Articles

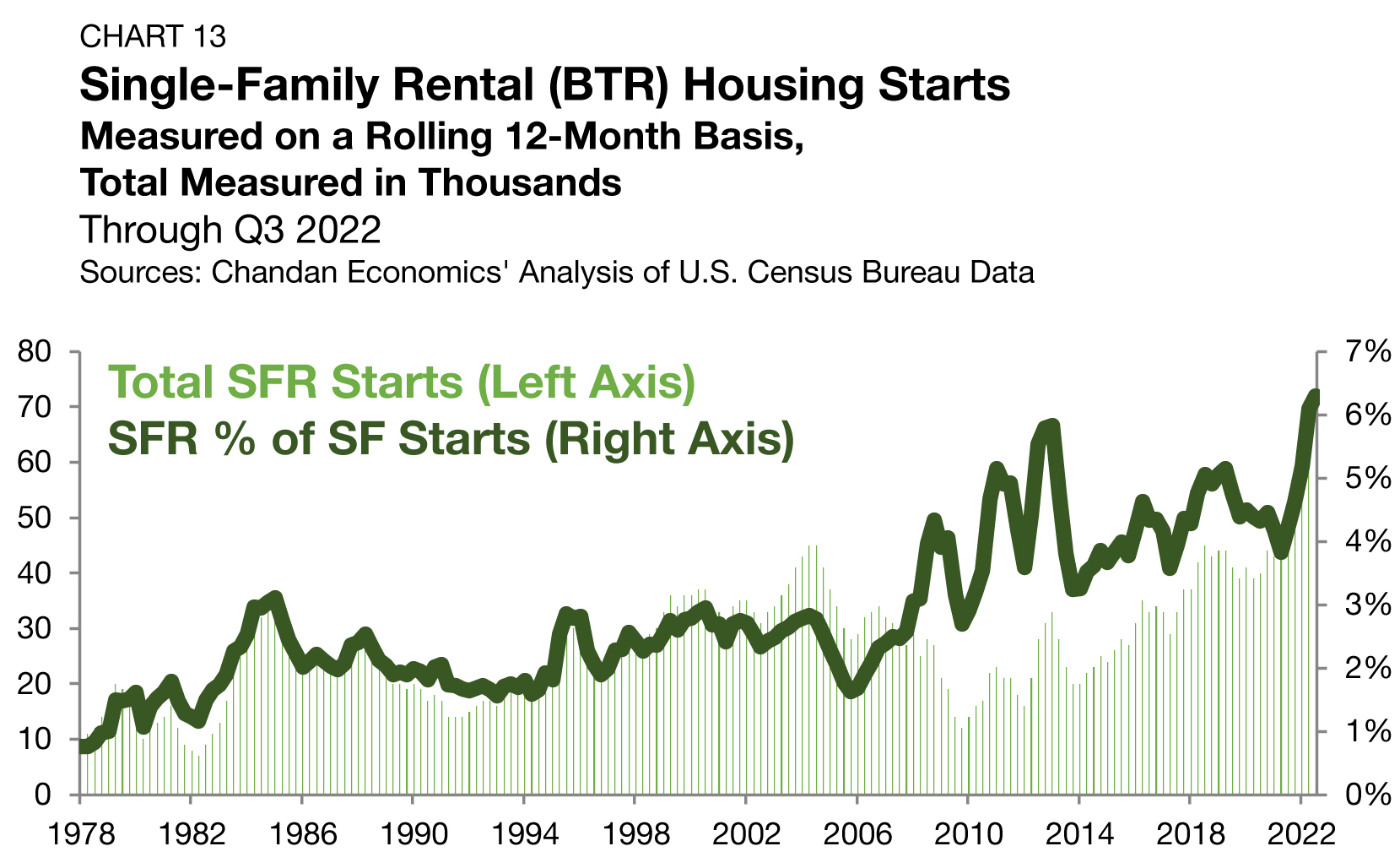

As the single-family rental (SFR) sector has matured, build-to-rent (BTR) has become a key source of new supply. Purpose-built rental communities are absorbing demand from households seeking the space and privacy of single-family living without the financial or lifestyle commitments of homeownership. Newly released U.S. Census Bureau data show that while SFR/BTR construction continued to decline from its 2024 peak through year-end 2025, development activity remains elevated compared to historical norms.

Articles

In commercial real estate, long-term financial partnerships drive deals. At the recent Real Estate Pride Roundtable in New York City, CRE leaders shared how living openly with their LGBTQ+ identities has allowed them to lead with authenticity in the boardroom and in life. This Pride Month, Arbor celebrates authenticity in the workplace.

Articles

In a new video, Dr. Sam Chandan, a leading commercial real estate scholar, expands on the findings of Arbor Realty Trust’s latest Special Report, developed in partnership with Chandan Economics. He shares his expert insight into the state of rental housing in spring 2026. Chandan notes that multifamily is moving toward a state of balance as supply pressures ease and growth trends turn positive. The result, he said, is that selective opportunities are emerging for well-positioned investors in a climate “defined less by dislocation” and “more by normalization.”

Articles

Homeownership has been an aspiration of generations of Americans, but elevated prices, mortgage rates, and financing hurdles are complicating the typical path to owning a home. According to the Federal Reserve Bank of New York’s 2026 Survey of Consumer Expectations Housing Survey, renters are continuing to experience difficulty with mortgage financing and have more measured views about homeownership’s current investment potential. As households reassess the housing market, rental housing demand is the beneficiary.

Current Reports

Arbor Realty Trust’s latest Small Multifamily Investment Trends Report, developed in partnership with Chandan Economics, evaluates what’s driving this sector’s ongoing stability as macroeconomic conditions remain mixed. Loan originations rose last quarter, and valuations are rebounding, signaling that normalization is taking hold.

Analysis

Over the past 12 months, the leading rent growth markets spanned multiple regions, each exhibiting distinct strengths and characteristics.

Articles

Labor market conditions are a foundational driver of rental housing demand, influencing tenant stability and household growth. While the national pace of hiring has moderated, the economies of many metropolitan areas continue to outperform. Expanding on Arbor’s latest Top Markets for Multifamily Investment Report, our research teams highlight the local dynamics supporting growth in several of the country’s strongest-performing multifamily markets.

Analysis

The U.S. multifamily sector continued to build momentum at the start of 2026. Rent growth moved into positive territory, and a moderating construction pipeline showed that vacancy may have reached its cycle peak.