily agency rankings reflects the depth of our financing capabilities, the strength of our industry partnerships, and our disciplined, detail-driven approach to execution. Longstanding relationships with Fannie Mae, Freddie Mac, and the Federal Housing Administration (FHA) — built over many years of close collaboration — enable our team to deliver strong borrower outcomes across market cycles, reinforcing Arbor’s position as one of the top multifamily lenders in 2025.

Articles

Senior renters are increasingly choosing multifamily housing, with more than half now living in these rental properties, according to new data from the U.S. Census Bureau’s American Community Survey. Where they live — both by property type and by metropolitan area — provides insight into how housing preferences, local market conditions, and migration patterns shape rental housing demand.

FREDDIE MAC® Conventional Small

Articles

Arbor is proud to have planted thousands of trees in the past 40 years – nearly 22,000 in the past five years alone – and we’re still going strong. Since day one, Arbor’s focus on community-building, which grew from the forward-thinking vision of Chairman, CEO, and President Ivan Kaufman, has defined the company’s direction and driven its philanthropic activities.