U.S. Multifamily Market Snapshot — November 2025

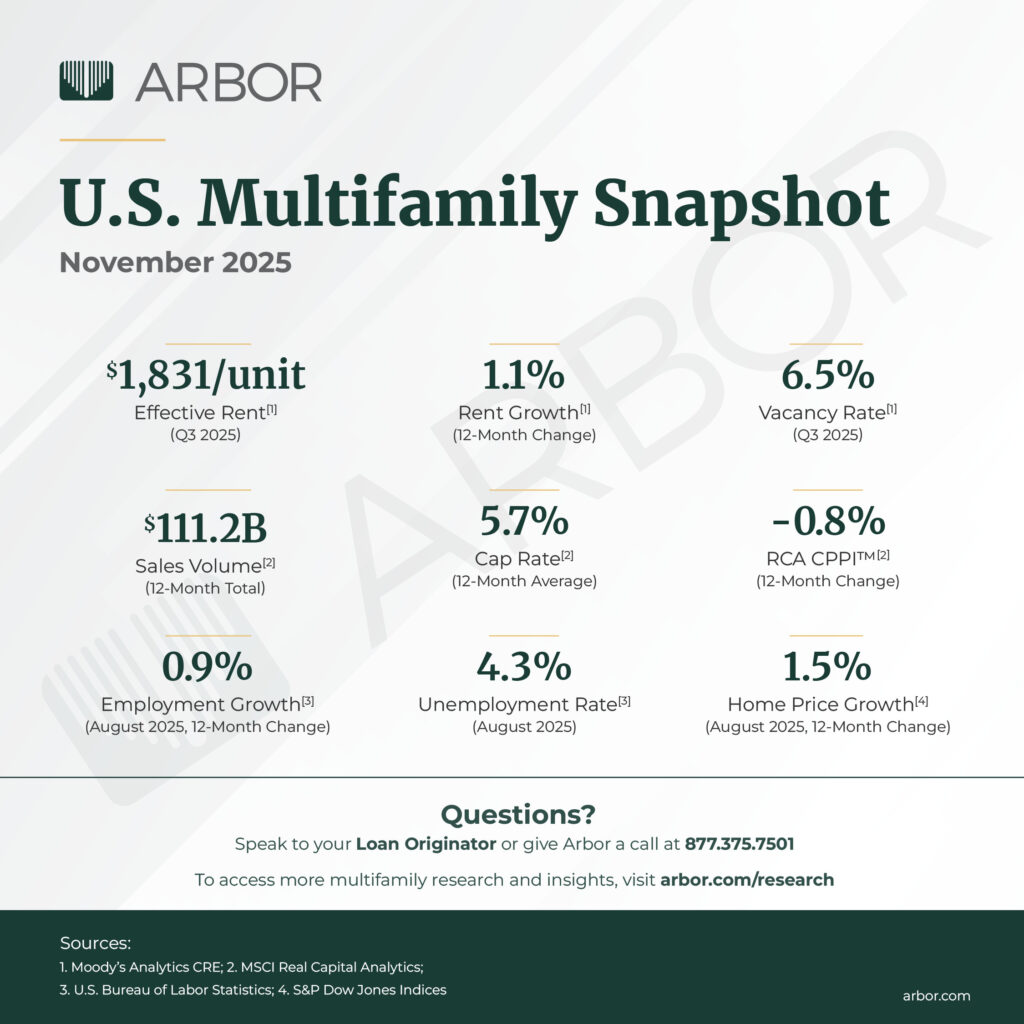

The U.S. multifamily market demonstrated clear signs of stabilization during the third quarter of 2025, as supply imbalances eased and investment activity climbed. Rent growth remained in line with pre-pandemic levels while vacancy rates held steady, and investors took advantage of easing interest rates.

According to data from Moody’s Analytics CRE, overall effective rent growth climbed by 1.1% over the past 12 months and remained more than 20% higher than pre-pandemic levels in 2019. At the market level, a mix of maturing, dynamic markets and affordable, opportunity-rich metros outperformed, according to the latest Arbor-Chandan Multifamily Opportunity Matrix, with Nashville, TN, leading the way.

Over the past two years, the pace of new development has been declining nationally. With that easing, the overall vacancy rate has held steady, finishing the third quarter at 6.5%. The rate has remained essentially unchanged for nearly a year, although Moody’s forecasts that vacancy will begin to tighten more significantly starting in 2026. Additionally, absorption is forecasted to rise this year, marking the third consecutive year of increasing rental demand, with completions remaining strong.

According to the latest report from MSCI Real Capital Analytics apartment investment volume during the third quarter totaled $43.8 billion, outpacing the prior year by 13%, and on par with levels observed prior to the pandemic in 2015 through 2019. Dallas led the nation in investment activity, with $6.7 billion in sales volume, and no other market was within $2.2 billion of Dallas’s total. Pricing also remained stable, with cap rates remaining near 5.7% for the seventh consecutive quarter.

Results of the National Multifamily Housing Council’s (NMHC) latest Quarterly Survey of Apartment Market Conditions signaled that the decline in interest rates over the past three months resulted in improved conditions for debt financing and an uptick in apartment deal flow. Additionally, 83% of participants in NMHC’s Quarterly Survey of Apartment Construction & Development Activity cited that the primary cause for delays in construction starts over the past three months was economic uncertainty, up from 57% in June and 68% in March.

As interest rates have continued to ease, the U.S. multifamily market’s stable foundation has solidified its standing as a premier asset class. Revived investor activity has reinforced the sector’s short-term and long-term prospects. Demand fundamentals are stabilizing, underwriting conditions are becoming more favorable, and price discovery has materialized. Despite lingering macroeconomic uncertainties, the multifamily market is expected to remain an attractive investment target for years to come.

Interested in the multifamily real estate investment market? Contact Arbor today to learn about our array of multifamily, single-family rental, and affordable housing financing options and view our multifamily articles and research reports.