Articles

The single-family rental (SFR) sector continued to demonstrate resilience through early 2026, supported by stable occupancy, positive rent growth, and improving capital markets activity.

The single-family rental (SFR) sector continued to demonstrate resilience through early 2026, supported by stable occupancy, positive rent growth, and improving capital markets activity.

In his latest Arbor Realty Trust video, Dr. Sam Chandan, a leading commercial real estate scholar, shares his insights into the findings of our latest Top Markets for Multifamily Investment Report, developed in partnership with Chandan Economics. The noted NYU professor outlines the market-level results of the Arbor-Chandan Opportunity Matrix, which spotlights multifamily markets that offer optimal value to commercial real estate investors.

Generation Z’s potential for household formation could soon reshape many U.S. metropolitan areas. From McAllen, TX, to Hartford, CT, explore the top multifamily markets where rental demand is set to rise as Gen Z leaves the nest.

Indianapolis ranked as the top multifamily investment market in the U.S., in the latest Top Markets for Multifamily Investment Report from Arbor Realty Trust and @Chandan Economics. The market has been supported by strong labor market conditions, tight occupancy levels, and a favorable affordability profile.

Arbor Realty Trust colleagues mentored more than 50 students this spring during two Project Destined programs designed to provide young professionals with insight into the inner workings of commercial real estate.

The latest Single-Family Rental Investment Trends Report from Arbor Realty Trust, developed in partnership with Chandan Economics, examines a commercial real estate sector that has proved to be both stable and resilient. Supported by strong occupancy, positive rent growth, and loosening capital markets, SFR remains firmly grounded on a path of steady growth.

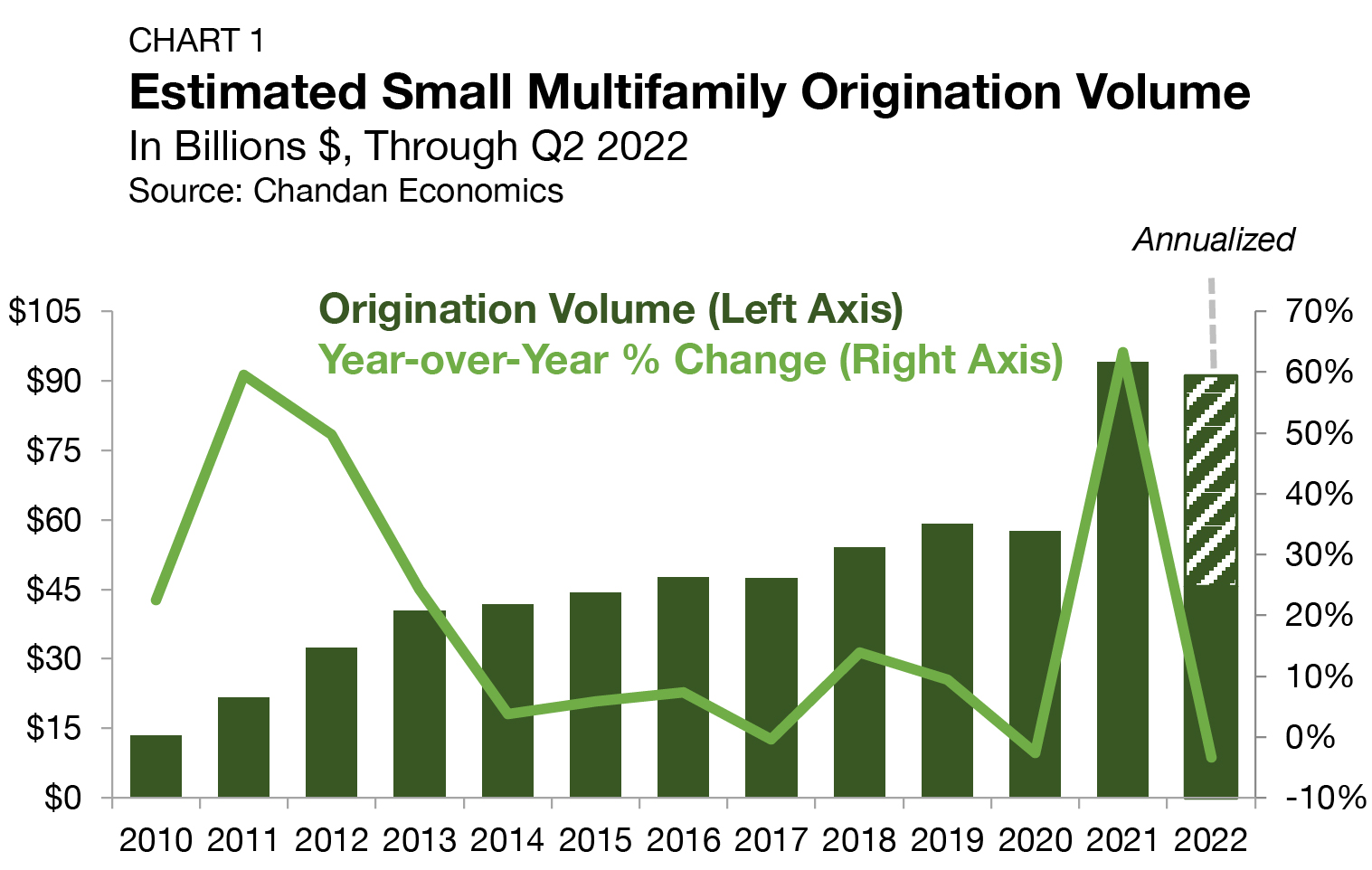

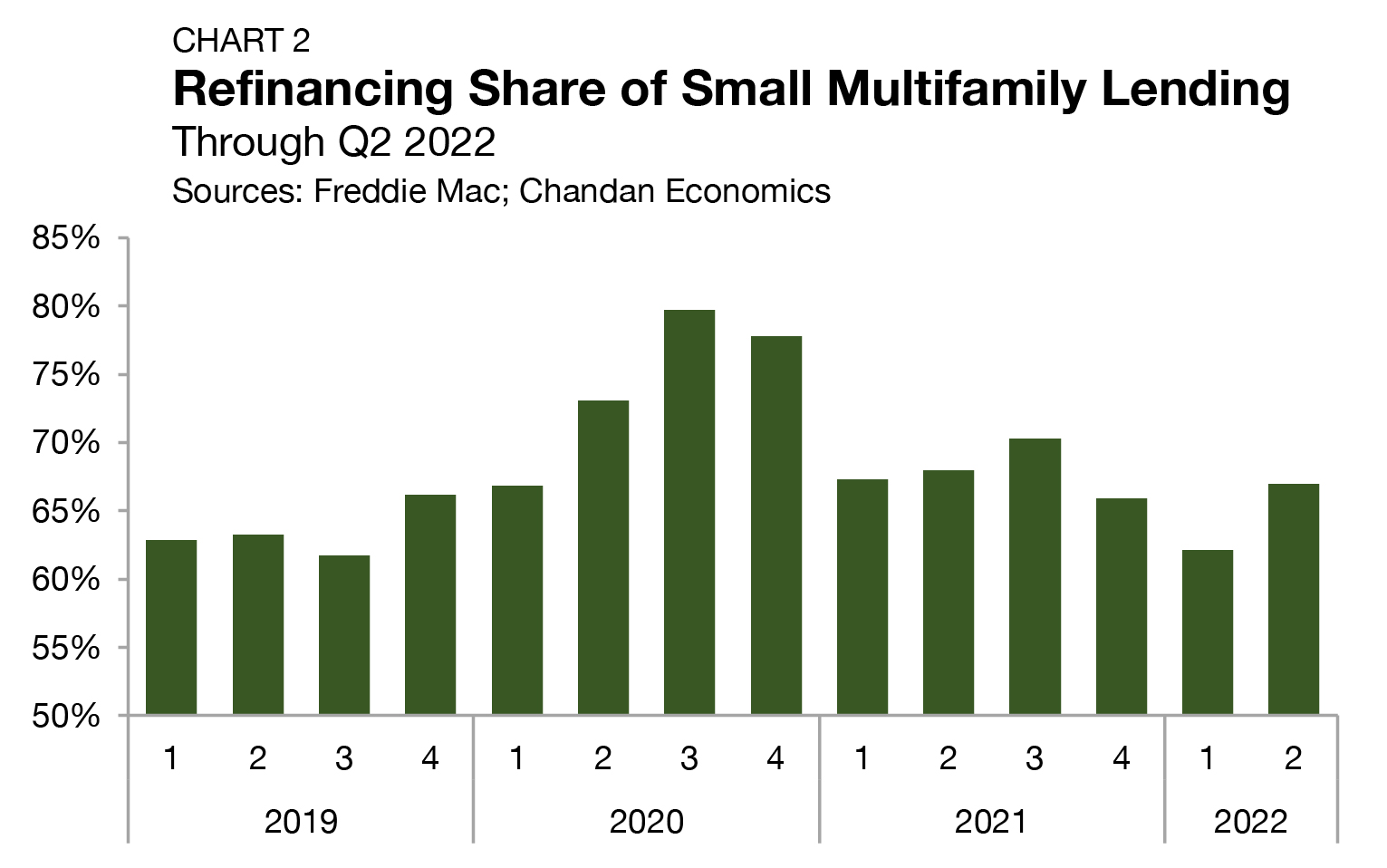

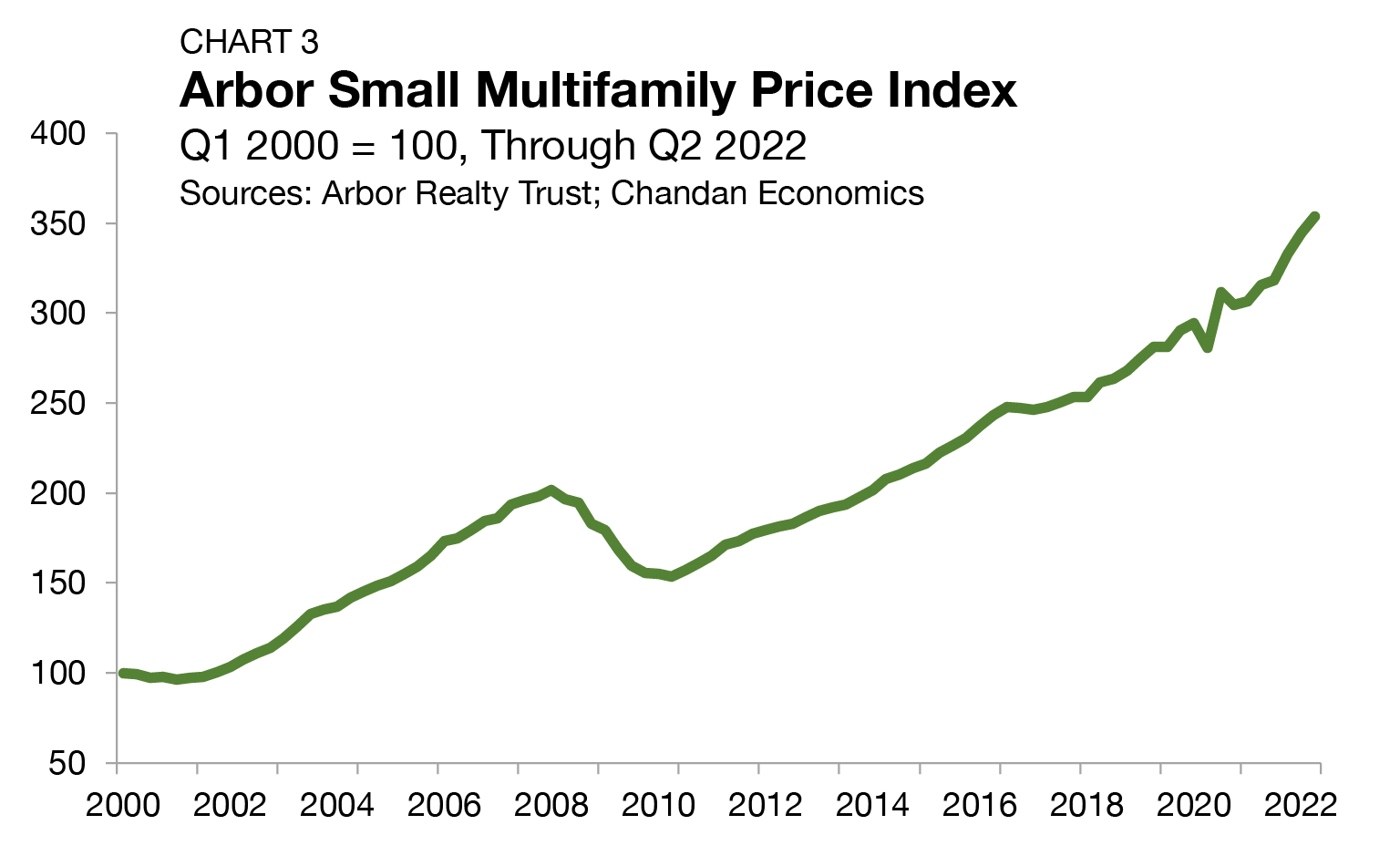

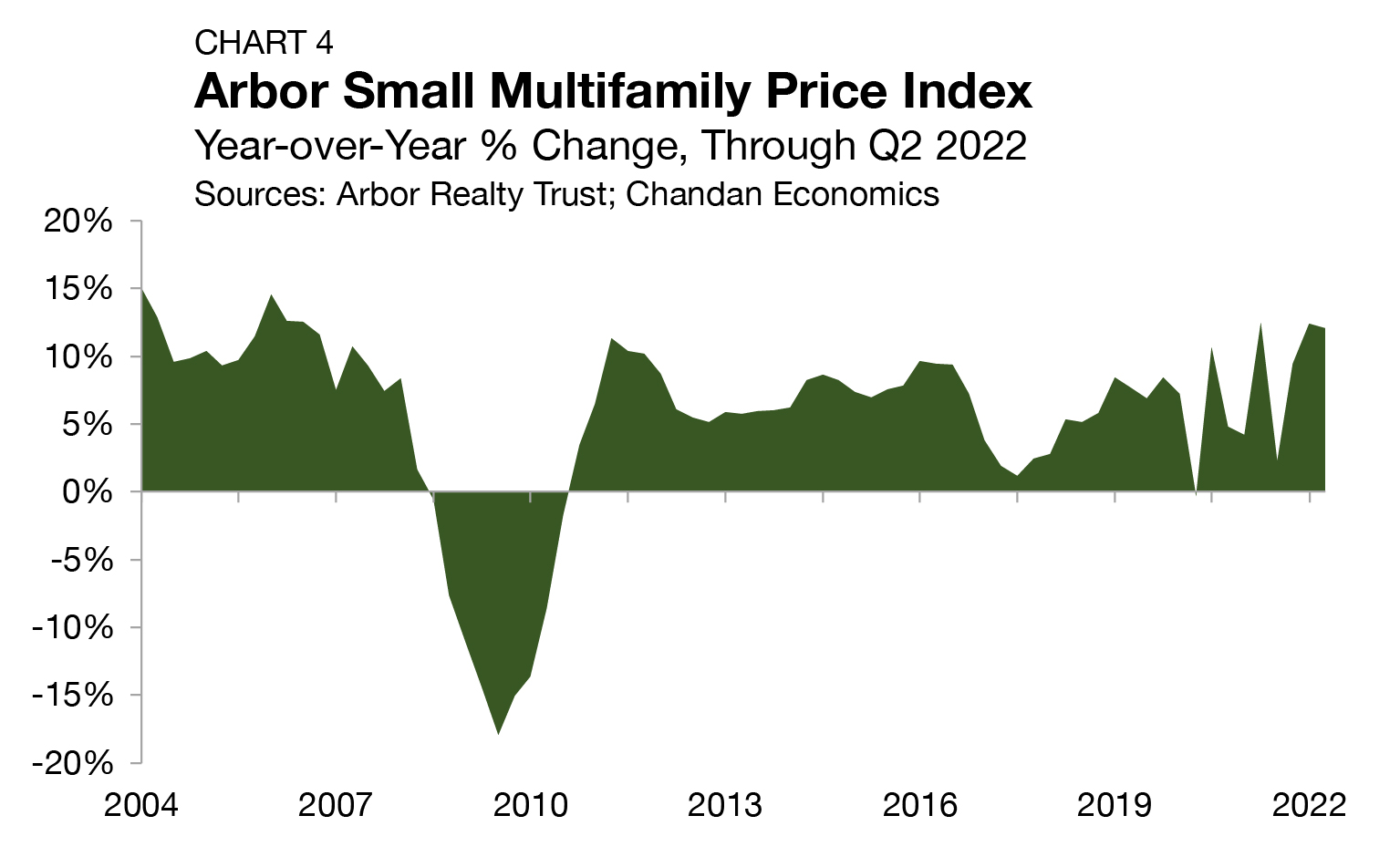

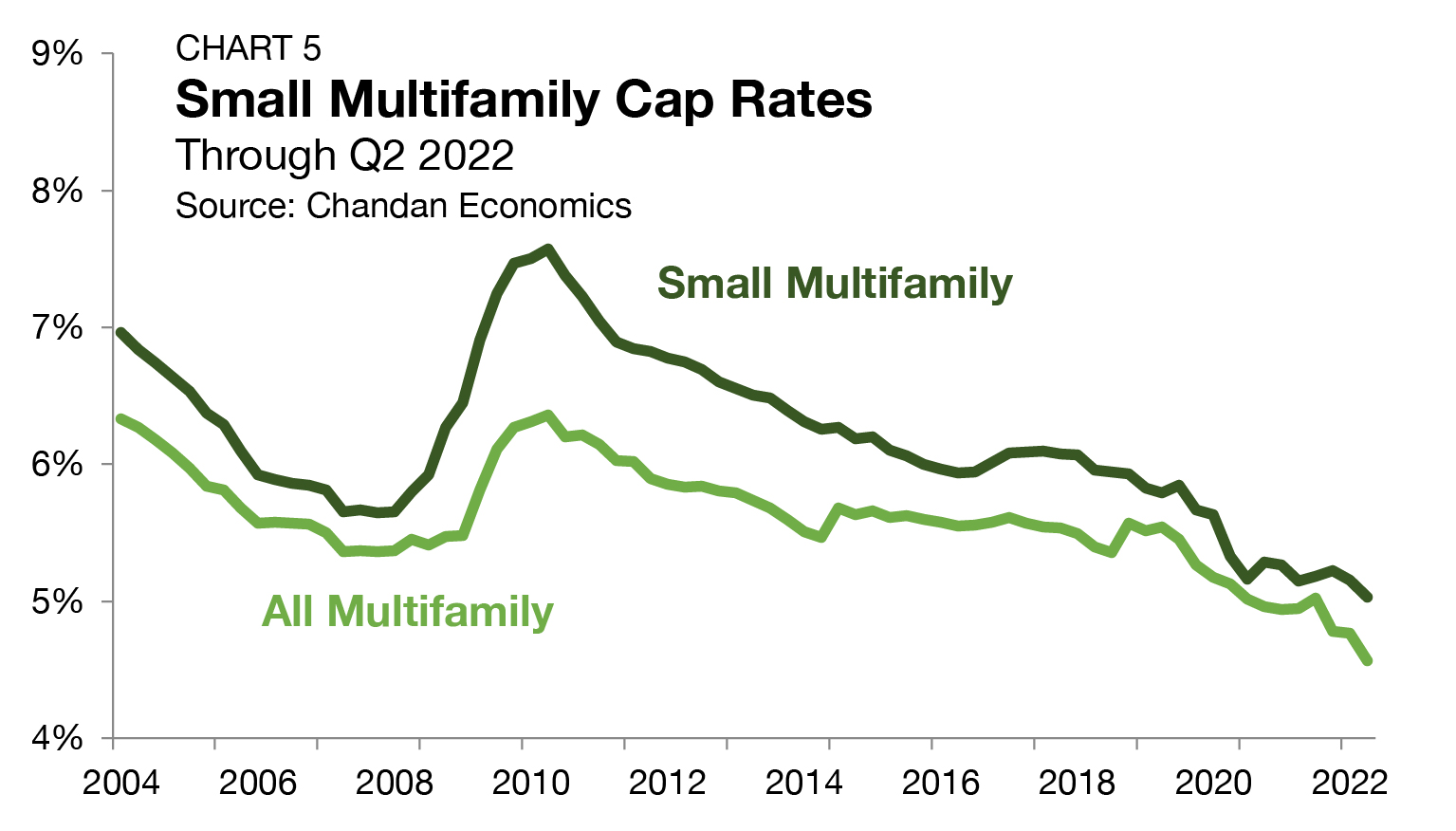

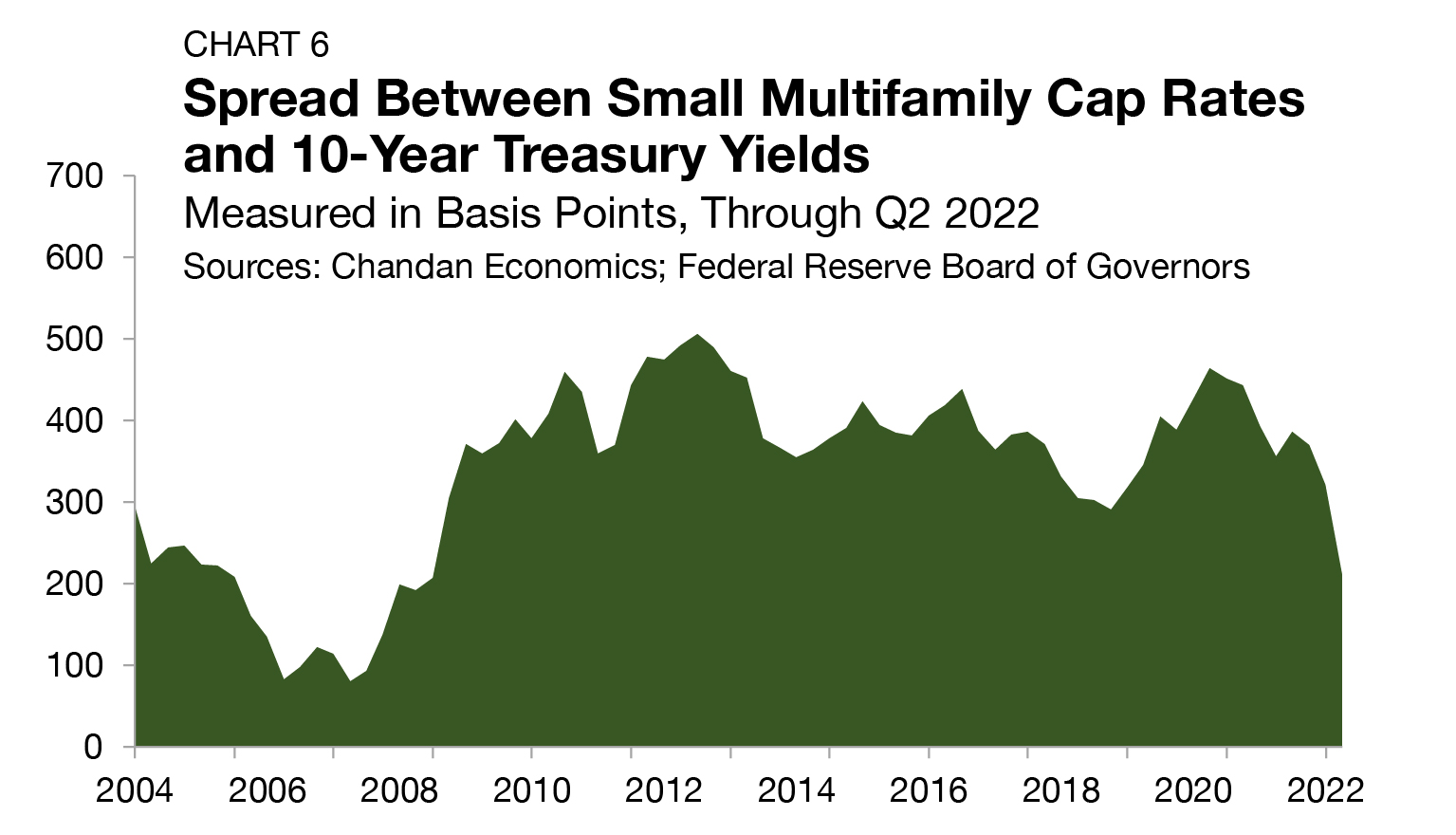

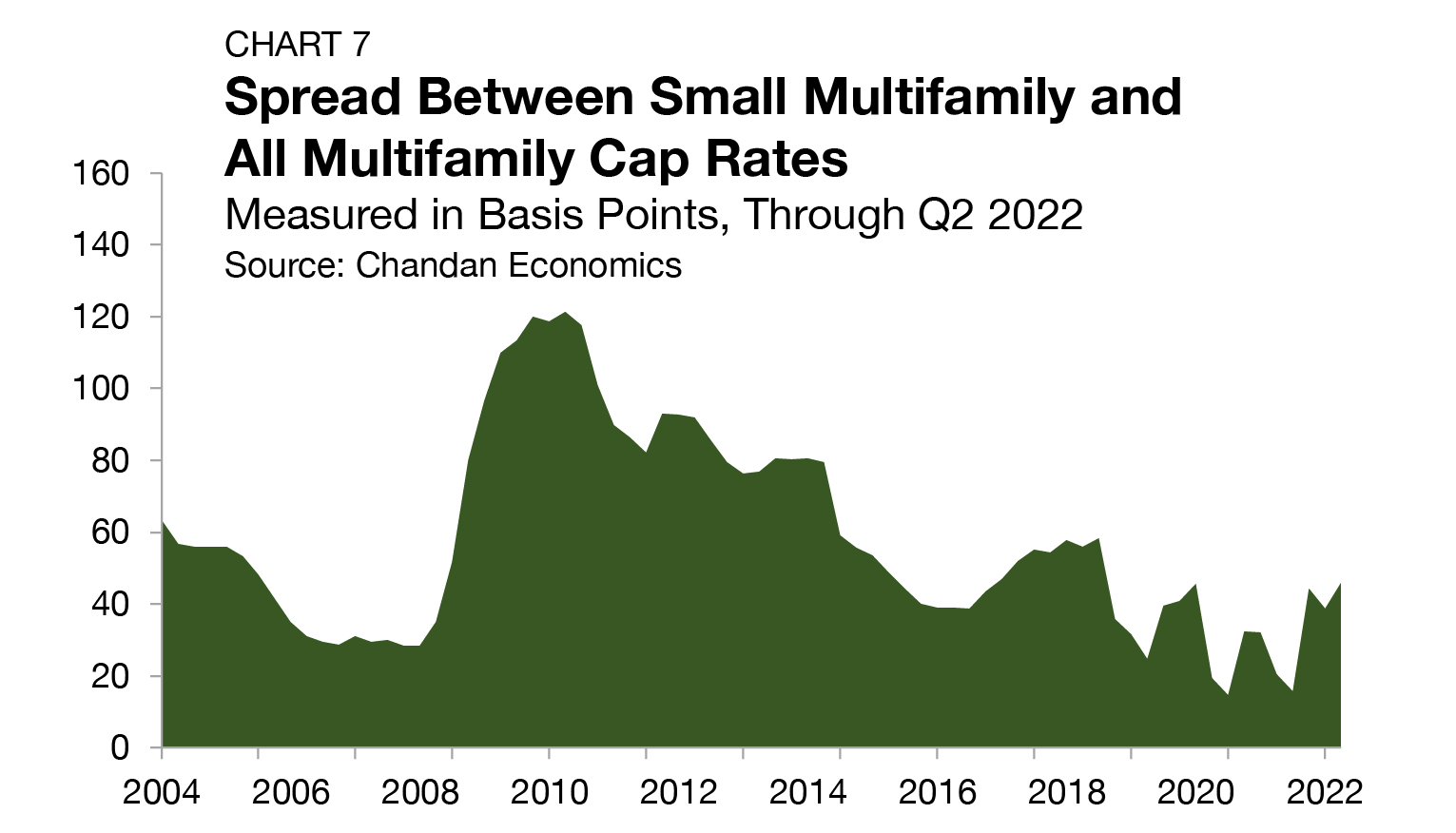

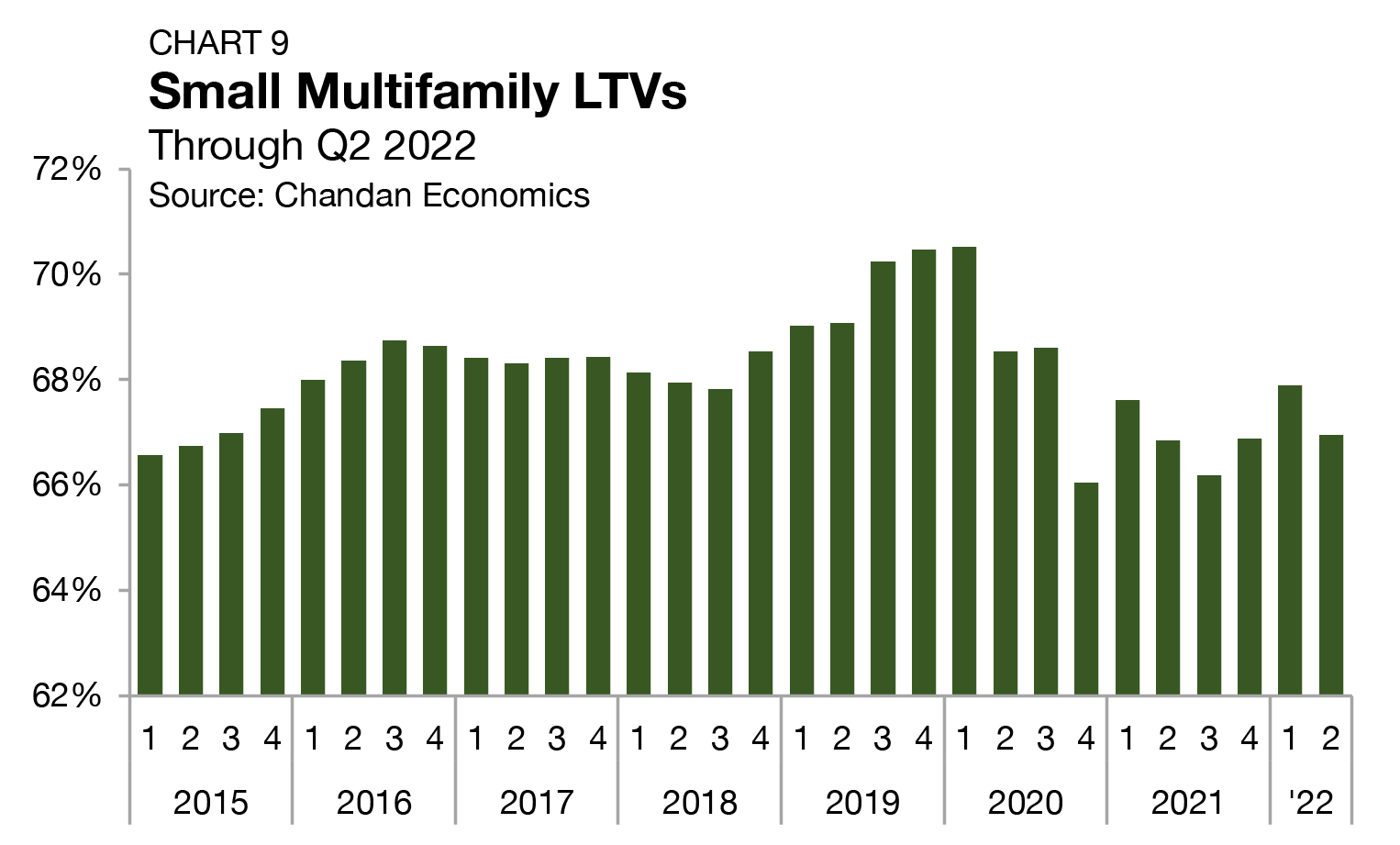

The small multifamily sector entered 2026 on a strong note, even as lending conditions remained shaped by persistently high interest rates and regulatory uncertainties.

As the single-family rental (SFR) sector has matured, build-to-rent (BTR) has become a key source of new supply. Purpose-built rental communities are absorbing demand from households seeking the space and privacy of single-family living without the financial or lifestyle commitments of homeownership. Newly released U.S. Census Bureau data show that while SFR/BTR construction continued to decline from its 2024 peak through year-end 2025, development activity remains elevated compared to historical norms.