Multifamily Completions Shift to Larger, Lower-Rise Properties

- Multifamily completions moderated from historic highs in 2025 after a record-setting 2024.

- Despite the decline, large multifamily properties accounted for 59.4% of completed multifamily units in 2025, continuing the sector’s long-term shift toward 50-plus-unit buildings.

- Larger does not necessarily mean taller: 60.5% of completed multifamily units were in buildings with fewer than four floors in 2025, consistent with the sustained role of lower-rise multifamily supply.

Evolving housing demand and household preferences are influencing both the layout and density of new multifamily development. Utilizing data from the U.S. Census Bureau’s Annual Survey of Construction, Chandan Economics and Arbor Realty Trust examine how the characteristics of new multifamily properties continue to change. This year’s data show that while multifamily completions moderated from 2024’s elevated pace, the sector’s shift toward larger properties continued. At the same time, larger has not necessarily meant taller, as lower-rise buildings continue to account for most new multifamily completions.

Multifamily Completions Normalize from Historic Highs

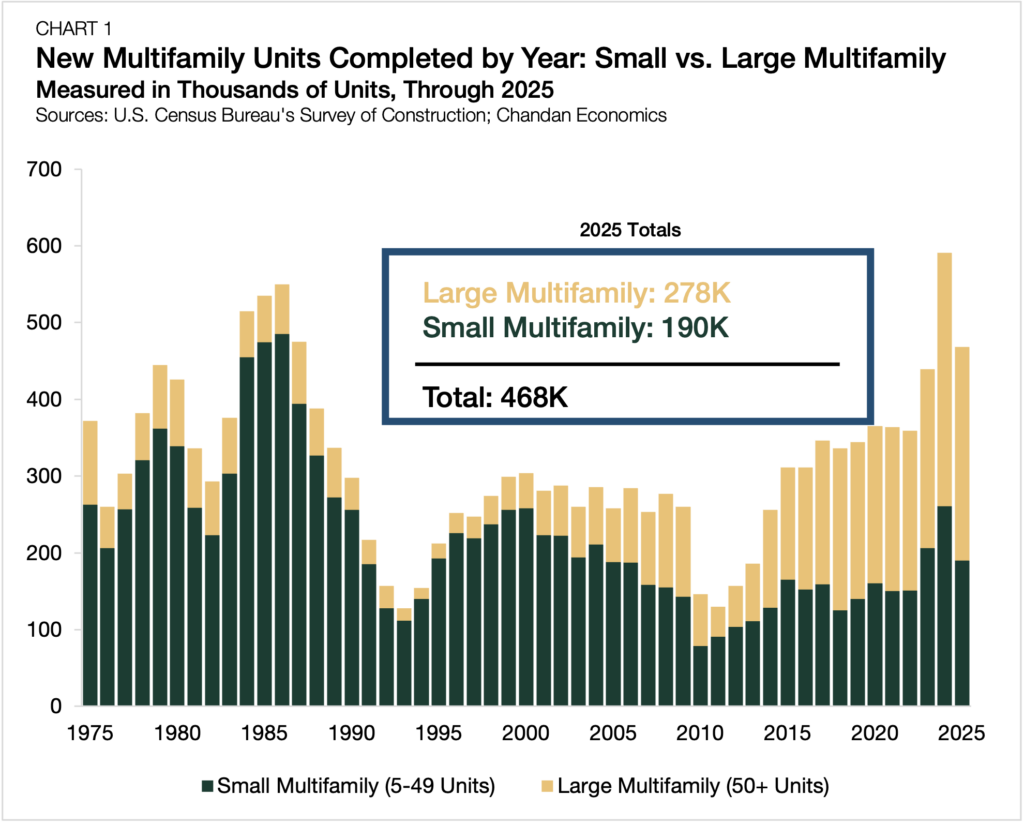

After surging to a historic high in 2024, multifamily completions moved lower in 2025. Across small and large multifamily properties, total completions declined from 591,000 units in 2024 to 468,000 units in 2025 (Chart 1).

The shift was more pronounced among smaller properties. Completions in buildings with 5–49 units fell to 190,000 units, down 27.2% from the prior year. By comparison, completions in properties with 50 or more units declined 15.8% to 278,000 units, coming down from the record high reached in 2024.

Even so, the 2025 decline reflects a normalization from historically elevated levels rather than a full reversal of the multifamily construction cycle. Large multifamily completions remained above every annual total recorded before 2023, indicating that the sector continues to deliver new supply at a comparatively strong pace.

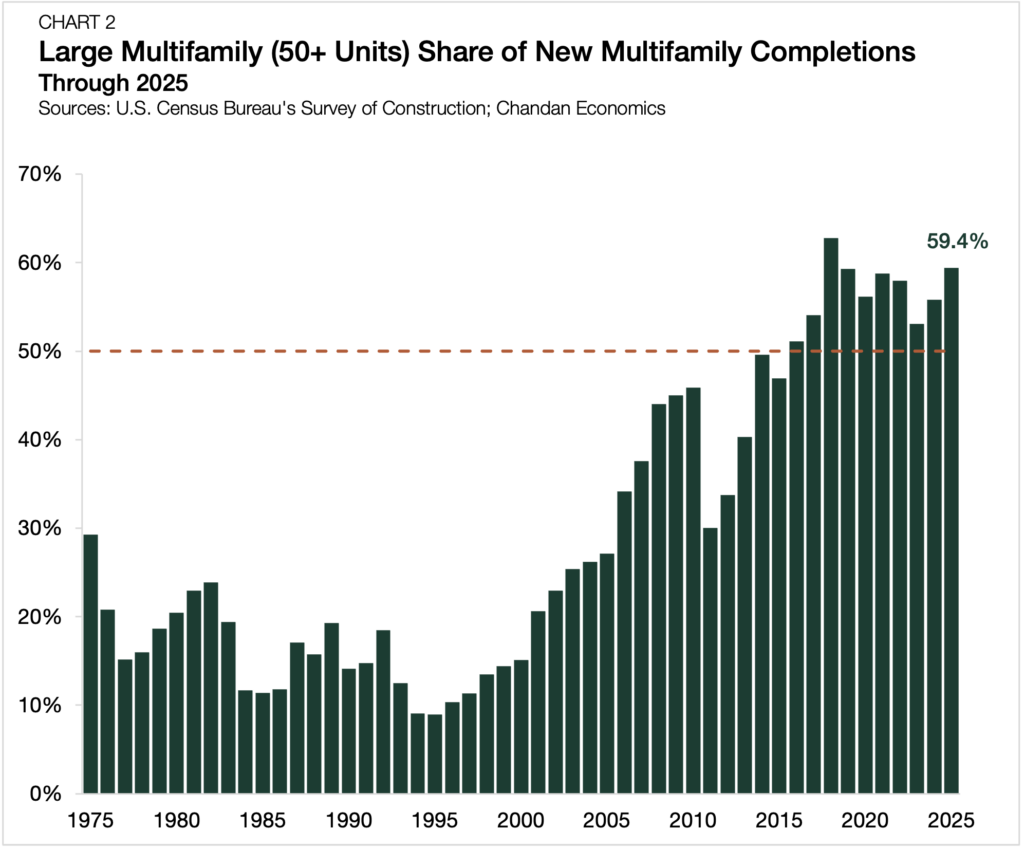

The composition of new multifamily construction also continued shifting toward larger properties. Buildings with 50 or more units accounted for 59.4% of all multifamily units completed in 2025, up from 55.8% in 2024 (Chart 2). This shift may also reflect the financial realities of development. A recent Urban Institute study highlighted that larger projects can offer economies of scale, while smaller developers often face greater barriers related to up-front capital, financing access, and project risk. Before 2016, large properties had never represented a majority of annual multifamily completions. Since then, they have accounted for more than half of completed units every year.

The large multifamily share of new multifamily completions in 2025 was the second highest in 50 years, trailing only the 62.8% recorded in 2018. The persistence of this trend suggests that the sector’s move toward larger properties is not simply the result of one unusually strong development year. It has become a defining and enduring feature of the past decade’s multifamily construction environment.

Larger Does Not Always Mean Taller

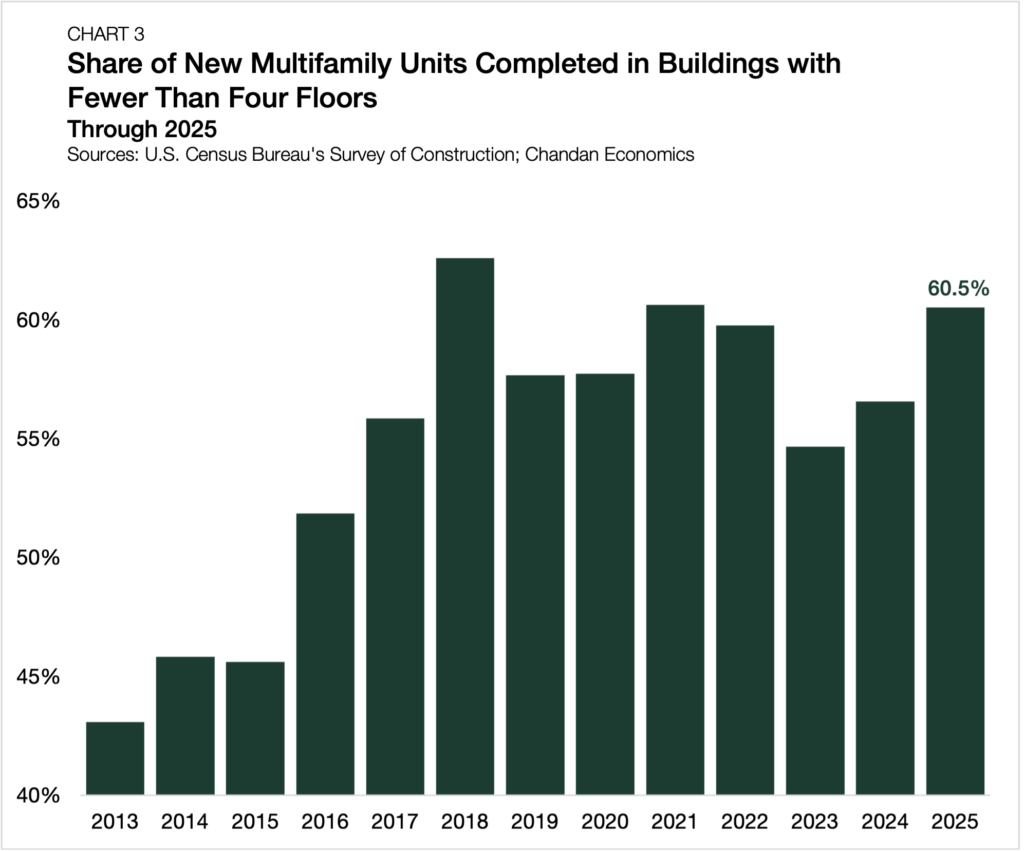

The rise of larger multifamily properties has not translated exclusively into taller buildings. In 2025, 60.5% of completed multifamily units were in buildings with fewer than four floors, up from 56.6% one year earlier (Chart 3).

The longer-term shift is notable. In 2013, only 43.1% of completed multifamily units were in buildings with fewer than four floors. By 2018, that share had risen to 62.6%, and it has remained above 50% every year since 2016. This points to a sustained lower-rise development environment. In other words, the sector is increasingly delivering large multifamily properties without relying exclusively on high-rise urban formats.

These data are consistent with the growing role of garden-style and suburban-oriented multifamily communities, where developers can add meaningful rental supply in lower-density settings. As housing affordability pressures continue to shape renter demand, lower-rise multifamily can offer a pathway to add supply in markets where high-rise development may be less feasible, less aligned with local demand, or more difficult to advance under existing zoning rules.

Other data points in the Census Bureau’s survey also support this interpretation. The share of completed multifamily units with more than one bedroom rose to 49.6% in 2025, up from 47.0% one year earlier. While still well below the 73.9% share recorded in 2004, the recent increase is consistent with some new supply serving households seeking more space.

The Bottom Line

Multifamily construction has normalized from historic highs in 2025, but the broader story is more complex. Developers are still adapting to high land costs, affordability pressures, changing renter needs, and the practical realities of where new housing can still get built.

Increasingly, that adaptation appears to include larger, lower-rise multifamily communities. These properties may not fit the traditional image of urban density, but they play an important role in expanding rental supply in suburban and lower-density markets where housing demand continues to grow.

As affordability pressures continue to shape renter demand and development activity, the characteristics of new multifamily construction will remain an important indicator of how the rental housing sector is adapting to changing market needs.

Interested in the multifamily real estate investment market? Contact Arbor today to learn about our array of multifamily, single-family rental, and affordable housing financing options or view our multifamily articles and research reports.