Renters Reassess Homeownership as Affordability Challenges Persist

- Renters still broadly value homeownership, but higher mortgage rates and subdued buying expectations suggest more households may remain in the rental market for longer.

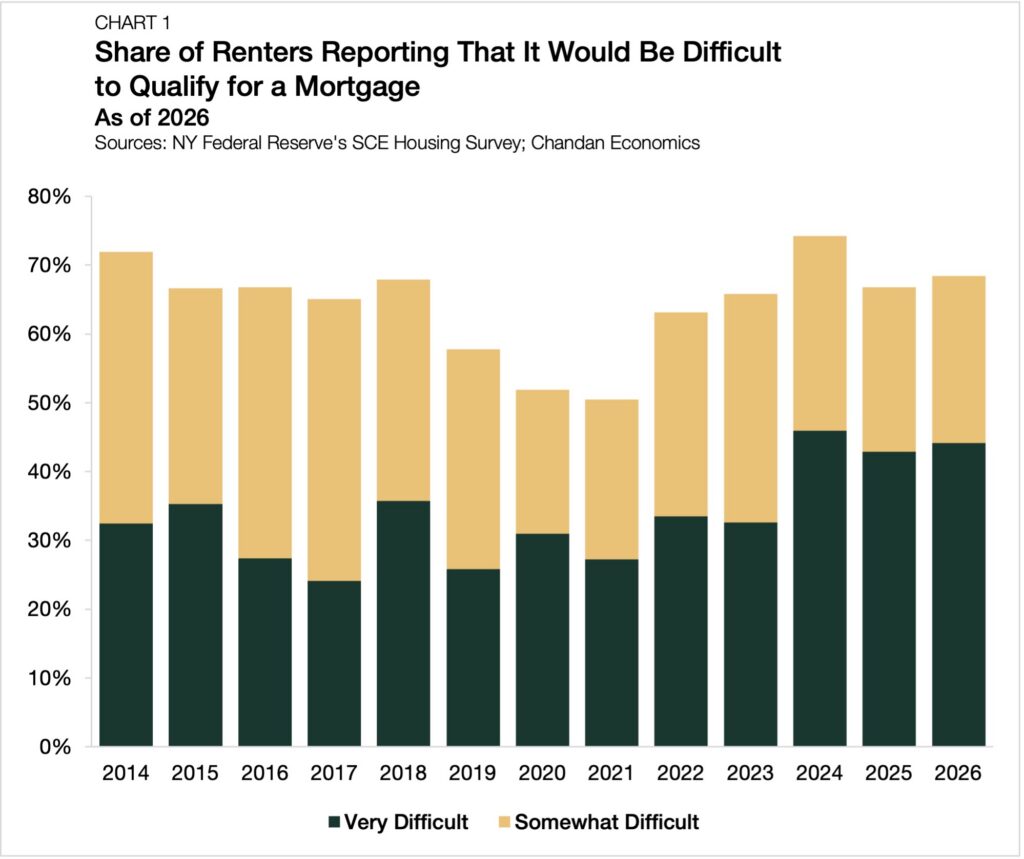

- Obstacles to purchasing a home persist, with 68.5% of renters reporting that obtaining a home mortgage would be somewhat or very difficult.

- Affordability challenges are beginning to reach higher-earning renters as home prices outpace wage growth and mortgage rates remain elevated.

Homeownership has been an aspiration of generations of Americans, but elevated prices, mortgage rates, and financing hurdles are complicating the typical path to owning a home. According to the Federal Reserve Bank of New York’s 2026 Survey of Consumer Expectations Housing Survey, renters are continuing to experience difficulty with mortgage financing and have more measured views about homeownership’s current investment potential. As households reassess the housing market, rental housing demand is the beneficiary.

Hurdles to Homeownership Increase

Renters continue to view mortgage access as a significant hurdle to homeownership. In the latest New York Fed Housing Survey, 68.5% of renters said it would be either somewhat or very difficult to obtain a home mortgage, up from 66.8% in 2025 (Chart 1). The “very difficult” share rose to 44.2%, remaining near the highest level in the history of the survey.

Obstacles to obtaining a mortgage have become more pronounced. Among those earning at least $60,000 annually, the share that reported obtaining a mortgage would be somewhat or very difficult rose by more than 20 percentage points since 2021, reaching 58.4% in 2026. This trend suggests that affordability constraints are no longer limited to lower-income renter households. Even renters with relatively stronger earnings profiles have reported more difficulty accessing the mortgage market.

One likely driver is that home prices have continued to outpace wage growth. Since the start of 2021, U.S. home prices are up 38.5%, compared with a 25.0% increase in average hourly earnings for private-sector workers. Broader inflation pressures have also weighed on household budgets over this period. Together, these dynamics have added pressure to down payment needs, debt-to-income ratios, and borrower qualification.

Mortgage rates remain another major affordability constraint. This spring, prevailing mortgage rates have held around 6.4%, remaining well above the levels many prospective buyers grew accustomed to before the Federal Reserve’s tightening cycle.

Renters’ perceptions point to an even more difficult borrowing environment. The average renter believes the mortgage rate they would qualify for today is 8.4%, above the prevailing national rate, and expects mortgage rates to move higher over the next several years. Misinformed expectations like these are reinforcing the view that mortgage affordability is pushing homeownership out of reach for many.

Renters Reassess the Value of Owning

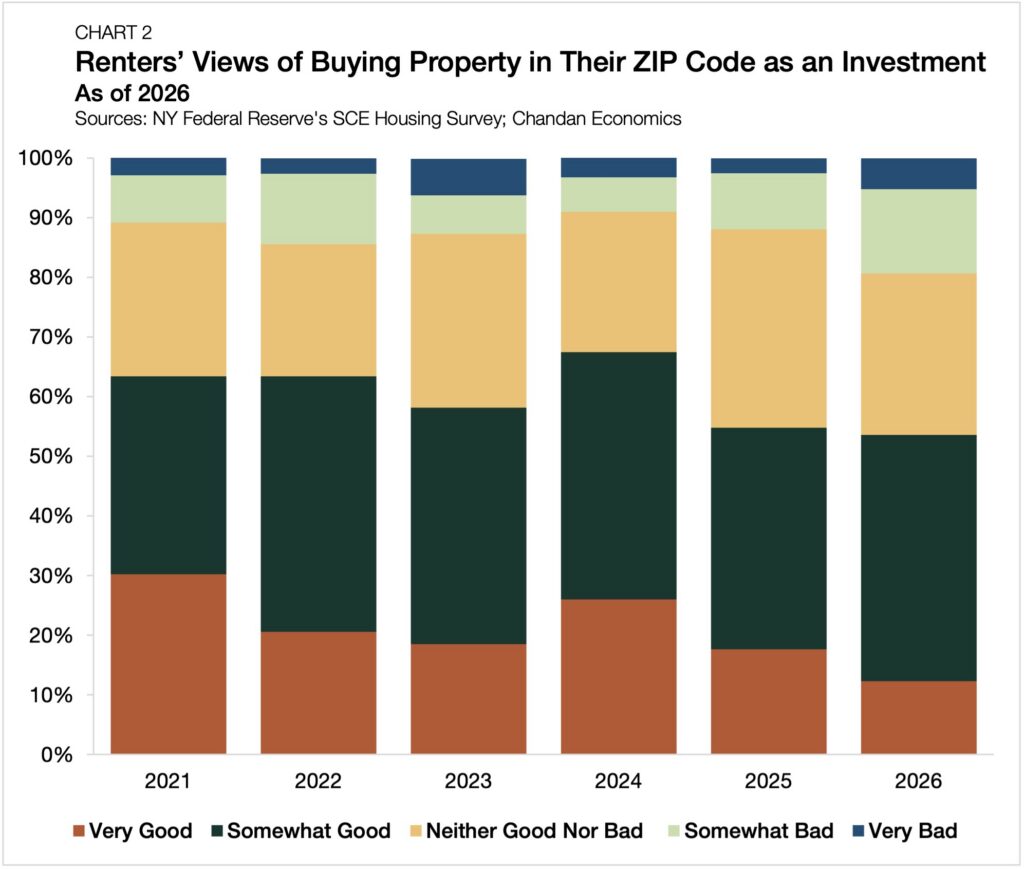

Financing challenges appear to be shaping not only renters’ ability to buy, but also how they evaluate the financial benefits of owning a home. Renters’ views of homeownership as a financial investment have softened. In 2026, 53.6% of renters said buying property in their ZIP code would be either a somewhat or very good investment, down by about 14 percentage points in the past two years (Chart 2). The “very good” share also fell to 12.3%, the lowest level since this question was introduced.

Renters also generally continue to prefer owning when financial constraints are removed, though that preference has become less decisive. The share of renters who prefer or strongly prefer owning fell from 71.5% in 2025 to 64.5% in 2026, while the share that is indifferent rose to 21.8%. This shift suggests that some renters may be placing greater weight on the flexibility, lower maintenance burden, and lifestyle advantages that renting can provide.

Additionally, long-term buying expectations remain subdued. The average renter reported a 34.7% probability of owning a primary residence at some point in the future, only slightly higher than last year but still well below the mid-2010s, when the average expected probability of future ownership exceeded 50%.

Taken together, the survey results suggest renters are not rejecting homeownership. Rather, they are reassessing the costs, accessibility, and investment value of owning in today’s housing market. For rental housing, this points to a demand environment where lifestyle renting and delayed ownership transitions may both continue to support renter household retention, even as many renters still view ownership as a preferred long-term outcome.

The Bottom Line

The New York Fed’s survey shows that renters still broadly value homeownership, but many are reassessing its accessibility and financial upside. With mortgage access perceived as difficult, home prices outpacing wage growth, and mortgage rates remaining elevated, the renter-to-owner transition has become more challenging across the U.S. As for-sale residential housing continues to experience headwinds, rental households are growing at a significantly higher pace than owner-occupied housing, strengthening demand across all multifamily property types.

Interested in the multifamily real estate investment market? Contact Arbor today to learn about our array of multifamily, single-family rental, and affordable housing financing options or view our multifamily articles and research reports.