Build-to-Rent Activity Stabilizes Above Historical Highs

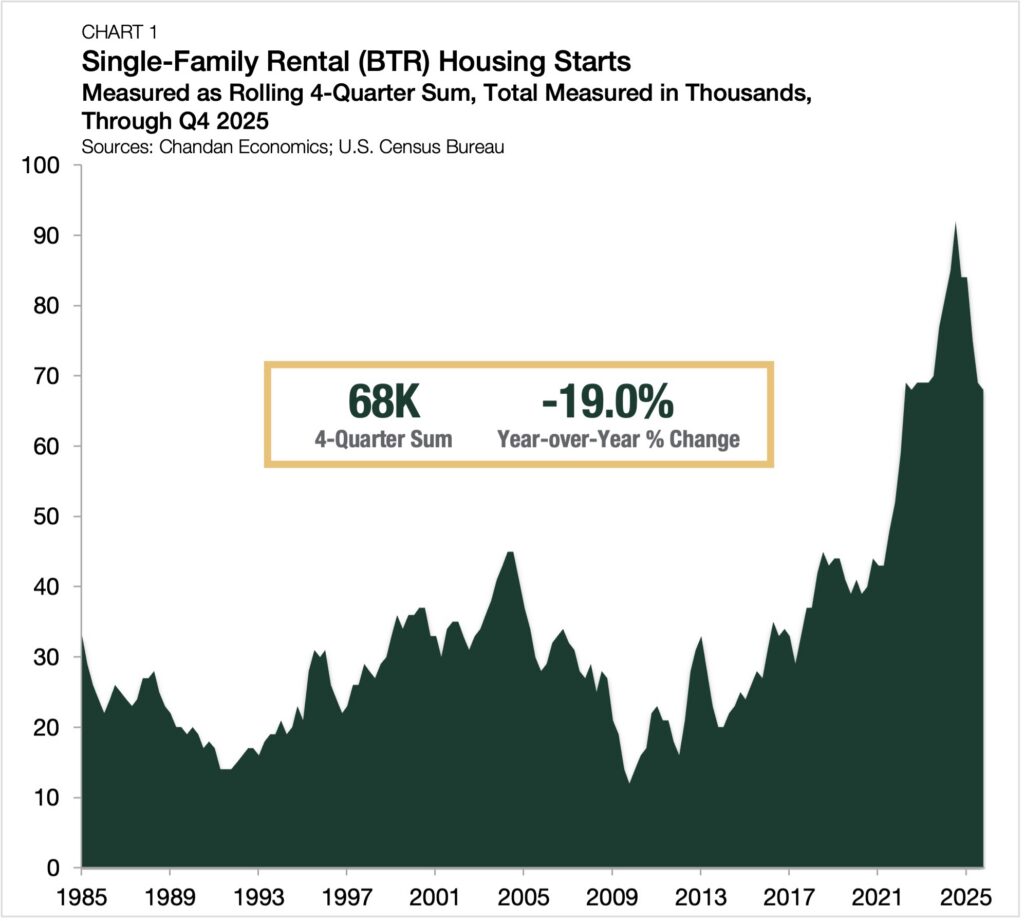

- SFR/BTR housing starts totaled 68,000 in 2025, down from last year’s record highs, although remaining robust.

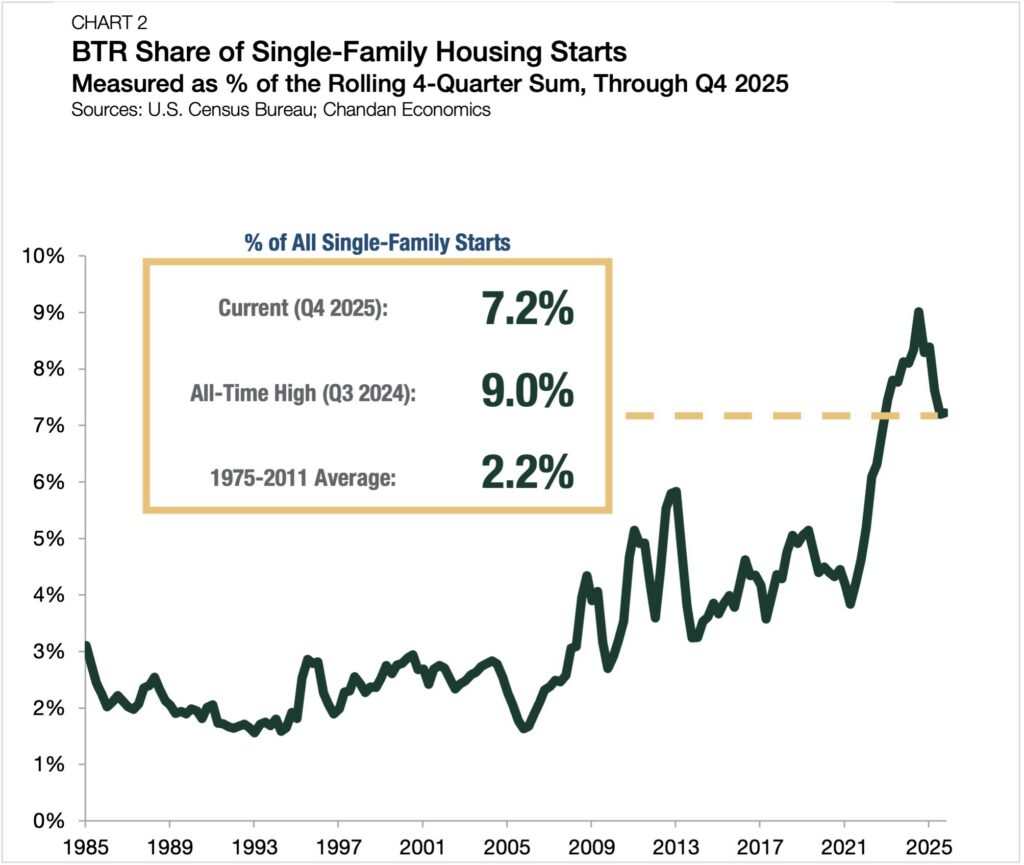

- BTR accounted for 7.2% of all single-family housing starts, remaining well above historical standards.

- While legislative uncertainties have slowed 2026 production, recent progress creates a rosier outlook.

As the single-family rental (SFR) sector has matured, build-to-rent (BTR) has become a key source of new supply. Purpose-built rental communities are absorbing demand from households seeking the space and privacy of single-family living without the financial or lifestyle commitments of homeownership. Newly released U.S. Census Bureau data show that while SFR/BTR construction continued to decline from its 2024 peak through year-end 2025, development activity remains elevated compared to historical norms.

SFR/BTR Construction Activity Normalizes

As detailed in Arbor’s Single-Family Rental Investment Trends Report series, developed in partnership with Chandan Economics, the SFR construction pipeline has decelerated lately. SFR/BTR starts totaled 68,000 units in the 12 months ending in December 2025 (Chart 1).

The rolling annual sum hit an all-time high of 92,000 in the third quarter of 2024 and has fallen in four of the past five quarters. Compared to the same time last year, the rolling sum is down by 16,000 units (-19.0%). Despite this reversal, the current level of BTR development remains historically robust, with the latest annual tally exceeding all yearly and quarterly totals before 2022.

Looking beyond units created, the BTR share of all single-family construction has also moved below recent highs. Over the year ending in the fourth quarter of 2025, BTR accounted for 7.2% of all single-family construction starts, down from 8.3% one year earlier and 9.0% at its third-quarter 2024 peak (Chart 2). BTR’s single-family construction market share remains above its trailing five-year average of 6.8%. Before 2022, its market share had never eclipsed 6.0%. This underscores the fact that while development activity has retreated, the sector continues to be fundamentally sound, and its production remains elevated compared to just a few years ago.

Lower BTR production is consistent with a broader normalization in single-family development activity. The higher cost of capital, rising home inventory, and more cautious builder sentiment have all contributed to a slower construction environment. However, the newly released Census data does not suggest a sharp break in BTR activity; it instead shows the sector is normalizing as it continues to command larger shares of single-family development.

Outlook

As covered in greater detail in Arbor’s latest Single-Family Rental Investment Trends Report, the SFR/BTR sector remains supported by long-term demand for attainable, lower-maintenance rental housing. Although production remained steady through the fourth quarter of 2025, the 21st Century ROAD to Housing Act up for consideration in Congress has created a more cautious development environment of late. However, a revised version of the bill, which passed the U.S. House of Representatives in late May, removes the seven-year sale-to-homeowner requirement and adds broader carve-outs for purpose-built rental housing. As a result, the final legislation may ultimately have a substantially softer impact on a key commercial real estate sector directly responsible for creating quality rental housing.

Interested in the multifamily real estate investment market? Contact Arbor today to learn about our array of multifamily, single-family rental, and affordable housing financing options or view our multifamily articles and research reports.