Emerging Multifamily Trends for 2026

- The multifamily sector remains a strong long-term bet, even in high-supply markets.

- Bipartisan support, at all levels of government, has boosted the affordable housing sector’s investment profile.

- Investors are leaning toward diversified, yield-stable segments, like single-family rentals (SFRs) and workforce housing.

Rental housing’s long-term investment outlook remains head and shoulders above its peers, driven by structural supply constraints and steady demand growth, finds the 2026 Emerging Trends in Real Estate report. Explore this trend and other key takeaways from the 47th edition of Urban Land Institute (ULI) and PwC’s influential industry report.

Key Takeaway #1: Multifamily is a Strong Long-Term Bet

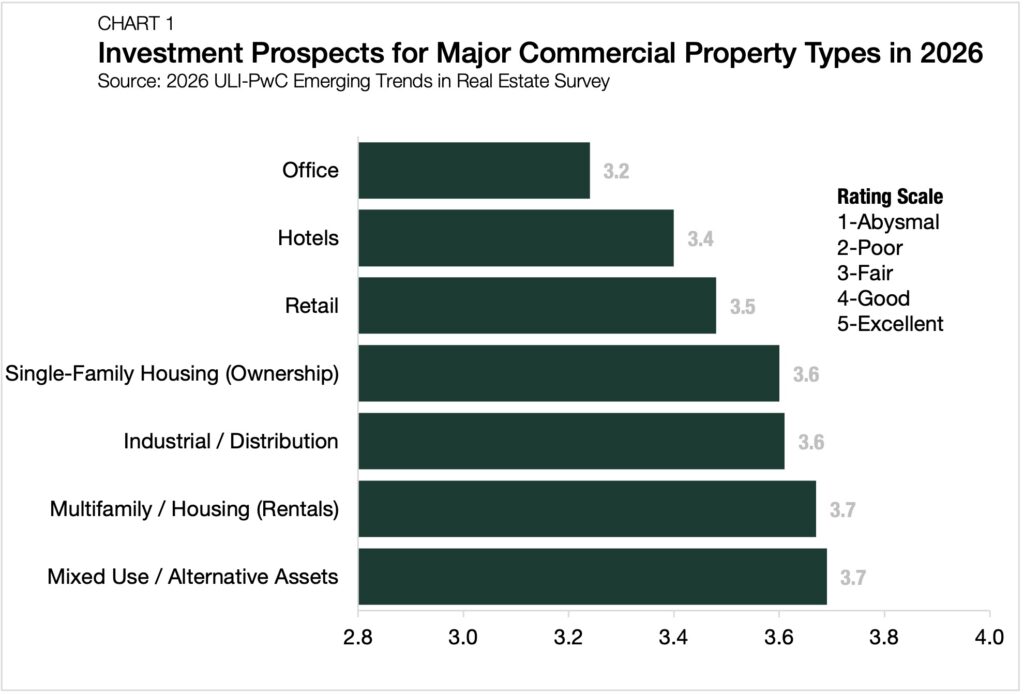

The multifamily real estate sector remains a favored asset class in the U.S., thanks to enduring renter demand and chronic underbuilding. Compared to other core commercial real estate property types, multifamily has the highest-rated investment prospects heading into 2026 (Chart 1). The only asset type rated higher is mixed-use/alternative property types, which include data centers.

While optimism persists for 2026, recovery will likely progress at a measured pace. The report notes that investors have been navigating thin yields and limited deal flow amid decelerating supply and demand. With multifamily starts having fallen by about 40% between 2023 and 2025, moderating development pipelines will influence vacancies and rent growth next year. At the same time, lower immigration levels will slow housing demand. Still, commercial real estate investors continue to pursue multifamily, which has a long-term investment profile “head and shoulders above other property types.”

As optimism builds nationally, next year’s recovery is likely to be defined by regional unevenness. Orlando, Austin, Miami, Nashville, and Phoenix were mentioned as markets where the rental housing supply could rise by 4% to 5% in 2026 and 2027, potentially slowing rent growth. However, many of these markets remain strong long-term bets because they have dynamic labor markets and robust population inflows.

Key Takeaway #2: Bipartisan Support for Affordability Boosts Investment Profile

The national affordability crisis has brought together lawmakers from both sides of the aisle and at all levels of government. The 2025 federal tax bill included several supportive affordable housing features, such as an extension of the Opportunity Zones program, increased funding for Low-Income Housing Tax Credits (LIHTC), and a rule change designed to improve LIHTC utilization.

The ULI-PwC report also identified other policy measures state and local governments are using to boost long-term housing supply, including:

- Tax abatements

- Facilitating adaptive reuse projects

- Zoning reforms

- Streamlining the permitting process

In the past year, over 400 pro-housing bills were introduced to state legislatures, with more than 100 signed into law, according to the National Council of State Housing Agencies.

The localized political response to housing affordability has spread nationally as migration patterns skew toward smaller, less costly metros where housing remains attainable. However, as smaller metros become more popular destinations, demand is accelerating faster than supply, adding to affordability pressures.

Looking ahead, the U.S. will need to construct another 4.3 million rental homes by 2035 to keep pace with rising demand, according to National Multifamily Housing Council.

Key Takeaway #3: Investor Interest in SFR and Workforce Housing Grows

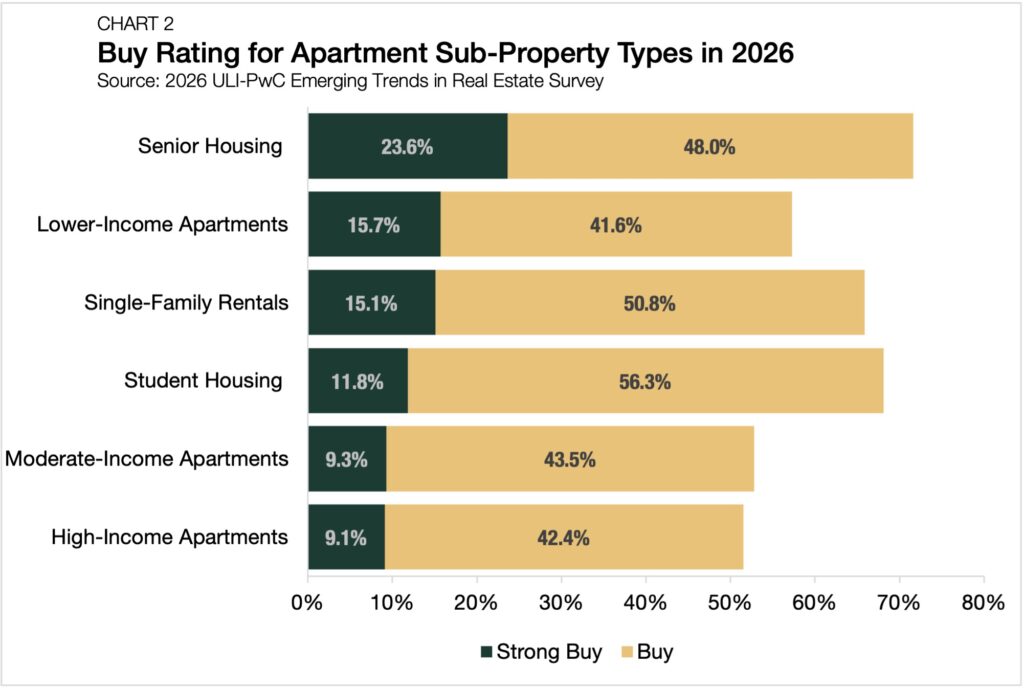

While traditional multifamily assets continue to anchor most institutional portfolios, the ULI-PwC report also highlights a growing shift among investors toward single-family rental, workforce, and senior housing as durable, long-term plays (Chart 2).

Among core residential property types, SFR now commands a larger institutional allocation (1.1%) than manufactured housing, data centers, and senior housing combined. Investors are drawn to SFR’s countercyclical resilience, particularly as affordability pressures keep would-be homebuyers in the rental market.

Workforce and attainable housing also stand out as priority segments for capital deployment. Frequently, institutional investors seek exposure to markets where rents are between 60% and 100% of area median income (AMI), positioning the assets as both socially impactful and financially defensive.

Simultaneously, senior housing has reemerged as a growth sector after several challenging years, with Baby Boomers, a key driver of long-term demand, expected to surpass 80 million by the end of the decade.

The Bottom Line

Industry experts remain bullish on rental housing demand heading into 2026, as demographic trends and home purchase affordability pressures improve multifamily’s investment profile. Although affordability will continue to challenge communities, change is in store for the new year as investors’ interest in SFR, workforce, and senior housing builds.

Interested in the multifamily real estate investment market? Contact Arbor today to learn about our array of multifamily, single-family rental, and affordable housing financing options or view our multifamily articles and research reports.