Investment

Arbor Realty Trust and Chandan Economics’ latest Special Report leverages industry-leading data analysis to interpret key multifamily real estate trends as the sector moves from recalibration to stabilization. With occupancy levels remaining strong and loan originations rebounding sharply, this biannual report outlines why now is an opportune time to deploy capital.

Articles

The nation’s rental housing is older than at any point on record, with a median age of 45 years, according to the 2026 America’s Rental Housing report from Harvard’s Joint Center for Housing Studies (JCHS). America’s aging housing stock has created unique opportunities as the need for capital investments to rehabilitate and preserve affordable housing units rapidly rises.

Current Reports

Arbor’s Single-Family Rental Investment Trends Report Q1 2026, developed in partnership with Chandan Economics, spotlights how market shifts, including the rising cost of living and historically high build-to-rent activity, have fueled record rental household growth.

Articles

Multifamily permitting trends indicate continued national stability amid local recalibration. Across the country, issuances were steady, rising just 2.6% in 2025. At the metropolitan level, trends diverged sharply, with some markets accelerating and others pulling back. Per-capita leaders continued to cluster around high-growth Sun Belt and regional hubs, while year-over-year market-level fluctuations suggest that more pipelines have become increasingly selective and, in some cases, more concentrated in large-scale projects.

Analysis

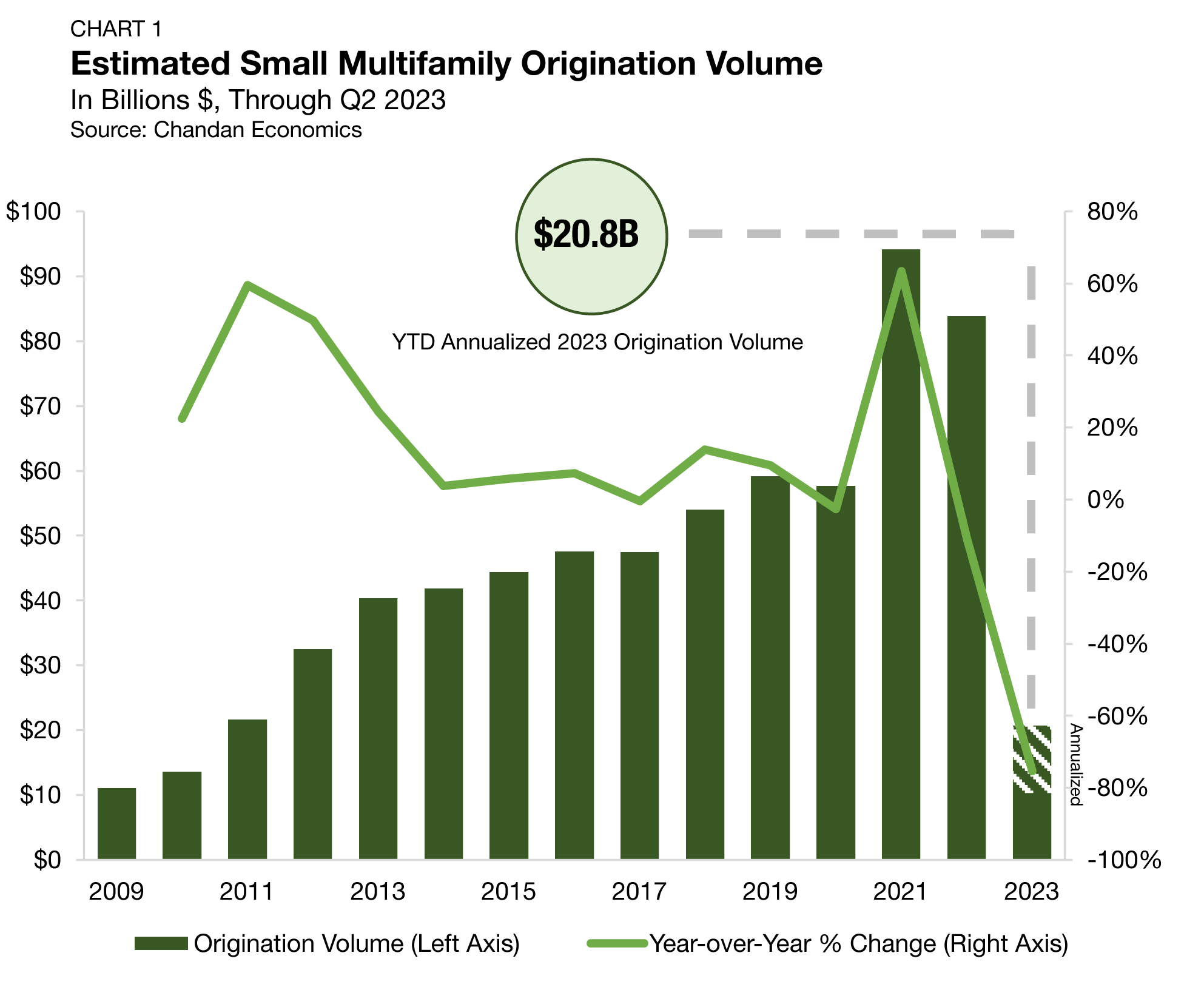

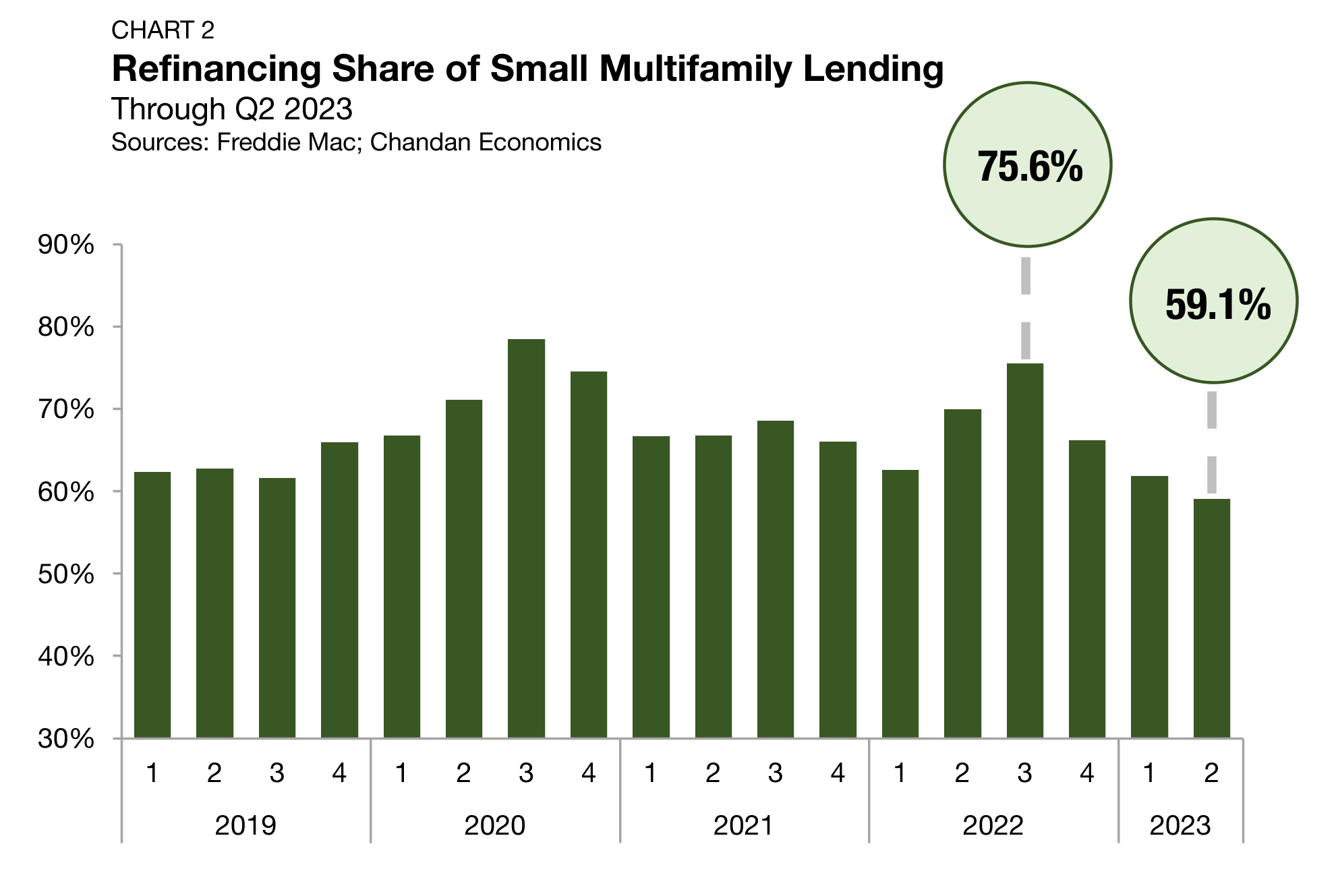

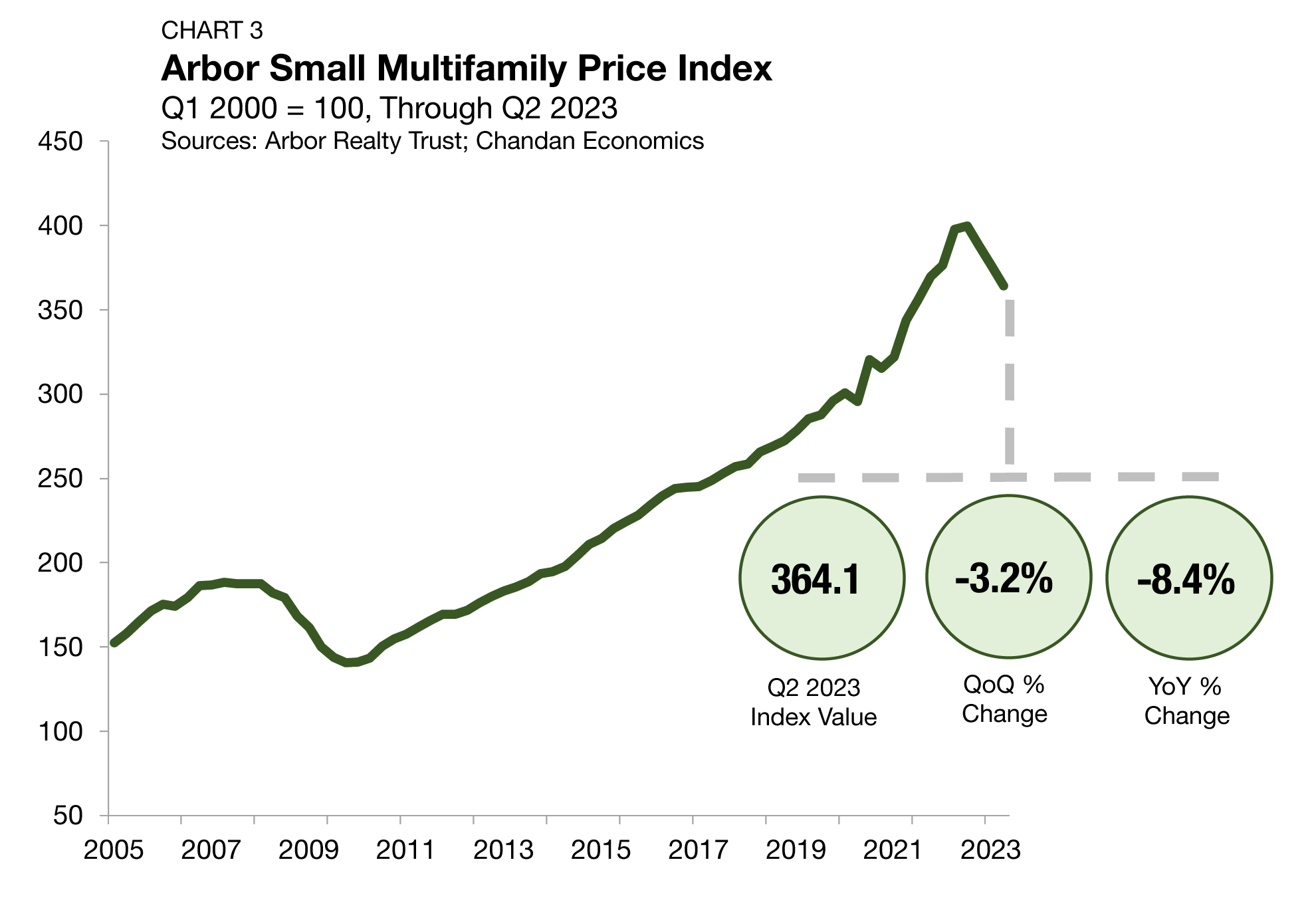

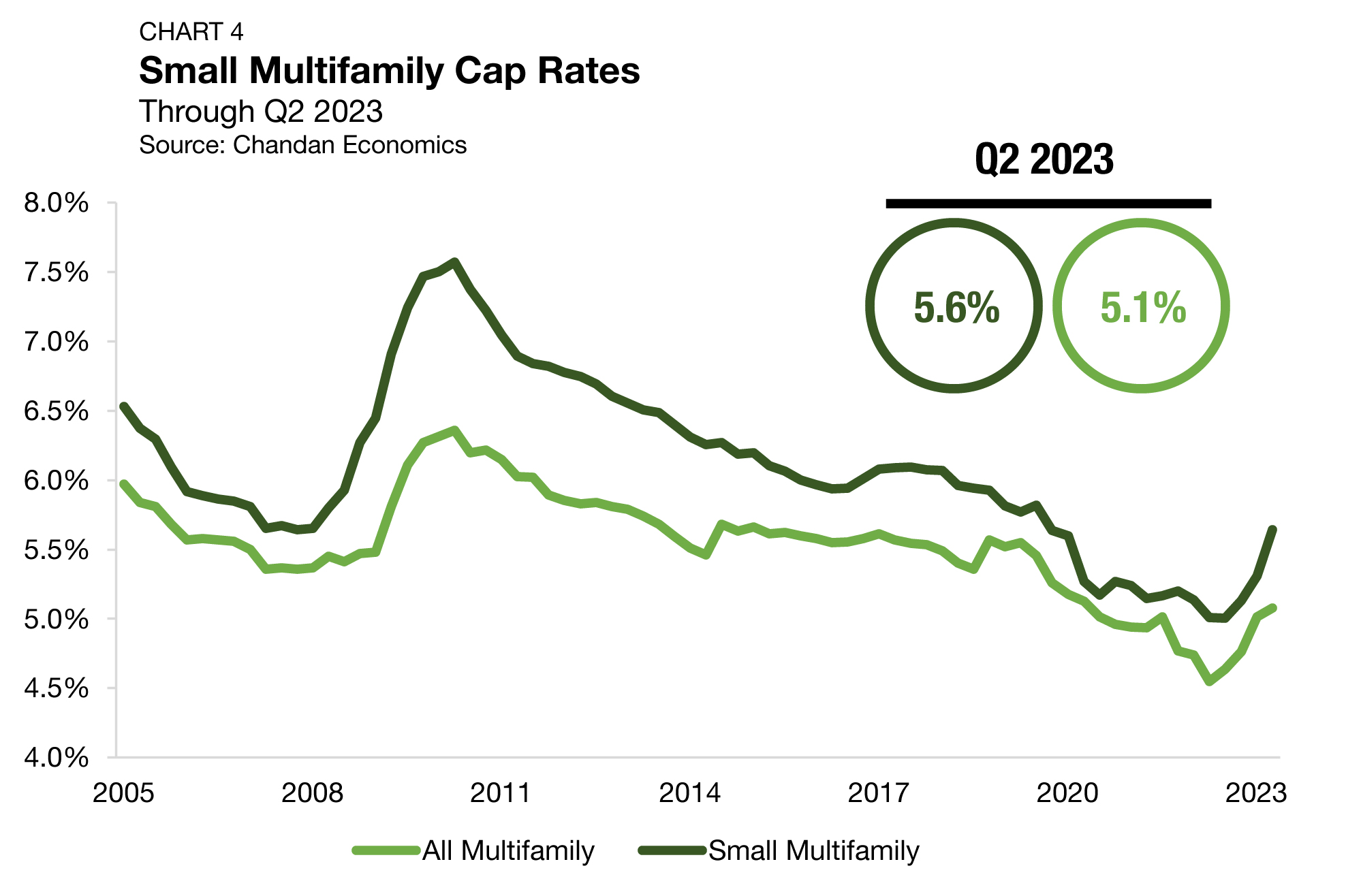

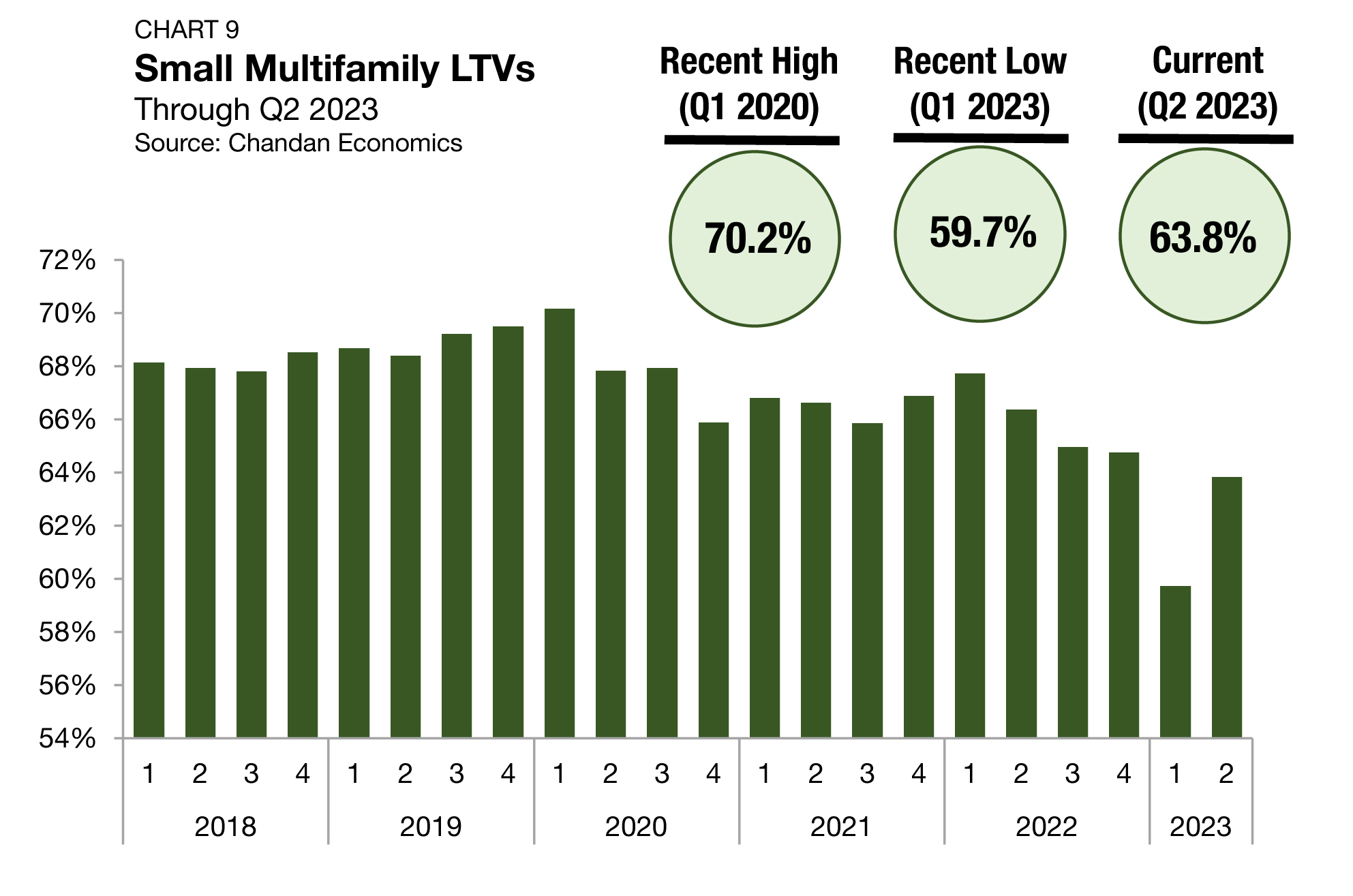

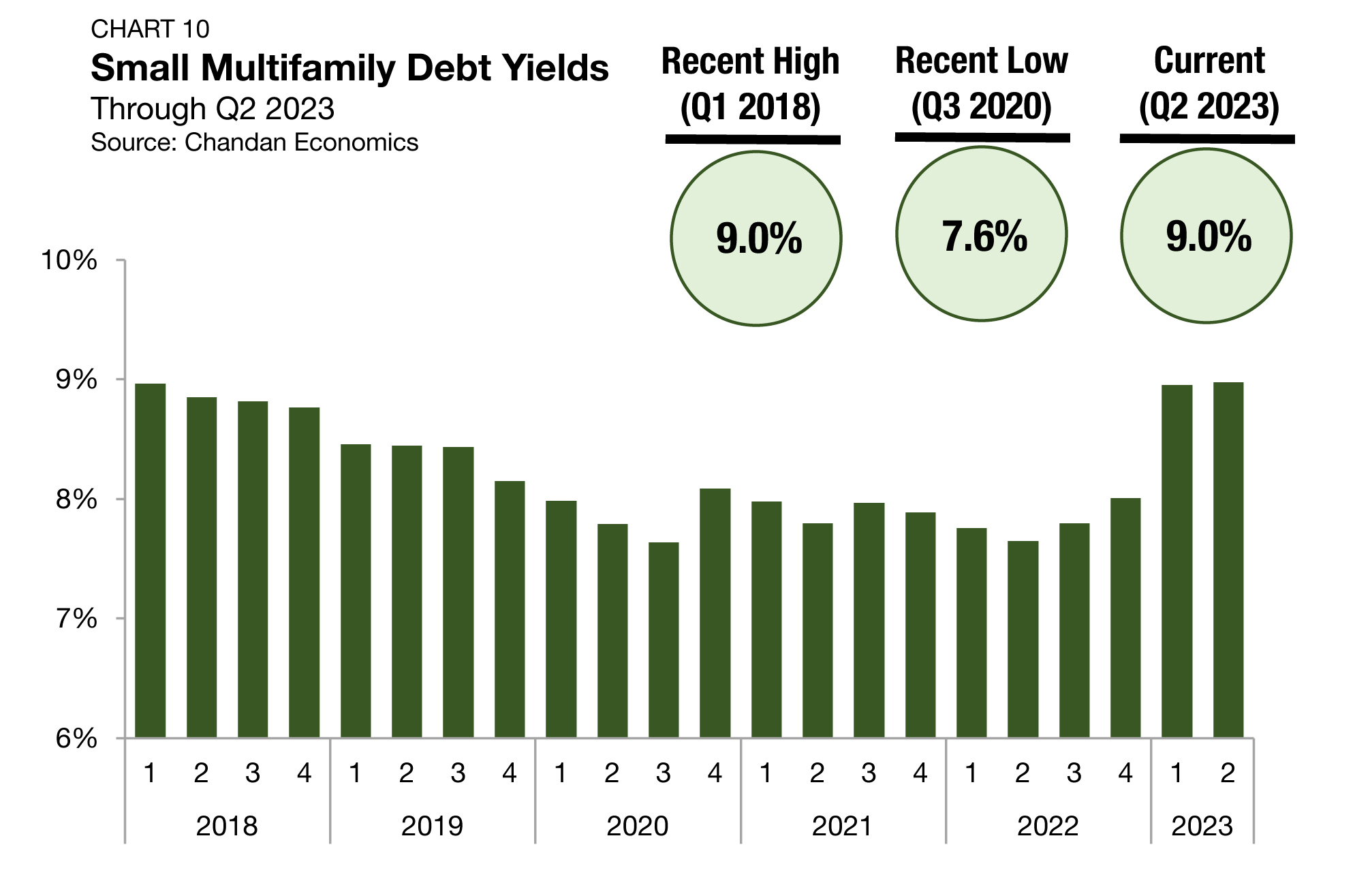

The small multifamily sector entered 2026 on a strong note, even as lending conditions remained shaped by persistently high interest rates and regulatory uncertainties.

Articles

The Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD), is one of the largest mortgage insurers in the world. The agency insures mortgages on affordable housing, multifamily properties, single-family homes, and healthcare facilities. Since 1934, FHA has financed over 50,000 multifamily mortgages nationwide. Whether you’re interested in acquiring, refinancing, or rehabilitating an affordable housing property, FHA multifamily loans are a financing route you need to know about.

FHA® 232/223(f): Healthcare Refinance, Acquisition or Mod Rehab

Articles

Despite a national slowdown, population growth remained concentrated in a small group of states in 2025, where strong net domestic migration inflows, economic opportunity, and in some cases elevated birth rates drove the annual increases. Overall, 14 states had an annual population growth rate above 0.75%, while 12 states had less than 0.1%, according to a Chandan Economics analysis of the U.S. Census Bureau’s 2024 American Community Survey.